FHA CE Class

•Als PPT, PDF herunterladen•

0 gefällt mir•298 views

Performance School of Real Estate FHA CA Class

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie FHA CE Class

Ähnlich wie FHA CE Class (20)

Mehr von JTtheCoach.com

Mehr von JTtheCoach.com (7)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

FHA CE Class

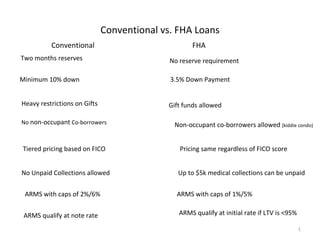

- 1. Conventional vs. FHA Loans Conventional FHA No reserve requirement Two months reserves Minimum 10% down 3.5% Down Payment Heavy restrictions on Gifts Gift funds allowed No non-occupant Co-borrowers Non-occupant co-borrowers allowed (kiddie condo) Tiered pricing based on FICO Pricing same regardless of FICO score No Unpaid Collections allowed Up to $5k medical collections can be unpaid ARMS with caps of 2%/6% ARMS with caps of 1%/5% ARMS qualify at note rate ARMS qualify at initial rate if LTV is <95%

- 2. Conventional vs. FHA Loans Conventional FHA Private MI required (over 80% LTV) Government insured Must have DU/LP approval Loan can be manually approved 2 years after Chapter 7 4 years out of Chapter 7 2 yrs. after payoff on Chapter 13 1 yr. of on-time payments after Chapter 13 7 yrs. after Foreclosure 3 yrs. After Foreclosure

- 4. FHA Flexible Credit Guidelines Minimum FICO score is 640 * Minimum time after a Chapter 7 Bankruptcy is 2 years (12 Mos minimum with extenuating circumstances-see below) Minimum time period after a Chapter 13 bankruptcy is one year from creditor settlement date with proof of on time payments for that year On Short Sale, it is possible to purchase a home one day after closing* If little credit history is available, alternative credit can be used. Payments on items such a car insurance, Utility bills or Cell phones can be used to create the credit required Minimum time period after a foreclosure is 3 years, unless extenuating circumstances: Death of wage earner Serious Illness Consumer Credit Counseling –must have paid payments on time for 12 mo. *In some exceptional cases, a score lower than 640 may be acceptable

- 5. Condominiums 234 (c ) Subdivision must be FHA approved Spot approval no longer available Do NOT trust MLS data-verify approval with Amerifirst LO

- 7. Appraisal Valuation Conditions These Valuation Conditions and protocol help the appraiser evaluate the standards required by the General Acceptability Criteria. The criteria are described below. It is helpful & facilitates the process if the following items are addressed prior to the appraiser viewing the property.