09-03-31 Web 2.0 Weekly

•

2 gefällt mir•527 views

- The first quarter of 2009 saw a rebound in financing for web 2.0 companies, with $521 million invested across 77 financings, up 54% from the previous quarter but down 44% from the first quarter of 2008. - Video and social networking sectors attracted the most investment in the quarter, with Twitter raising the most of any single company at $35 million. - The document identifies 90 public web 2.0 companies, with a total market cap of $34.8 billion, and provides a table comparing various financial metrics like revenue, market cap, employees and valuation for these companies.

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Andere mochten auch

Ähnlich wie 09-03-31 Web 2.0 Weekly

Ähnlich wie 09-03-31 Web 2.0 Weekly (18)

Mehr von David Shore

Mehr von David Shore (13)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

09-03-31 Web 2.0 Weekly

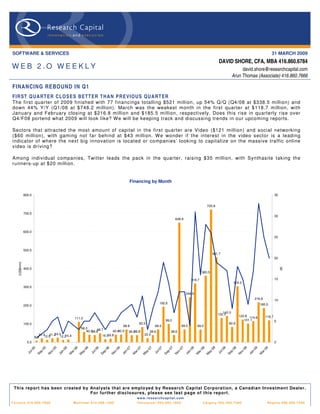

- 1. SOFTWARE & SERVICES 31 MARCH 2009 DAVID SHORE, CFA, MBA 416.860.6784 WEB 2.O WEEKLY david.shore@researchcapital.com Arun Thomas (Associate) 416.860.7666 FINANCING REBO UND IN Q1 F IR ST Q UA RT E R CL O S E S B ET T E R T HA N P R E VI OU S QU A RT ER The first quarter of 2009 finished with 77 financings totalling $521 million, up 54% Q/Q (Q4/08 at $338.5 million) and down 44% Y/Y (Q1/08 at $748.2 million). March was the weakest month in the first quarter at $118.7 million, with January and February closing at $216.8 million and $185.5 million, respectively. Does this rise in quarterly rise over Q4/F08 portend what 2009 will look like? W e will be keeping track and discussing trends in our upcoming reports. Sectors that attracted the most amount of capital in the first quarter are Video ($121 million) and social networking ($60 million), with gaming not far behind at $43 million. W e wonder if the interest in the video sector is a leading indicator of where the next big innovation is located or companies’ looking to capitalize on the massive traffic online video is driving? Among individual companies, Twitter leads the pack in the quarter, raising $35 million, with Synthasite taking the runners-up at $20 million. Financing by Month 800.0 35 720.8 700.0 30 649.9 600.0 25 500.0 461.7 20 (US$mm) (#) 400.0 360.5 15 318.7 304.3 300.0 244.0 216.8 10 192.6 185.5 200.0 142.0 132.3 122.8 114.6 118.7 111.0 101.1 99.0 5 82.6 82.5 100.0 69.5 68.8 69.0 69.0 56.3 40.5 48.7 42.0 38.0 40.9 38.8 38.8 38.6 38.6 24.4 22.0 21.4 21.2 18.8 16.5 15.4 12.5 12.2 8.0 0.0 0 5 6 6 7 7 8 8 05 06 6 06 07 7 07 08 8 08 09 9 5 6 7 8 -0 -0 -0 -0 -0 -0 -0 -0 -0 -0 -0 l-0 l-0 l-0 l-0 p- n- p- n- p- n- p- n- ov ay ov ay ov ay ov ar ar ar ar Ju Ju Ju Ju Se Ja Se Ja Se Ja Se Ja M M M M N M N M N M N This report has been created b y Anal ysts that are emplo yed b y Research Capital Corporation, a Canadian Investment Dealer. For further disclosures, please see last page of this report. w w w . r e s e a rc h c a p i t a l . c o m T o ro n t o 4 1 6 . 8 6 0 . 7 6 0 0 Montreal 514.399.1500 Vancouver 604.662.1800 Calgary 403.265.7400 Regina 306.566.7550

- 2. Page 2 THE WEB 2.0 UNIVERSE Ninety public Web 2.0 companies identified: Our W eb 2.0 universe contains 90 companies, with a combined market cap of $34.8 billion. These include a wide variety of companies, including MMOG (Massive Multi-Player Online Gaming) companies, social networking software companies, media sharing companies, and social lending companies. See below for a summary of the full universe (Figure 1). The average market cap for the group is ~$386 million (but a median of only $31 million), with average trailing revenue of $138.6 million (median $48 million). The companies are also generally profitable, with a median EBITDA margin of 16.4%. On a valuation basis, the overall average is 4.7x trailing revenue (median 1.3x) and 8.9x trailing EBITDA (median 6.6x). Twelve of the companies have more than 500 employees. C omparable C o mpany A nalys is > W eb 2.0 Trading Current U S D Market U S D LT M To tal US D L TM T otal E B ITDA TE V/LT M T E V/LT M C om pany Nam e L TM as of T ic ker E xc hang e Curr enc y H Q P ric e C ap ($m) R ev ($m) E B ITDA ($m) % R evenu e E B IT DA E mployees Acce le rize New Me dia, Inc. 9 /30 /200 8 AC LZ OT C B B US D U nited S ta tes 0 .35 9 .4 3.2 (4 .7) NM 4.3 x - 20 Actoz S oft C o., L td. 9 /30 /200 8 A0 527 90 K OS E KR W S outh K orea 11, 150 7 1.1 52. 9 9 .7 18 .3% 0.9 x 4.7x NA AQ Inte ractive , Inc. 1 2/31 /200 8 38 38 TSE J PY J apan 40 ,000 .00 2 2.4 62. 1 5 .0 8 .0% - - NA As s ocia ted Media H oldings Inc. 6 /30 /200 7 AS MH OT C P K US D U nited S ta tes 0 0 .1 0.1 (2 .3) NM 8.0 x - 3 B igstring Corp. 9 /30 /200 8 BS GC OT C B B US D U nited S ta tes 0 .02 0 .8 0.1 (2 .1) NM 29.8 x - 8 B e tawave Corpora tion 9 /30 /200 8 B W AV OT C B B US D U nited S ta tes 0 4 .4 6.3 (1 1.0) NM 2.4 x - 41 B e yond Commerce, Inc. 9 /30 /200 8 B Y OC OT C B B US D U nited S ta tes 0 .51 2 0.9 1.1 (7 .7) NM 21.8 x - 25 B right T hings plc 9 /30 /200 8 AIM:B G T AIM GBP U nited K ingdom 0 2 .5 0.2 (1 .6) NM 10.5 x - 9 B roa dW ebAs ia Inc. 9 /30 /200 8 BW BA OT C P K US D U nited S ta tes 0 .51 4 3.3 0.0 (4 .6) NM - - 46 C DC C orp. 9 /30 /200 8 C HIN.A N as da qG S US D H ong K ong 1 11 6.5 428 .1 1 8.8 4 .4% 0.4 x 9.2x 3 ,12 5 C hina G ate wa y C orpora tion 9 /30 /200 8 C GW Y OT C B B US D U nited S ta tes 0 .00 0 .0 6.7 (6 .6) -9 8.9% 0.0 x - 37 C hine s e G amer International 9 /30 /200 8 G T S M:308 3 GTSM TWD T aiwan 171 42 5.9 37. 8 1 7.8 47 .1% 9.8 x 2 0.8 x NA C ornerW orld C orporation 1 /31 /200 9 C WR L OT C B B US D U nited S ta tes 0 .14 6 .6 1.3 NM NM 6.1 x - NA D ADA S pA 9 /30 /200 8 C M:D A CM E UR Ita ly 5 10 1.2 223 .0 3 5.6 16 .0% 0.6 x 4.1x 574 D XN Holdings B hd 1 1/30 /200 8 D XN KL SE MY R Ma la ys ia 0 .30 1 8.8 76. 0 1 0.1 13 .3% 0.5 x 3.8x NA D ibz Inte rnational, Inc. NA D IB Z OT C P K US D U nited S ta tes 0 0 .0 NA NM NM - - NA D igitalP ost Inte ra ctive , Inc. 9 /30 /200 8 D G LP OT C B B US D U nited S ta tes 0 .01 0 .7 0.4 (3 .3) NM 3.9 x - 11 D igitalT own, Inc. 1 1/30 /200 8 DGT W OT C B B US D U nited S ta tes 3 6 7.9 NM (2 .5) NM - - 3 D olphin Digital Me dia, Inc. NA D P DM OT C B B US D U nited S ta tes 0 .59 2 8.7 NA NM NM 1.0 x - 6 E olith C o. L td. 1 2/31 /200 7 A0 410 60 K OS E KR W S outh K orea 515 1 7.4 18. 1 (0 .0) -0 .3% - - NA E xte ns ions , Inc. 9 /30 /200 8 E XT I OT C P K US D U nited S ta tes 0 .15 1 4.2 NM NM NM - - 2 F inancia l Media G roup, Inc. 1 1/30 /200 8 F NG P OT C B B US D U nited S ta tes 0 0 .5 6.8 1 .2 18 .3% 0.7 x - 22 F luid Mus ic Ca nada, Inc. 9 /30 /200 8 T S X:F MN TSX C AD U nited S ta tes 0 .40 1 6.7 4.2 (8 .6) NM 3.8 x - 29 F rogs te r Interactive P icture s AG 6 /30 /200 8 F RG XT R A E UR G ermany 7 2 0.4 5.3 (3 .2) -6 0.6% 1.1 x 6.5x NA G a ma nia D igital E ntertainment C o., L td. 9 /30 /200 8 61 80 GTSM TWD T aiwan 32 .60 14 5.5 109 .3 1 8.5 16 .9% 0.5 x 1.8x NA G a me On C o L td. 1 2/31 /200 8 38 12 TSE J PY J apan 93, 600 9 3.2 76. 8 1 9.9 25 .9% 3.6 x - NA G e oS e ntric O yj 9 /30 /200 8 G E O1 V H LS E E UR F inland 0 .03 2 4.6 5.4 (1 2.4) NM - - 92 G iant Intera ctive G roup, Inc. 1 2/31 /200 8 GA NYS E US D C hina 7 1,5 43.6 233 .2 14 4.4 61 .9% 1.3 x 5.3x NA G iga Media Ltd. 9 /30 /200 8 G IG M N as da qG S US D T aiwan 5 .91 31 9.3 200 .5 4 8.0 23 .9% - - 975 G ravity C o., L td 9 /30 /200 8 GR VY N as da qG M US D S outh K orea 1 1 9.2 35. 4 6 .8 19 .2% 40.4 x - 636 G ree, Inc. 6 /30 /200 8 T S E : 363 2 TSE J PY J apan 5 ,600 .00 1,2 86.4 30. 3 1 0.9 36 .0% 1.2 x 6.7x NA G ungH o O nline E ntertainment, Inc. 1 2/31 /200 8 37 65 OS E J PY J apan 1 35, 300 15 9.6 115 .8 2 0.7 17 .8% 0.7 x - NA H anbitS of t, Inc. 1 2/31 /200 8 A0 470 80 K OS E KR W S outh K orea 3 ,210 .00 5 0.9 50. 3 (1 4.2) -2 8.2% 0.3 x 6.1x NA IAC /InterActiveC orp. 1 2/31 /200 8 IAC I N as da qG S US D U nited S ta tes 15 2,1 48.0 1 ,44 5.1 6 4.6 4 .5% - - 3 ,20 0 IAS E nergy, Inc. 1 /31 /200 9 IAS C.A OT C B B US D C ana da 0 .05 3 .2 0.0 (0 .8) NM - - NA IdeaE dge, Inc. 1 2/31 /200 8 OT C B B :IDAE OT C B B US D U nited S ta tes 0 1 4.8 0.0 (4 .6) NM 1.8 x - NA is ee media Inc. 1 2/31 /200 8 IE E T S XV C AD C ana da 0 .09 3 .7 1.2 (4 .7) NM 1.0 x 2.8x NA J umbuck E ntertainment P ty Ltd. 1 2/31 /200 8 AS X:J MB AS X AU D Aus tra lia 1 1 6.9 12. 2 4 .5 37 .2% 5.3 x - 72 J umpT V Inc. 6 /30 /200 8 T S X:J T V TSX C AD C ana da 0 .54 4 8.9 11. 5 (1 .8) -1 5.3% 0.9 x 1 1.5 x NA K a boos e Inc. 9 /30 /200 8 T S X:K AB TSX C AD C ana da 0 4 4.6 59. 1 4 .5 7 .6% 3.5 x 1 0.3 x NA K ings oft Co. Ltd. 9 /30 /200 8 38 88 S E HK HKD C hina 3 .25 45 0.3 106 .8 3 6.1 33 .8% 2.4 x - 1 ,66 0 Lingo Media Corporation 9 /30 /200 8 T S XV : LM T S XV C AD C ana da 1 7 .2 3.2 (1 .4) -4 2.5% 0.3 x - NA Live World Inc. 9 /30 /200 8 LV WD OT C P K US D U nited S ta tes 0 .13 4 .0 11. 7 (1 .2) -1 0.1% - - 73 LookS mart, Ltd. 1 2/31 /200 8 LOOK N as da qG M US D U nited S ta tes 1 1 7.2 65. 0 (2 .0) -3 .1% - - NA Magnitude Information S ys tems Inc. 9 /30 /200 8 MA G Y OT C B B US D U nited S ta tes 0 .02 8 .3 0.1 (3 .2) NM 4.1 x 1 0.7 x 13 Mixi, Inc. 1 2/31 /200 8 21 21 TSE J PY J apan 3 78, 000 59 7.5 120 .8 4 5.9 38 .0% 1.0 x 6.2x NA Mode rn Times G roup Mtg AB 1 2/31 /200 8 MT G B OM S EK S weden 135 .25 1,0 68.9 1 ,57 9.2 25 2.5 16 .0% - - NA Moggle , Inc 1 2/31 /200 8 MMOG OT C B B US D U nited S ta tes 2 8 3.5 NM (1 .1) NM 4.5 x - 3 MOK O.mobi L imited 1 2/31 /200 8 MK B AS X AU D Aus tra lia 0 .09 5 .4 1.0 (2 .0) NM 2.4 x 8.8x NA N E OW IZ G ames C orpora tion 1 2/31 /200 7 A0 956 60 K OS E KR W S outh K orea 45, 400 31 5.9 130 .4 3 5.1 26 .9% 1.5 x 3.3x NA N etD ragon W ebS oft, Inc. 1 2/31 /200 8 77 7 S E HK HKD C hina 4 .09 27 8.9 87. 2 3 9.9 45 .7% - - NA N ete as e.com I nc. 1 2/31 /200 8 NT ES N as da qG S US D C hina 25 3,1 12.0 451 .1 29 3.3 65 .0% - - NA N eXplore Corpora tion 9 /30 /200 7 N XP C OT C P K US D U nited S ta tes 0 .60 3 3.5 NM (4 .9) NM - - 19 N gi G roup Inc. 1 2/31 /200 8 24 97 TSE J PY J apan 24, 300 3 0.9 101 .3 3 1.2 30 .8% 0.2 x 0.9x NA N orthgate Te chnologies L imited 1 2/31 /200 8 59 005 7 BS E INR India 31 .30 2 1.3 131 .8 2 3.2 17 .6% 2.5 x 9.8x 286 Open T e xt Corp. 1 2/31 /200 8 OT E X N as da qG S US D C ana da 34 1,7 71.3 769 .3 19 5.0 25 .3% - - 3 ,40 0 Openwave S ys tems Inc. 1 2/31 /200 8 OP W V N as da qG S US D U nited S ta tes 0 .90 7 5.0 199 .6 (1 0.2) -5 .1% - - 627 P e rf ect W orld C o., Ltd. 1 2/31 /200 8 PW R D N as da qG S US D C hina 14 71 6.4 210 .2 11 3.7 54 .1% 2.6 x - NA P hotoChannel N etwork s Inc. 1 2/31 /200 8 T S XV : P N T S XV C AD C ana da 1 .60 4 2.7 15. 9 (0 .8) -4 .9% - - NA Quepa s a C orp. 9 /30 /200 8 QP S A N as da qC M US D U nited S ta tes 1 1 2.2 0.1 (1 1.8) NM 0.0 x 0.1x 63 OA O R B C Information S ys tems 1 2/31 /200 7 R BC I R TS US D R us s ia 0 .38 5 2.7 139 .3 1 8.2 13 .1% - - NA S handa Interactive E ntertainme nt L td. 1 2/31 /200 8 S N DA N as da qG S US D C hina 37 2,5 54.0 522 .0 23 9.9 46 .0% 0.7 x 5.2x NA S hutte rf ly, Inc. 1 2/31 /200 8 S F LY N as da qG S US D U nited S ta tes 9 .34 23 4.9 213 .5 2 8.4 13 .3% 1.4 x 1 5.4 x 514 S K C ommunications Co., Ltd. 1 2/31 /200 7 A0 662 70 K OS E KR W S outh K orea 7, 300 21 7.2 150 .0 1 4.1 9 .4% 3.3 x 3 2.5 x NA S N AP Inte ra ctive , Inc. 9 /30 /200 8 S T VI OT C B B US D U nited S ta tes 0 .80 8 .6 2.3 0 .2 10 .1% 1.1 x - 5 S N M G lobal H oldings 9 /30 /200 8 S N MN OT C P K US D U nited S ta tes 0 0 .0 2.0 (0 .7) -3 4.8% 0.1 x - 33 S ocia l Media V e nures , Inc. 1 2/31 /200 8 S MV I OT C P K US D U nited S ta tes 1 .20 0 .0 0.1 (0 .1) -6 0.5% 2.8 x 6.8x NA S ohu. com Inc. 1 2/31 /200 8 S OH U N as da qG S US D C hina 40 1,5 28.4 429 .1 18 0.5 42 .1% - - 3 ,19 7 S ite s earch C orporation 1 /31 /200 9 S T PC OT C B B US D U nited S ta tes 3 .50 2 8.2 NM (1 .1) NM 0.8 x 3.9x 15 S park N etworks , Inc. 1 2/31 /200 8 LOV AME X US D U nited S ta tes 2 4 7.3 57. 3 1 2.3 21 .5% - - NA S pectrumDN A, Inc. 9 /30 /200 8 S P XA OT C B B US D U nited S ta tes 0 .19 9 .2 0.1 (2 .7) NM 13.7 x 2 7.8 x 7 T encent Holdings L td. 1 2/31 /200 8 70 0 S E HK HKD C hina 58 13,3 41. 9 1 ,04 6.4 51 7.5 49 .5% 0.2 x - 6 ,19 4 T he P arent C ompany 8/2/2008 K ID S .Q OT C P K US D U nited S ta tes 0 .05 1 .3 112 .0 (1 3.5) -1 2.0% - - 347 T he 9 L imited 1 2/31 /200 8 N CT Y N as da qG S US D C hina 12 33 1.7 249 .8 8 4.1 33 .7% - - NA T he S treet.com, Inc. 1 2/31 /200 8 TSCM N as da qG M US D U nited S ta tes 1 .99 6 0.7 71. 9 7 .0 9 .7% 4.6 x - 310 T otal S port Online A S 3 /31 /200 6 T OS O OT C NO NOK N orwa y 0 0 .2 2.0 (1 .0) -5 0.6% 0.2 x - 16 T ree.C om, Inc. 1 2/31 /200 8 TR EE N as da qG M US D U nited S ta tes 4 .47 4 4.6 228 .6 (2 3.9) -1 0.4% 0.1 x 2 9.5 x 700 U nis erve C ommunications Corp. 1 1/30 /200 8 T S XV : US S T S XV C AD C ana da 0 0 .8 23. 8 0 .1 0 .4% 1.0 x 4.3x NA U nited Online Inc. 1 2/31 /200 8 U NT D N as da qG S US D U nited S ta tes 4 .35 35 7.3 669 .4 15 3.9 23 .0% 18.1 x - 1 ,46 9 U OMO Media , Inc 1 /31 /200 9 U OMO OT C B B US D C ana da 0 1 1.1 0.6 (0 .5) -7 8.2% 44.0 x - NA V O IS , Inc. 1 2/31 /200 8 V OIS OT C B B US D U nited S ta tes 0 .12 1 .0 0.0 (1 .3) NM - - 4 W ebze n Inc. 1 2/31 /200 8 W ZE N N as da qG M US D S outh K orea 2 2 0.7 20. 6 (2 .1) -1 0.1% 3.1 x - 330 W iz za rd S of twa re Corpora tion 9 /30 /200 8 W ZE AME X US D U nited S ta tes 0 .43 1 9.4 6.2 (6 .5) NM - - 110 W oozyF ly, Inc. 9 /30 /200 8 W ZY F OT C B B US D U nited S ta tes 0 2 .6 0.0 NM NM - - 14 W orlds .com Inc. 9 /30 /200 8 W DDD OT C B B US D U nited S ta tes 0 .18 9 .4 0.1 NM NM - - 1 W ynds torm C orporation NA W Y ND OT C B B US D U nited S ta tes 0 2 .2 NA NM NM 3.1 x 9.6x NA XIN G AG 1 2/31 /200 8 O1B C XT R A E UR G ermany 28 .80 19 7.1 45. 9 1 4.7 32 .0% 1.9 x 8.5x NA Y e dangOnline Corp. 1 2/31 /200 7 A0 527 70 K OS E KR W S outh K orea 8, 400 9 5.1 49. 6 1 1.1 22 .4% 0.5 x - NA Y nk K orea Inc. 1 2/31 /200 7 A0 237 70 K OS E KR W S outh K orea 3 ,780 .00 6 .7 14. 1 (1 .1) -7 .6% 0.8 x - NA ZipLocal Inc. 1 2/31 /200 8 T S XV : ZIP T S XV C AD C ana da 0 1 .0 2.6 (2 .8) NM - - NA H igh 13,3 41. 9 1 ,579 .2 51 7.5 65 .0% 44.0 x 3 2.5 x 6 ,194 Low 0 .0 0.0 -23.9 -9 8.9% - - 1 A vera ge 386.3 138.6 31.3 8.9% 4.7x 8.9x 603 Median 3 0.9 47. 8 0 .2 16 .4% 1.3 x 6.6x 83 Figure 1. Web 2.0 Universe Summary Source. Capital IQ C A P I T A L M A R K E T S A C T I V I T Y (M & A A N D F I N A N C I N G ) March activity slows below busy February: In the month of March there were 19 financings announced (total $118.7 million, average $6.1 million) compared to 25 financings announced in February, totalling $185.5 million, or $7.4 million on

- 3. Page 3 average (Figure 2). The average value for February was above the $6.8 million average for January, with four financings over $15 million in February (Twitter, Synthasite, Tremor Media, and Offerpal Media) vs. no deals over $15 million in January. There was only one $15 million deal in March – Vidyo. Financing Activity Last Three Months 250.0 25.0 200.0 20.0 150.0 15.0 (US$m) (US$m) 100.0 10.0 50.0 5.0 0.0 0.0 Jan-09 Feb-09 Mar-09 Total Average Figure 2. Financings, Last Three Months Source. Company reports Vidyo largest deal in March: The largest deal in March was the $15 million Series D round for Vidyo (Figure 3). For additional details, see Figures 30 and 31 (at end of note).

- 4. (US$m) 0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0 Twitter Synthasite Tremor Media Aster Data Systems Source. Company reports Vidyo Offerpal Media Imagini Yodle Buzznet Emergent Game AdMob LendingClub SendMe Inc. Outbrain Miva Figure 3. Capital Market Activity, Last Three Months VirtuOz Auditude Visible Measures companies raising $60.5 million. SuperSecret RatePoint Nurien DECA Go Internet Media IMVU NewsGator One True Media Tvtrip GoViral Play Hard Sports SundaySky JibJab Xobni InsideView Kewego Tongxue Motionbox SocialMedia Fliqz Oodle Greystripe Wamba OMGPOP Geni Gbox Sportsblogs AboutUs TextDigger OneSpot Apture FetchDog Simulmedia Virtual Fairground Mixpo Tynt E-Global Sports Network AnySource Media Pixazza Financing Summary - Last Three Months 7 Billion People FamilyLink.com Tripwolf mEgo WhistleBox Mendeley Sports Composite DE Outright Hunch Tvinci Filtrbox MMO Life AdultSpace Cake Financial Myngle Hubdub Snooth CoveritLive 33Across fav.or.it Three Melons TweetDeck BackType Identi.ca Meez Pulse Entertainment Jan-09 Mar-09 Feb-09 Page 4 16 companies raising over $120 million (Figure 4). Social networking companies have the next highest totals, with 11 Video continues to be the most active sector: Activity over the last three months was busiest in the video sector, with

- 5. Page 5 Capital Market Activity by Sector - Last Three Months 140.0 120.0 100.0 80.0 (US$m) 121.1 60.0 40.0 60.5 42.9 42.3 20.0 35.8 26.5 25.0 22.5 20.9 19.5 15.6 15.0 12.4 12.0 12.0 11.5 11.4 10.0 6.2 5.5 4.3 4.1 3.2 3.1 2.0 1.3 0.0 Comment/Reputation Gaming Micromedia Visual Commerce Wiki Travel RSS Microblog Media Mobile Publishing Online Learning Financial Services Infrastructure Lending Blog Mobile Ad Search Social Networks Virtual Goods Video Virtual World Aggregation Crowdsourced Ad Network Analytics Content # companies 16 11 8 5 3 4 2 4 2 3 2 1 3 1 1 2 1 1 3 1 1 1 2 1 1 1 Figure 4. Capital Market Activity, by Sector, Last Three Months Source. Company reports Average round size decreases: On a trailing 12-month basis, total financing dollars fell as of March 2009, with average round sizes decreasing slightly. (Figure 5). LTM Financing 4,000.0 18.0 16.0 3,500.0 14.0 3,000.0 12.0 2,500.0 10.0 (US$m) (US$m) 2,000.0 8.0 1,500.0 6.0 1,000.0 4.0 500.0 2.0 0.0 0.0 May-06 May-07 May-08 Nov-05 Mar-06 Nov-06 Mar-07 Nov-07 Mar-08 Nov-08 Mar-09 Jul-05 Sep-05 Jan-06 Jul-06 Sep-06 Jan-07 Jul-07 Sep-07 Jan-08 Jul-08 Sep-08 Jan-09 Total Average Figure 5. Financings, Last 12 Months Source. Company reports

- 6. Page 6 Cumulative total nears $5.8 billion: Overall, on a cumulative basis, W eb 2.0 financings have totalled nearly $5.8 billion, with the majority of the financing coming in late 2007 and the first three quarters of 2008 (Figure 6).Financing for the first quarter of 2009 passed that raised in the fourth quarter of 2008 – reversing the downtrend since the second quarter last year. However, for the period ended Q1-C2009, total capital raised was below Q1-C2008 level (at $748.2 million). Web 2.0 Financing (cumulative) 1,400.0 7,000.0 1,314.8 1,200.0 6,000.0 963.4 1,000.0 5,000.0 800.0 4,000.0 748.2 (US$m) (US$m) 600.0 3,000.0 528.9 521.0 400.0 2,000.0 338.5 330.1 151.7 159.3 200.0 1,000.0 126.4 135.6 129.5 87.2 84.0 37.5 33.5 18.2 41.9 57.8 38.8 20.1 0.0 0.0 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 2004 2005 2006 2007 2008 2009 Figure 6. Financing, Cumulative Source. Company reports U.S. remains dominant: U.S. companies continue to dominate capital market activity – with almost 67.5% of financings/M&A involving U.S. companies (based on dollars) (Figure 7). Based on number of transactions, the U.S. leads with 73.1% of deals, while Canada is third in number of financings at 4.7% (Figure 8). Financing/M&A by Country - LTM (#) Financing/M&A by Country - LTM ($) China Canada UK Israel 16.0% 4.7% 5.6% 3.4% Russia France 4.1% 2.6% UK Israel 2.4% 1.9% ROW France 10.7% 1.6% Denmark 1.6% ROW 5.0% USA 73.1% USA 67.5%

- 7. Page 7 Figures 7 & 8. Financing/M&A, by Country (LTM, $, #) Source. Company reports Larger volume of early-stage funding (by count): Almost half of financings in the last 12 months are for early-stage companies (Angel/Seed or Series A) (Figure 9). Series B rounds are 29.2% of the total, with later-stage (Series D, E and PIPE) deals accounting for just 9.2%. Financing by Type - LTM Series C 15.2% Series B 29.2% Series D 4.4% Angel/Seed 11.2% Debt financing Series A 2.8% 35.2% PIPE 2.0% Figure 9 Financing, by Type (LTM, #) Source. Company reports Equity financings smaller over last 12 months: In the last 12 months, the average size of Series A, B, C and D rounds have all been lower than the overall average (Figure 10).

- 8. Page 8 Average financing round size 40.0 36.1 35.0 33.5 31.6 30.0 27.4 25.0 22.7 (US$m) 20.0 17.5 15.0 11.4 11.7 11.3 11.3 10.0 7.9 7.3 6.3 5.4 5.0 3.3 2.4 0.0 Angel/Seed Debt financing PIPE Series A Series B Series C Series D Series E LTM Average Size Overall Average Figure 10. Average Size per Round Source. Company reports C A P I T A L M A R K E T S A C T I V I T Y (P R I C E P E R F O R M A N C E ) Price Performance: Our W eb 2.0 index (market-cap weighted) underperformed the NASDAQ composite index from mid 2008 until recently when it has moved sharply higher than the NASDAQ index (Figure 11).