Renewable Energy Financing - An IEA Perspective

•

1 gefällt mir•1,222 views

Presentation by IEA Deputy Executive Director, Ambassador Richard Jones, at the Renewable Energy Finance in Practice Forum in Vienna on 31 May.

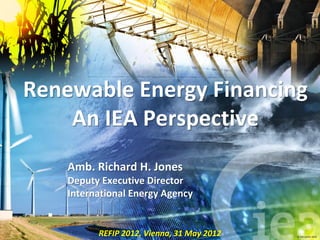

![Recent trends - Electricity

Wind Bioenergy Solar PV Hydro other

Generation

338 296 31 3503 74

2010 [TWh]

CAGR 2005-

26.5% 8.8% 50.8% 3.1% 4.6%

2010 [%]

© OECD/IEA 2010](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Andere mochten auch

Ähnlich wie Renewable Energy Financing - An IEA Perspective

Ähnlich wie Renewable Energy Financing - An IEA Perspective (20)

Mehr von International Energy Agency

Mehr von International Energy Agency (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Renewable Energy Financing - An IEA Perspective

- 1. Renewable Energy Financing An IEA Perspective Amb. Richard H. Jones Deputy Executive Director International Energy Agency REFIP 2012, Vienna, 31 May 2012 © OECD/IEA 2010

- 2. Recent trends - Electricity Wind Bioenergy Solar PV Hydro other Generation 338 296 31 3503 74 2010 [TWh] CAGR 2005- 26.5% 8.8% 50.8% 3.1% 4.6% 2010 [%] © OECD/IEA 2010

- 3. …and in Heat and Transport 60 50 • 3% share of road Mtoe 40 transport 30 • Grew at 26% per 20 year in average 10 0 • Growth focussed in Brazil, US, EU 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 Brazil bioethanol US bioethanol EU-27 biodiesel RoW biofuels 200 Rest of world China • Rapid growth in 150 solar water heating GWth 100 • Focused mainly 50 in China 0 © OECD/IEA 2010

- 4. Costs are falling Growing deployment has led 100 PV Module Price (USD 2010/Wp) < 1976 to cost reductions in key technologies < 1980 Hydro and some geothermal already 10 < 1990 cost-competitive < 2000 New technologies such as wind Learning Rate: 19.3% < 2010 onshore and biomass are competitive in a broader set of 1 1 10 100 1 000 10 000 100 000 circumstances Cumulative capacity (MW) Data from Breyer and Gerlach, 2010 PV still expensive but 19% cost reduction for each capacity doubling; parity with retail prices in the next five years in countries with high insolation and electricity prices © OECD/IEA 2010

- 5. Low-carbon power technologies come of age Global installed power generation capacity in the New Policies Scenario 10 000 GW Fossil-fuel additions 8 000 Nuclear additions Renewable additions 6 000 Existing 2010 capacity 4 000 2 000 0 2010 2015 2020 2025 2030 2035 Renewables account for about half of all the new capacity added worldwide through to 2035 © OECD/IEA 2011

- 6. Going green comes at a price Investment in new power plants and infrastructure in the New Policies Scenario 2011-2035: $16.9 trillion Renewables make up 60% of investment in new power plants, led by wind, solar PV & hydro, even though they represent only half of the capacity additions © OECD/IEA 2011

- 7. Impact of Capital Costs on Levelised Costs of Electricity 30 25 20 ct USD/kWh 15 PV Wind 10 CC Gas 5 0 0% 5% 10% Cost of Capital Note: Simplified calculation for illustration. Assumptions: Gas: 800 USD/kW; annual O&M: 2.5% of capex; FLH: 5000 h/y; 8 USD/Mbtu; 50% thermal efficiency Wind: 2200 USD/kW; 2.5% O&M; 3000 h/y PV: 3000 USD/kW; 1% O&M, 1500 h/y The financing regime is key for RE economics © OECD/IEA 2010

- 8. Cost of capital and risk Interest rates also depend on risks perceived by investors, influenced by: 1. General economic framework Large spreads in interest rates among countries 2. Technology risk RE encompass a wide range of technologies at different stages of maturity 3. Policy risk Stability of country policy frameworks over time © OECD/IEA 2010

- 9. Policy Schemes and Financing Interact Different policy instruments yield qualitative differences in financial flows: Certificate Schemes Generators under a certificate scheme are exposed to volatile prices for certificates and wholesale power Feed – In Schemes Under a classical FIT, cash flows are very stable and predictable Different risk/return profiles attract different investors Like returns on government bonds, FIT cash flows are predictable and well suited for institutional investors © OECD/IEA 2011

- 10. Policy Impact and Cost-Effectiveness Comparative assessment in OECD, BRICS and other DCs Example - Wind on-shore: Leading countries (e.g. DE, DK, PT, SP) have predictable incentives - mostly FITs/FIPs - and good overall policy framework Some countries using TGCs (IT, UK) show good deployment but at higher support costs Non-economic barriers can hamper any kind of support (e.g. in JP and GR) It is the overall policy framework that matters © OECD/IEA 2011

- 11. Best-Practice Policy Principles 1. Predictable RE policy framework, integrated into overall energy strategy 2. Portfolio of incentives based on technology and market maturity 3. Dynamic policy approach based on monitoring of national and global market trends 4. Non-economic barriers must be tackled 5. System integration issues must be addressed © OECD/IEA, 2012

- 12. Evolving RE Markets and Policies • With growing maturity level, policies need to evolve and increasingly expose investors to market risks Inception Take-off Consolidation Maturity Level & Deployment Predictable Hydro geothermal technology-specific incentives Wind on-shore Technology-neutral policies (e.g. C-pricing) Solar PV RD&D policies Wind off-shore Ocean CSP Time High-risk Low-risk Fully mature © OECD/IEA, 2012

- 13. One “size” does not fit all! Example Technology Policy / Typology of RE Risk Deployment investors Technology Phase Ocean Very High Inception VC-PE CSP High Take-off ? Wind offshore Funding gap PV Low Take-off Asset / Wind onshore Project Financing Hydro Low Consolidation Very Large / Consortia Investor type depends on risk profile Technology risk Project-specific risk © OECD/IEA 2010

- 14. Size and time matter RE projects come at very different sizes and investment levels and risks 5 kW PV rooftop 500 MW wind 10 GW off-shore large hydro 10 k EUR 1.75 bl EUR 15-20 bl USD Lead times for project construction also widely differ The difference in scale will yield different types of investors and financing products From home owners to very large investors and consortia. © OECD/IEA 2010

- 15. Emerging Financing Sources Development banks and export credit agencies are increasingly key sources New institutional and non-traditional investors gradually more active in renewable finance Pension, infrastructure, sovereign wealth funds; insurance companies; non-utility corporations New financial innovations emerging e.g. third-party leasing schemes for small-scale PV However, new investors have different risk profiles More experience and time needed Only gradual impact on markets © OECD/IEA 2010

- 16. Conclusions Very significant growth of renewables in all IEA scenarios, particularly in the power sector Investment needed in the 5-10 trillion USD scale by 2035 Different technologies will attract different investors depending on their maturity level and perceived risks Policies can play a major role in reducing risk for investors But can be a source of risk themselves Need to evolve over time © OECD/IEA 2010