Booking open Available Pune Call Girls Wadgaon Sheri 6297143586 Call Hot Ind...

Investment Idea: Garden Silk Mills Limited - HOLD

1. December 31, 2010

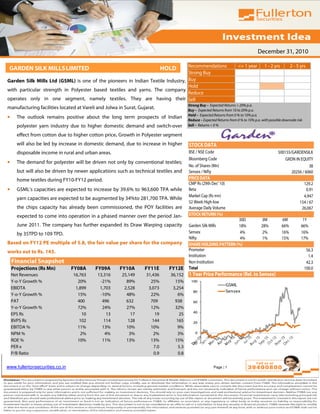

Recommendations <= 1 year 1 - 2 yrs 2 - 5 yrs

GARDEN SILK MILLS LIMITED HOLD

Strong Buy

Garden Silk Mills Ltd (GSML) is one of the pioneers in Indian Textile Industry, Buy

Hold

with particular strength in Polyester based textiles and yarns. The company

Reduce

operates only in one segment, namely textiles. They are having their Sell

Strong Buy – Expected Returns > 20% p.a.

manufacturing facilities located at Vareli and Jolwa in Surat, Gujarat. Buy – Expected Returns from 10 to 20% p.a.

Hold – Expected Returns from 0 % to 10% p.a.

• The outlook remains positive about the long term prospects of Indian

Reduce – Expected Returns from 0 % to 10% p.a. with possible downside risk

polyester yarn industry due to higher domestic demand and switch-over Sell – Returns < 0 %

effect from cotton due to higher cotton price. Growth in Polyester segment

will also be led by increase in domestic demand, due to increase in higher STOCK DATA

disposable income in rural and urban areas. BSE / NSE Code 500155/GARDENSILK

Bloomberg Code GRDN IN EQUITY

• The demand for polyester will be driven not only by conventional textiles;

No. of Shares (Mn) 38

but will also be driven by newer applications such as technical textiles and Sensex / Nifty 20256 / 6060

home textiles during FY10-FY12 period. PRICE DATA

CMP Rs (29th Dec' 10) 129.2

• GSML’s capacities are expected to increase by 39.6% to 963,600 TPA while Beta 0.91

Market Cap (Rs mn) 4,947

yarn capacities are expected to be augmented by 34%to 281,700 TPA. While

52 Week High-low 154 / 67

the chips capacity has already been commissioned, the POY facilities are Average Daily Volume 26,067

expected to come into operation in a phased manner over the period Jan- STOCK RETURN (%)

30D 3M 6M 1Y

June 2011. The company has further expanded its Draw Warping capacity Garden Silk Mills 18% 28% 66% 66%

by 35TPD to 109 TPD. Sensex 4% 2% 16% 16%

Nifty 4% 1% 15% 17%

Based on FY12 PE multiple of 5.8, the fair value per share for the company SHARE HOLDING PATTERN (%)

works out to Rs. 143. Promoter 56.3

Institution 1.4

Financial Snapshot Non Institution 42.3

Projections (Rs Mn) FY08A FY09A FY10A FY11E FY12E Total 100.0

Net Revenues 16,763 13,316 25,149 31,436 36,152 1 Year Price Performance (Rel. to Sensex)

Y-o-Y Growth % 20% -21% 89% 25% 15% 100

GSML

EBIDTA 1,899 1,703 2,528 3,073 3,254

80 Sensex

Y-o-Y Growth % 15% -10% 48% 22% 6%

PAT 400 496 632 709 938 60

Y-o-Y Growth % 72% 24% 27% 12% 32%

40

EPS Rs 10 13 17 19 25

BVPS Rs 102 114 128 144 165 20

EBITDA % 11% 13% 10% 10% 9%

NPM % 2% 4% 3% 2% 3% 0

ROE % 10% 11% 13% 13% 15%

-20

PER x 7.0 5.3

P/B Ratio 0.9 0.8

www.fullertonsecurities.co.in Page | 1

2. December 31, 2010

BUSINESS PROFILE

Garden Silk Mills Ltd. occupies a leadership position in the manufacturing of Polyester Filament Yarn (PFY)-

GSML is market leader

based textiles in India. It is the largest manufacturer of PFY-based fabrics in the country. It is also the leading in polyester chips

market with a market

manufacturer of fully drawn flat filament yarn and textile-grade chips.The company's products and services

share of 38%

include textiles, which includes yarn (including partially oriented yarn and processed yarns), cotton, polyester,

silk, fabrics, georgettes, chiffons, faille’s and jacquards. Their apparel section includes Vareli business shirts and

ready-to-wear women garments. Additionally the company is also the second largest specialty yarn maker and

the largest specialty chip maker in India.

GSML is market leader in polyester chips market with a market share of 38%. The company ’ s chip

manufacturing facilities are located at Surat (Gujarat), which accommodates about 42% of India ’ s total

extruder base yarn manufacturing facilities. Furthermore, Silvassa, which contains additional 31% of the

capacity, is located in close proximity from Surat. This locational advantage gives GSML easy access to the end

consumers increasing its cost-efficiencies substantially. GSML’s impressive marketing network encompasses GSML has presence in

more than 70 dealers, 12 company owned depots and more than 290 authorized retail outlets including shops countries like USA, UK,

South Africa, and Gulf

and counters in over 65 cities in India. GSML fabrics are also available in a host of countries including Canada,

and is planning for

U.S.A., U.K., Indonesia, Malaysia, South Africa, Middle East and Gulf countries. future expansion

Revenue Break up FY10 Revenue (Rs mn) Segmentwise Revenue

6.30% 100%

5.67

Contribution

7.85 8.00

80%

42.54 Yarn to weaving

45.78 48.96 6% mills/looms

60%

Export

43%

40%

Chips to

Domestic 51%

42.76 42.35

50.93 independent POY

20%

players

0% Fabric to end

FY08 FY09* FY10 users

FY09* Revenue is for 9 months

93.70% Chips Yarn (POY & Processed yarn) Fabrics Others

Industry Outlook

Globally synthetic fibers, led by polyester (polyester staple fiber and polyester filament yarn) have been The demand for

polyester filament yarn

growing rapidly owing to a growing demand for fiber and the continuing replacement of natural fibers in India grew by around

in a world short of agricultural acreage. In the last 15 years the total fiber consumption worldwide has 14% in 2009-10 and is

expected to grow at a

grown up from 47% to 57% while that of cotton have reduced from 42% to 32%. Moreover the CAGR of 6-7% in the

percentage of polyester in global synthetics market has gone up from 58% to 79% in this period. In India years to come

polyester has been steadily replacing natural fibers as well. According to industry reports India’s overall

textile and apparel industry is expected to touch $220 billion (Rs.9.9 trillion) by 2020 from $70 billion

now.

www.fullertonsecurities.co.in Page | 2

3. December 31, 2010

Textile Value Chain: Garden Silk Mills Ltd’s Business Model.

• Long term prospectus of polyester business remains positive; expected to grow by 7.0%. Reason being higher domestic

demand and switch-over effect from cotton due to higher cotton price.

• Raw materials prices are expected to remain stable despite rising crude oil prices .Purified Terephthalic Acid (PTA) &

Monoethylene Glycol (MEG) are the key raw materials for GSML.The prices of these raw materials, being crude derivatives

are more or less in tandem with the crude oil prices. The polyester players have moderate pricing flexibility, wherein

moderate and gradual increase in the feedstock prices can be eventually passed on to the consumers, but any sudden

upward spike in prices may have to be absorbed by the polyester yarn manufacturer. Industry reports say that even in

case of rising crude prices; the prices of these ram materials are expected to remain stable; reason being increase in

production capacities of PTA & MEG.

• Cotton yarn is a substitute for Polyester yarn. High cotton prices and low availability may lead to increase in cotton yarn

prices. This may prompt independent weaving mills/looms to shift their polyester-cotton (PC) from cotton yarn to

polyester yarn. In recent months the domestic prices have peaked to a life time high of Rs 100/kg due to strong demand

from China. The prices of cotton are expected to remain robust in near-to-medium term because of delay in cotton

deliveries due to heavy rains and secondly due to global demand exceeds its supply.

www.fullertonsecurities.co.in Page | 3

4. December 31, 2010

BUSINESS PERFORMANCE

Robust Revenue Growth…

Revenue in Q2FY11 grew 48.7% annually to Rs 9550.6mn due to increase in exports which stood at 6.3%. This GSML is also putting

up a coal based

was basically due to increase in demand for polyester from China, and secondly due to increase in international thermal power

cotton prices. Net profit for FY 2009-10 stood at 252.7mn, an increase of 148% on Y-o-Y basis. project of 18 MW at

Jolwa expected to

Tax payment for Q2FY11 increased by 40.9% to 65.2mn due to deferred tax adjustments. EBITDA margins stood commence power

generation before

at 8.08% as compared to 8.3% for Q2FY10. This erosion was due to high raw material prices and employee March, 2011

expenses. PAT margins stood at 4.9% for Q2FY11 as against 1.7% Q2FY10.

Revenue, Operating & PAT Margin Quarterly Performance

40,000 10% 10000 12%

35,000 9% 9000

8% 8000 10%

30,000

7% Revenues (Rs mn) 7000 8%

Margins(%)

25,000 6% 6000

20,000 5% 5000 6%

4% 4000

15,000 3000 4%

3%

10,000 2000 2%

2%

5,000 1000

1% 0 0%

- 0%

FY08 FY09 FY10 FY11E FY12E

Revenue (Rs Mn) EBIDTA Margin PAT Margin Net Revenue (Rs mn) EBITDA Margins

Peer Group Comparison

EBIDTA PAT

Revenue P/E P/B CMP FV

Companies Margin Margin ROE (%)

(Rs. mn) (x) (x) (Rs.) (Rs.)

(%) (%)

Garden silk 25,149 10% 1% 13% 7.8 1.0 129 10

JBF 49,409 10% 4% 24% 5.4 1.3 179 10

Century Enka 12,309 18% 8% 18% 4.2 0.7 196 10

*FY10 Consolidated figures

Peer Comparison

Compared to Garden Silk; Century Enka is operating at higher EBITDA margins mainly on account of lower Q2FY11 witnessed

raw material prices. The raw materials cost pressures, owing to higher international crude prices, have higher revenue &

profitability growth

impacted the FY10 profitability of GSML. The recent strong quarterly result indicates strong profitability due

to passing on of raw material costs to customers. However with strong expansion program planned ahead;

we do expect the margin pressures to alleviate in future.

www.fullertonsecurities.co.in Page | 4

5. December 31, 2010

VALUATION

We expect GSML’s revenues grow at a CAGR of 20% over FY2010-12 to Rs 38bn by FY2012. We further

Based on FY12 PE

estimate that the PAT would grow by 22% in FY2012. multiple of 5.8, the fair

Based on FY12 PE multiple of 5.8, the fair value per share for the company works out to Rs. 143. value for the company

works out to Rs. 143

We recommend a ‘HOLD’ rating on the stock.

Financial Analysis and Projections

Particulars (Rs Mn) FY08A FY09A FY10A FY11E FY12E

Net Revenue 16,763 13,316 25,149 31,436 36,152

Other Income 196 156 204 314 362

Total Income 16,958 13,472 25,353 31,751 36,513

Operating Expenditure 15,059 11,769 22,825 28,678 33,260

Depreciation 574 448 726 999 949

EBIT 1,325 1,255 1,803 2,073 2,304

EBIT Margin (%) 8% 9% 7% 7% 6%

Interest 638 555 872 1,031 925

Profit Before Tax 687 700 931 1,042 1,380

Less: Tax 287.4 204.1 298.9 333.6 441.5

Profit After Tax 400 496 632 709 938

PAT Margin (%) 2% 4% 3% 2% 3%

ROE (%) 10% 11% 13% 13% 15%

EPS (Rs) 10 13 17 19 25

BVPS (Rs) 102 114 128 144 165

Valuation Ratios (x) FY11E FY12E

P/E 7.0 5.3

P/B 0.9 0.8

www.fullertonsecurities.co.in Page | 5

6. December 31, 2010

Board of Directors

Director Name Current Position Description

Mr. Alok P. Shah is Joint Managing Director and Executive Director of Garden Silk Mills Ltd. He holds B.S. (Stanford

Managing Director University) M.B.A. (University df Chicago, USA). Directorship held in other Public Limited Companies (excluding foreign and

Mr. Alok P. Shah and Executive private companies) are: Garden Finmark Umited Inita PowerCompany Limited Palomarlextiles Limited Bijlee Textiles

Director Limited Jarigold Textiles Limited Rosekamal Textile Umited Wheel &AxleTextiles Limited Amichand Textile Limited

PashahTextiles Umited SPS Silk Limited Prabhat Silk Mills Limited VareliTrading Company Limited.

Mrs. Shilpa P. Shah is Executive Director of Garden Silk Mills Ltd. She holds M,A. (University of California, USA). She is an

Mrs. Shilpa P. Shah Executive Director Industrialist. Directorship held in other Public Limited Companies (excluding foreign and private companies) are: Prabhat

Silk Mills Umited, SuratTextile Mills Limited.

Mr. Sanjay S. Shah is Executive Director of Garden Silk Mills Ltd. He is B.A. from Essex University, U.K. and has experience in

Mr. Sanjay S. Shah Executive Director the field of Yarn Preparatory and Weaving. He possesses experience in overall business management particularly with

regard to textile industry and has more than 16 years of experience in Senior Corporate Management.

Mr. Suhail P. Shah is Executive Director of Garden Silk Mills Ltd. He holds a Post Graduate in Physical Chemistry from The

University of Chicago and a Doctorate in Theoretical Physical Chemistry from The University of Chicago. Mr. Shah has to his

credit various research accomplishments, computational skills and publications at the international level. He has more

Mr. Suhail P. Shah Executive Director

than 10 years of experience in research with various universities of international repute. Mr. Shah has supported the

Company and contributed suggestions in identifying international suppliers, carrying out technical appraisal with them for

finalising the Continuous Polymerisation {CP) Chips Project of the Company.

Mr. Rajen P. Shah is Non-Executive Director of Garden Silk Mills Ltd. He holds M.S. (University of California, USA).

Non-Executive

Mr. Rajen P. Shah Directorship held in other Public Limited Companies (excluding foreign and private companies) are: Surabhi Chemicals &

Director

Investments Limited.

Non-Executive Mr. Yatish C. Parekh is Non-Executive Independent Director of Garden Silks Mills Ltd. He holds B.Com and FCA. His

Mr. Yatish C.

Independent Directorship held in other Public Limited Companies (excluding foreign and private companies) are Surabhi Chemicals &

Parekh

Director investments Limited.

www.fullertonsecurities.co.in Page | 6