Etica Wealth Management - Mutual Funds Presentation

•

2 gefällt mir•1,103 views

Detailed information on Mutual Funds, SIP, STP, Financial Planning, Investment Planning, Savings for Long term

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (17)

Andere mochten auch

Andere mochten auch (20)

Ähnlich wie Etica Wealth Management - Mutual Funds Presentation

Ähnlich wie Etica Wealth Management - Mutual Funds Presentation (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Etica Wealth Management - Mutual Funds Presentation

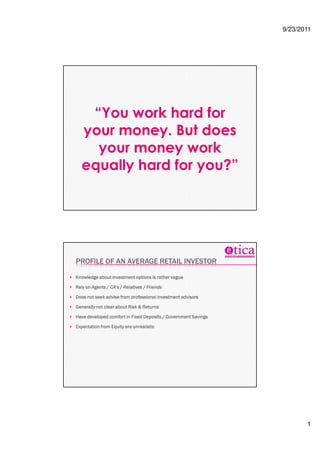

- 1. 9/23/2011 “You work hard for your money. But does your money work equally hard for you?” PROFILE OF AN AVERAGE RETAIL INVESTOR Knowledge about investment options is rather vague Rely on Agents / CA’s / Relatives / Friends Does not seek advise from professional investment advisors Generally not clear about Risk & Returns Have developed comfort in Fixed Deposits / Government Savings Expectation from Equity are unrealistic 1

- 2. 9/23/2011 Presentation on Financial Planning ÉTICA WEALTH MANAGEMENT PVT LTD GAJENDRA KOTHARI, CFA, CAIA, ICFA Vice- Vice-President & Head – Products (PMS division), UTI AMC Ltd. 7 yrs of work experience in the Financial Services Industry Currently responsible for Product designing and tying up with bank and distribution Channel in UTI PMS Chartered Financial Analyst (CFA) from CFA Institute, USA Chartered Alternative Investment Analyst (CAIA) from CAIA, Massachusetts International Certificate in Financial Advice (ICFA), London, UK Earlier roles - Institutional Sales (London – 3 yrs), Institutional Sales (Mumbai – 2yrs), Retail Sales (Mumbai – 2 years) Speaker at various investor forums on various personal finance topics 2

- 3. 9/23/2011 FEW HOUSEKEEPING REQUESTS… Not a Sales talk Would request you to participate enthusiastically No offence to any particular individual Mobile Silent “AN INVESTMENT IN KNOWLEDGE PAYS THE BEST INTEREST" - Benjamin Franklin 3

- 4. 9/23/2011 A COMMAN MAN’S CONCERN How can I grow and protect my financial wealth? How can I pay and manage my debt / liabilities (Good / Bad / Ugly) (EMIs)? How much should I save to be able to pay for my children’s education? How can I maximize the tax benefits which can be availed of? How can I save enough to be able to retire comfortably and maintain the current lifestyle? How can I meet emergency requirements / contingencies? How can I maximize what my heirs will inherit? LIFE STAGES Each individual is unique; so are his needs and wants; also, through out life, unique; wants; an individual’s needs and wants keep changing. changing. Therefore, financial planning process must first assess an individual at what stage of life he / she is in. in. Life stage is not a mechanical process based on some ‘age’ criteria but based on a number of milestones These milestones could be completion of formal education, first job and subsequent major job changes, major life events like marriage, birth of child, acquisition of major assets, education of children, marriages, separation, death etc 4

- 5. 9/23/2011 LIFE STAGES - MILESTONES Dependent till early 20s - Education & skill acquisition 20s Career beginners, enjoyers in 20 to 30 - first job / joining business, first vehicle, marriage & first child Career advancers in 30s - Young family, children in school, house purchase 30s Peak earners, achievers 40s - children in college, more savings and less 40s debts Pre retirees, empty nesters 50s - grown children, re-arrange financials in 50s re- preparation for retirement / starting on own etc Retired 60s - settled children, debts cleared, estate planning.. 60s planning.. 5

- 6. 9/23/2011 WHAT IS FINANCIAL PLANNING ? Financial planning is the process of successfully meeting financial needs of finances. life through the proper management of finances. “Big picture approach” It is more than just investment or tax or estate or retirement planning. It is planning. more. multi- all these and more. It is an integrated and multi-disciplinary approach balancing and fine tuning each of these components. components. It is also NOT an one time & one size fit all exercise recognizing each individual’s goals, desires, needs, experiences and expectations are different It is your roadmap to Financial Health, & Sustainable Wealth creation and to Freedom. achieve Financial Freedom. 6

- 7. 9/23/2011 FINANCIAL PLANNING PROCESS WHY YOU NEED FINANCIAL PLANNING? Life without Financial planning is like Unplanned Vacation. Vacation. If you wish to achieve your financial goals successfully & peacefully you must plan your financial life. life. 7

- 8. 9/23/2011 PROBLEMS OF RANDOM INVESTMENT Wrong selection - flavor of the month. Wrong timing - mostly near top. Short term investment. Inadequate investment. WHY IS IT IMPORTANT, THE INDIA CONTEXT Few major socio economic changes which make personal financial planning more critical in the Indian context Absence of any kind of social security for vast majority of people Increased longevity due to improved medical care AND ever increasing medical costs Rapidly decreasing career span; retirement (voluntary or otherwise) age is span; falling Gradually (dramatically?) reducing joint / extended family system More market driven and globalized Indian economy; more choices and more economy; risks 8

- 9. 9/23/2011 WHO NEEDS FINANCIAL PLANNING? Whatever may be level of your income or assets, you planning. need financial planning. It is myth that only rich people need financial planning. planning. CURRENT STATUS & GOAL SETTING Find out the net saving available for investment. investment. Wealth accumulated till today. today. What is your intention of investment (goal setting)? Simply put, How much money you need? & When you need the money? (Time horizon) Specific financial goals are vital to financial planning. planning. 9

- 10. 9/23/2011 FINANCIAL GOALS - EXAMPLES Mandatory Goals: Children education Children marriage – Not major in the USA Retirement Planning. Purchase of residential premises. Purchase of vehicle. Short term Goals 1- : 1-2 years. Medium term goals 3- : 3-5 years. Optional Goals: Long term goals 5- : 5-10 years. Up gradation of Residence. Distant goals 15- : 15-20 years. Luxury Car. Purchase of Luxury items at Home. Vacation Abroad. Charity - Religious or Social. Inheritance - Estate planning. Early Retirement - Financial freedom. BEST PRACTICES goals. Set measurable goals. Understand the effect your financial decisions have on other financial issues. issues. Revaluate your financial plan periodically. periodically. Start now. Do not assume that financial planning is for when you are older. now. older. Start with what you have got. Do not assume that financial planning is for the got. wealthy. wealthy. Take charge. You should be in control of the financial planning process. charge. process. Look at the bigger picture. Financial planning is more than retirement planning or tax picture. planning. planning. Do not confuse financial planning with investing. investing. Do not wait for a money crisis to begin financial planning. planning. 10

- 11. 9/23/2011 WHAT IS COMPREHENSIVE FINANCIAL PLANNING ? Comprehensive financial planning uses an integrated approach to monitor all aspects of someone’s financial situation: - Insurance & Risk Planning - Goal Based & Retirement Planning - Investment Planning - Tax Planning - Estate Planning Investment Planning 11

- 12. 9/23/2011 SAVING AND INVESTMENT Everyone needs to save for a rainy day. Once you have saved day. enough to take care of emergencies, you should start thinking about investing and to make your money grow. grow. Investment planning focuses on identifying effective investment strategies according to an investor’s risk appetite and financial goals. goals. There is a wide variety of investment options, including Equities, Bonds, Gold, Mutual funds, Bank Deposits, Real Estate, Commodities and Derivatives. WHY INVESTMENT PLANNING Investment Planning is important because it helps you to derive the maximum benefit from your investments. investments. Your success as an investor depends upon your ability to choose the right investment options. This, in turn, depends on options. your requirements, needs and goals. goals. Investment Planning also helps you to decide upon the right investment strategy. Besides your individual requirement, your strategy. investment strategy would also depend upon your age, personal circumstances and your risk appetite. appetite. 12

- 13. 9/23/2011 BASICS OF INVESTMENT PLANNING 13

- 14. 9/23/2011 LET TIME AND COMPOUNDING WORK FOR YOU... POWER OF COMPOUNDING? Which option will you chose from below? 1. Receiving Rs 1,00,00,000.00 2. Receiving double the money than previous day i.e Rs 1,2,4,8,16,32……so on for a month 14

- 15. 9/23/2011 POWER OF COMPOUNDING? How much will you get at the end of month? 1. Rs 30,00,00,000.00 2. Rs 1,07,37,41,823.00 15

- 16. 9/23/2011 16

- 17. 9/23/2011 IS THERE ANY SOLUTION TO OVERCOME THIS PROBLEM? EVEN LOW INFLATION WILL TREBLE COST OF LIVING Inflation rate assumed is 4.5% per annum in line with RBI’s comfort range. Source: Sundaram BNP Paribas AMC 17

- 18. 9/23/2011 LIFESTYLE INFLATION – A TIME BOMB 5 years back Today % increase Ordinary Shoes – Rs 500 Red Tape shoes – Rs 3000 500% Titan Watch – Rs 1500 Tommy Hilfilger – Rs 7500 400% Restaurant – Rs 1000 Fine Dining – Rs 5000 400% Medicine – Rs 500 No Limit ---- School fees – Rs 5000 DPS fees – Rs 1,00,000 1800% Didn’t exist I Pod – Rs 15,000 ---- Normal mobile – Rs 3,000 I-phone – Rs 30,000 900% Scooter / MC – Rs 50,000 Sedan Car – Rs 8,00,000 1500% 2 BHK 3 BHK with SP, Club etc No Comparison Marriage, Foreign vacation & more……. Inflation X Multiply by 5 members - !!!!!!!!!!! Maid - Washing Machine, Driver - Tata Nano Narayana Murthy Driver WEALTH CREATION IN DIFFERENT ASSET CLASSES Today not investing in Equity is Risky Figures as of April 2010 Rs 1000-a-month invested in Equity is an investment made in Sensex Source: Sundaram BNP Paribas AMCc 18

- 19. 9/23/2011 WHO’S THE BEST ??? Asset Class 1 Year 3 Year 5 Year 10 Year 15 Year 20 Year 30 Year Silver 115.54% 29.77% 48.49% 24.24% 13.63% 12.11% 3.79% Gold 36.82% 14.46% 38.25% 13.98% 9.06% 6.97% 0.35% Sensex 10.94% 7.52% 11.51% 18.36% 12.40% 15.10% 17.04% Bonds 6.00% 8.00% 8.00% 10.00% 12.00% - - Figures as of March 31, 2011 19

- 20. 9/23/2011 ASSET ALLOCATION IS THE KEY 20

- 21. 9/23/2011 21

- 22. 9/23/2011 STARTING EARLY & INVESTING REGULARLY Source: Sundaram BNP Paribas AMC 22

- 23. 9/23/2011 TIME MATTERS, NOT TIMING Source: Sundaram BNP Paribas AMC 23

- 25. 9/23/2011 INVESTMENT OPTIONS Real Returns(-) = Returns (9%) - Tax (20%) - Inflation (8-9%) ROLLING RETURN OF SENSEX Date Sensex 1 Year 2 Years 3 Years 5 Years 10 Years 15 Years Dec-79 118.76 Dec-80 148.25 24.83 Dec-81 227.72 53.61 38.47 Dec-82 235.83 3.56 26.13 40.92 Dec-83 252.92 7.25 5.39 30.62 Dec-84 271.87 7.49 7.37 9.26 18.02 Dec-85 527.36 93.98 44.40 49.54 28.89 Dec-86 524.45 -0.55 38.89 44.00 18.16 Dec-87 442.17 -15.69 -8.43 27.53 13.40 Dec-88 666.26 50.68 12.71 12.40 21.38 Dec-89 778.64 16.87 32.70 21.85 23.42 20.69 Dec-90 1048.29 34.63 25.44 53.97 14.73 21.60 Dec-91 1908.85 82.09 56.57 69.26 29.48 23.69 Dec-92 2615.37 37.01 57.95 83.27 42.69 27.20 Dec-93 3346.06 27.94 32.40 78.66 38.10 29.47 Dec-94 3926.9 17.36 22.53 43.43 38.21 30.61 26.27 Dec-95 3110.49 -20.79 -3.58 9.06 24.30 19.42 22.50 Dec-96 3085.2 -0.81 -11.36 -3.98 10.08 19.39 18.98 Dec-97 3658.98 18.60 8.46 -3.47 6.95 23.53 20.06 Dec-98 3055.41 -16.50 -0.48 -0.89 -1.80 16.45 18.07 Dec-99 5005.82 63.83 16.97 27.38 4.97 20.45 21.43 Dec-00 3972.12 -20.65 14.02 4.19 5.01 14.25 14.41 Dec-01 3262.33 -17.87 -19.27 3.33 1.12 5.51 12.96 Dec-02 3377.28 3.52 -7.79 -17.86 -1.59 2.59 14.52 Dec-03 5838.96 72.89 33.78 21.24 13.83 5.73 15.57 Dec-04 6602.69 13.08 39.82 42.26 5.69 5.33 15.32 Dec-05 9397.93 42.33 26.87 66.81 18.80 11.69 15.75 Dec-06 13786.91 46.70 44.50 53.66 33.41 16.15 14.09 Dec-07 20286.99 47.15 46.92 75.29 43.13 18.68 14.63 Dec-08 9647.31 -52.45 -16.35 1.32 10.56 12.18 7.31 Dec-09 17464.81 81.03 -7.22 12.55 21.48 13.31 10.46 Dec-10 20509.09 17.43 45.80 0.36 16.89 17.84 13.40 Yearly Rolling Returns 31 30 29 27 22 17 Positive Returns 23 22 25 25 22 17 Negative Returns 8 8 4 2 0 0 25

- 26. 9/23/2011 SENSEX RETURNS - 17.06% P.A SMALL VS MID VS LARGE 26

- 27. 9/23/2011 AXIS BANK - 47.45% P.A SBI BANK - 27.06% P.A " A SBI Fixed Deposit doubles your money in 10 years. Had you invested the same money in SBI stock, it would have given you 1800% returns" 27

- 28. 9/23/2011 BHARTI AIRTEL - 37.07% P.A BHEL - 21.61% P.A 28

- 29. 9/23/2011 ONGC - 13.83% P.A INFOSYS - 57.36% P.A 29

- 30. 9/23/2011 MUTUAL FUND AS AN INVESTMENT VEHICLE INDEX 1. Mutual Fund Concept 2. Organization of a Mutual Fund 3. Advantages / Disadvantages of Mutual Funds 4. Types of Mutual Fund Schemes 5. Mutual Fund Investment Strategies 6. Mutual Funds Vs. Direct Equity Investments 7. Worldwide MF Industry 8. Mutual Funds - Performance 9. Mutual Fund Investment Blunders 10. Mutual Funds Taxation 30

- 31. 9/23/2011 MUTUAL FUND OPERATION FLOW CHART CONCEPT A Mutual Fund is a trust that pools the savings of a number of investors who share a common financial goal. goal. The money thus collected is then invested in capital market instruments such as shares, debentures and other securities. securities. The income earned through these investments and the capital appreciation realized are shared by its unit holders in proportion to the number of units them. owned by them. Thus a Mutual Fund is the most suitable investment for the common man as it offers an opportunity to invest in a diversified, professionally managed cost. basket of securities at a relatively low cost. 31

- 32. 9/23/2011 MUTUAL FUNDS = PACKAGED ATTA or FUND STRUCTURE Fund Sponsor Trustees Asset Management Company R&T Agent Custodian 32

- 33. 9/23/2011 SBI MUTUAL FUND Mutual Fund Trust SBI Mutual Fund Sponsor State Bank of India Trustee SBI Mutual Fund Trustee Company Private Limited AMC SBI Funds Management Private Limited Custodian HDFC Bank Limited, Mumbai Citibank N.A., Mumbai Stock Holding Corporation of India Ltd., Mumbai Bank of Nova Scotia (custodian for Gold) RTA Computer Age Management Services Pvt. Ltd 33

- 34. 9/23/2011 ADVANTAGES OF MUTUAL FUNDS Professional Management Diversification Potential Higher Return Vs other Avenues Low Costs Liquidity Transparency Flexibility Choice of schemes Tax benefits Well regulated DISADVANTAGES OF MUTUAL FUNDS Management fees Exit Costs Potential poor performance Complicated tax reporting issues Potential market risk with all investments Aggressive or unethical sales personnel / practices - 90% of the reason why investors stay away from Mutual Funds 34

- 35. 9/23/2011 REALITY CHECK…. In a country with a population of close to 120 crores, we at best have about 1 crore investors – less than 1% ! (even that is suspect) 4-5 crore mutual funds investors a myth; these are folios that belong to about 60-70 lakh active unique investors Households’ investments in capital market have fallen from a high 23.3% of gross financial savings in 1991-92 to a meagre 2.6% in 2008-09! HOUSEHOLD SAVINGS - WHERE’S THE MONEY PARKED? 35

- 36. 9/23/2011 DECLINING INVESTMENTS IN CAPITAL MARKET INVESTMENTS / SAVINGS OF THE HOUSEHOLD SECTOR (GROSS) IN CAPITAL MARKET (Per cent) # Preliminary P Provisional Source: SEBI HANDBOOK OF STATISTICS ON THE INDIAN SECURITIES MARKET 2009 THANKS TO MR C B BHAVE Mr U K Sinha, SEBI Chairman 36

- 37. 9/23/2011 TYPES OF SCHEMES By Structure Open Ended Schemes Close Ended Schemes By Investment Objectives Growth Schemes Income Schemes Balanced Schemes Money Market Schemes Other Schemes Tax Saving Schemes Special Schemes Index Schemes Sector Specific Schemes ETFs (including gold ETFs) Fund of Funds RISK-RETURN TRADEOFF Siamese Twins 37

- 38. 9/23/2011 EQUITY Scoreboard – Hybrid & Debt schemes 38

- 39. 9/23/2011 HOW DO MUTUAL FUNDS HELP YOU ? SHORT TERMACCOUNT SAVINGS DEBT FUNDS FIXED DEPOSITS FMPS Mutual Banks SIPS CURRENT ACCOUNT LIQUID FUNDS RECURRING DEPOSITS Funds LIEN LOAN AGAINST SHARES EQUITY //COMMODITY TRADING EQUITY COMMODITY FUNDS 39

- 40. 9/23/2011 COMPUTING NET ASSET VALUE For investors, the performance of their investment depends on what happens to the fund’s per unit value, or net asset value (NAV) NAV = Market Value of Assets – Liabilities Number of Shares Outstanding MUTUAL FUND INVESTMENT STRATEGIES Choose in funds consistent with your objectives, constraints, and tax situation Invest. Don’t speculate. (Stock market is not a casino) Be regular Own funds in different asset classes Do your homework or hire wise experts to help you. Monitor your investments at a regular interval. Remember, no investment is forever. Don’t panic. 40

- 41. 9/23/2011 DIRECT EQUITY VS MUTUAL FUNDS Diversification Professional Management Transaction costs Convenience / No demat account required Blue Chip portfolio for as low as Rs. 500 High Service Standards Transparency WORLDWIDE MUTUAL FUND ASSETS Worldwide MF Assets in Rs 1,097,00,000 crs (31st Dec’10) India MF Assets in Rs. 7,00,538 crs (31st Mar’11) 0.63% of the worldwide MF assets 1 USD = Rs 44.40 as at Mar 31, 2011 (trillions of U.S. dollars, end of Dec 2010) Source: Investment Company Institute 41

- 42. 9/23/2011 US LEADS THE WORLD MUTUAL FUND MARKET WORLDWIDE MF ASSETS BY TYPE OF FUND Data as of Dec 2010 Source: Investment Company Institute 42

- 43. 9/23/2011 FACTORS TO CONSIDER FOR CHOOSING A FUND Track record / experience of the fund house Stability of the investment team / adherence to an investment process Consistent performance of the fund across market cycles Disclosure and service levels offered by the fund house Relative performance among its peer group (across time periods) Investment style (whether it suits your risk profile) Look for Expense Ratio, Exit load etc PERFORMANCE OF DIVERSIFIED EQUITY FUNDS Sensex 9.77 32 7.51 22 11.47 16 Performance as at March 31, 2011 43

- 44. 9/23/2011 PERFORMANCE OF TAX-SAVING EQUITY FUNDS Sensex 9.77 16 7.51 14 11.47 8 Performance as at March 31, 2011 PERFORMANCE OF BALANCED FUNDS Performance as at March 31, 2011 44

- 45. 9/23/2011 INVESTMENT MODES Systematic Investment Plan (SIP) Invest a fixed sum every month. (6 months to 10 years- through post-dated cheques or Direct Debit facilities) Fewer units when the share prices are high, and more units when the share prices are low. Average cost price tends to fall below the average NAV. Systematic Transfer Plan (STP) Invest in debt oriented fund and give instructions to transfer a fixed sum, at a fixed interval, to an equity scheme of the same mutual fund. Systematic Withdrawal Plan (SWP) PATH TO BUILDING YOUR PORTFOLIO 45

- 46. 9/23/2011 SYSTEMATIC INVESTMENT PLANNING (SIP) A long journey begins with a small step DIFFERENCE IN APPROACH Earn (Rs 1 lakh) Earn (Rs 1 lakh) Spend (???) Save (Rs 20,000) Save (???) Spend (Rs 80,000) 46

- 47. 9/23/2011 47

- 48. 9/23/2011 Rs 18 lakhs investment in SENSEX growing to Rs 3.46 crores in 30 years 48

- 49. 9/23/2011 SIP CALCULATIONS My retirement portfolio at the end of my 50th Birthday Atleast 15 crores Monthly pension Rs 12 lakhs SIP CALCULATIONS Monthly Amount Rs 50,000 Rs 1,00,000 My Period 10 years 10 years retirement Total Investment Rs 60,00,000 Rs 1,20,00,000 portfolio at Return @15% Rs 1,37,60,852 Rs 2,75,21,705 the end of my Return @20% Rs 1,88,04,764 Rs 3,76,09,529 55th Birthday Period 25 years 25 years Total Investment Rs 1,50,00,000 Rs 3,00,00,000 Atleast Return @15% Rs 16,21,76,480 Rs 32,43,52,961 85 crores Return @20% Rs 42,42,64,335 Rs 84,85,28,670 You earn regularly, You spend regularly, Why not invest regularly? 49

- 50. 9/23/2011 50

- 51. 9/23/2011 51

- 52. 9/23/2011 52

- 53. 9/23/2011 GOAL - ADITI’S EDUCATION Current investment – Rs 10,000 p.m Tenure – 25 years Expected Rate of return – 18% Aditi’s estimated wealth on her 25th Bday – Rs 5,82,33,121 GOAL - ADITI’S MARRIAGE Current investment – Rs 10,000 p.m Tenure – 30 years Expected Rate of return – 18% Aditi’s estimated wealth on her 30th Bday – Rs 14,32,52,892 53

- 54. 9/23/2011 SIP VS STP 54

- 55. 9/23/2011 TWO GREATEST INVESTMENT BLUNDERS 1. Investing in the NFOs 2. Investing in the schemes which gives high dividends INVESTING IN NFOS Its new (Old wine in a new bottle, participate in India’s growth potential) Its at Rs 10 i.e its cheaper than a existing fund whose NAV is Rs.110 My friend / relative is buying it My distributor / agent has strongly recommended it. I can make good profit in the short term 55

- 56. 9/23/2011 RS.10 OR RS.100 - NAV MAKES NO DIFFERENCE DOES NAV MATTER? 56

- 57. 9/23/2011 DON'T FALL FOR THE DIVIDEND BAIT The NAV falls to the extent of dividend payout Expense incurred on advertisement campaigns for spreading the word goes from your fund If the basis of investing in a scheme is flawed, so is the investment MF EXPENSES Initial Issue Expenses : One time expense Born by the AMC Earlier 6% charged to the scheme Recurring Expenses : These can be charged to the scheme. 57

- 58. 9/23/2011 FEES SEBI has stipulated the following annual limits on recurring expenses (including management fees) for schemes other than index schemes: Avg weekly New asset Max Expenses for Max Expenses for Crore) (Rs Crore) Equity Scheme Debt Scheme First 100 2.5% 2.25% Next 300 2.25% 2% Next 300 2% 1.75% Above 700 1.75% 1.5% The management fees cannot exceed : 1.25% on the first Rs 100 crore of net assets of a scheme 1.00% on the balance net assets FEES BREAK-UP Fees of various service providers, such as Trustees, AMC, Registrar & Transfer Agents, Custodian, & Auditor fees Selling expenses including scheme advertising and commission to the distributors Expenses on investor communication, account statements, dividend / redemption cheques / warrants Listing fees and Depository fees Service tax Expenses cannot be charged to the scheme Penalties and fines for infraction of laws. Interest on delayed payment to the unit holders. Legal, marketing, publication and other general expenses not attributable to any scheme(s). Expenses on general administration, corporate advertising and infrastructure costs. 58

- 59. 9/23/2011 MF TAXATION Short Term Capital Long Term Capital Gain Tax Gain Tax Mutual Funds (holding period (holding period > < 12 months) 12months) Equity 15%* Nil As per your tax slab 10% / 20%* Debt *Additional education cess of 3% on the amount of tax $ Additional surcharge of 5% and an education cess of 3% on the amount of tax % WARNING SIGNALS Fund's management changes Performance slips compared to similar funds. Fund's expense ratios climb Independent rating services reduce their ratings of the fund. Change in management style or a change in the objective of the fund / Scheme Mergers. 59

- 60. 9/23/2011 BUYING MUTUAL FUNDS Contacting the Asset Management Company directly Web Site Branch Offices Mutual Fund Agents / IFAs Locate one on AMFI site Financial Planners ASK Wealth Sykes & Ray FP, IMM, Parag Parikh FAS National Distributors Birla Sunlife, Bajaj Capital, India Infoline Banks Net-Banking Branch Banking / Relationship Managers ATMs Online Platform Fund Supermart, ICICI Direct, Motilal Oswal, Indiabulls KEEPING TRACK… Filling up an application form and writing out a cheque = end of the story… NO! Periodically evaluate performance of your funds Fact sheets and Newsletters Websites Newspapers Professional advisor 60

- 61. 9/23/2011 Mutual Fund investments are subject to market risks. Please read the SID and SAI carefully and consult your financial advisor before investing. SOURCE Sundaram BNP Paribas Mutual Fund Religare Mutual Fund UTI Mutual Fund ICICI Prudential Mutual fund www.valueresearchonline.com www.outlookmoney.com Fidelity Mutual Fund The Finance Literates blog Bloomberg 61

- 62. 9/23/2011 62

- 63. 9/23/2011 THANK YOU For any further information, please contact: Mr. Gajendra Kothari, CFA, CAIA, ICFA M:+91 90043 89883 E: gajendra.kothari @eticawealth.com Ética Wealth Management Private Limited 501, T-39 Sunshine Building, Shastri Nagar, Lokhandwala Complex Road, Andheri West, Mumbai - 400 053 Landmark: Suburban Diagnostics, Near Lokhandwala Circle T: +91 22 2632 9644 +91 22 4264 8740 E: info@eticawealth.com 63