Empfohlen

Weitere ähnliche Inhalte

Andere mochten auch

Andere mochten auch (13)

Ähnlich wie Standard Activism Materials Update

Ähnlich wie Standard Activism Materials Update (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Standard Activism Materials Update

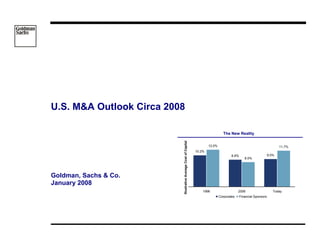

- 1. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 1/17 U.S. M&A Outlook Circa 2008 The New Reality Illustrative Average Cost of Capital 12.0% 11.7% 10.2% 8.8% 9.0% 8.0% Goldman, Sachs & Co. January 2008 1996 2006 Today Corporates Financial Sponsors

- 2. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 1/17 M&A Outlook Circa 2008 Agenda Likely U.S. Deal Activity – Trends among Key Players Changes to Transaction Structures and Terms Evolution of Board, Management and Shareholder Dynamics — Impact on Activism and Hostile Activity What’s Next? This material is intended only to facilitate your discussions with Goldman Sachs as to the opportunities available to our private clients and is provided solely in our capacity as a broker-dealer. This material does not constitute an offer or solicitation with respect to the purchase or sale of any security in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation. This material is based upon information which we consider reliable, but we do not represent that such information is accurate or complete, and it should not be relied upon as such. Any historical price(s) or value(s) is as of the date indicated. Information and opinions are as of the date of this material only and are subject to change without notice. Services offered through Goldman, Sachs & Co. Member FINRA. © Copyright 2008, The Goldman Sachs Group, Inc. All rights reserved 1

- 3. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 2/17 Deal Activity The Bottom Line: Likely Net Reduction; Change in Nature of Acquirors Key Takeaways Financial buyers — Increased cost of capital — Financing backlog from pending deals creating overhang / doability issues − Smaller transactions and joint bids with corporates — But, $300 billion of capital to invest and new “class” of financial buyer − Change in the nature of deals Strategic buyers ? — Sellers: − − Volatility / uncertainty = Fewer companies for sale More spinoff transactions (Cadbury Schweppes, Bristol-Myers) — Buyers: − Decrease in CEO / Board confidence and increase in risk-averse behavior − Higher M&A “hurdle” − But, strategic buyers will have reduced competition from financial players − Weakness of dollar will catalyze cross-border M&A − Reduced stock prices = more potential acquisition opportunities What are the likely overall results? — Strategic activity is not likely to offset decrease in sponsor activity — Handful of large deals could be big drivers of activity (and the big question mark) 2

- 4. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 3/17 Private Equity / Financial Investors The Bottom Line: Current Conditions in the Financing Markets Likely to Meaningfully Reduce LBO Activity Cost of Capital Has Swung Back in Favor of Strategic Buyers Credit Spreads Are Considerably Higher Illustrative Average Cost of Capital 550 12.0% 11.7% 500 10.2% 450 8.8% 9.0% 8.0% 400 350 300 250 200 150 1996 2006 Today 100 1/1/06 4/1/06 7/1/06 10/1/06 1/1/07 4/1/07 7/1/07 10/1/07 Corporates Financial Sponsors CDX BB Index CDX B Index Illustrative Financing Terms Mean More Leveraged Finance Backlog Continues to Be Considerable Operating / Financing Risk (Issuance vs. Backlog) Pre-Correction Post-Correction HY Issuance Loan Issuance HY Backlog Loan Backlog $352 Typical EBITDA Leverage: 7.0 – 8.0x 5.0 – 6.5x Equity %: 20-35% 35-45% Flex: L + 300 L + 500 $226 Caps: 11% 15% Covenant: No Yes $86 $91 $86 $79 $94 $78 $101 $66 $69 MAC Clause: No Yes (generally) $56 $54 $39 $33 $11 $9 May-07 Nov-06 Mar-07 Nov-07 (7/07) Oct-06 Dec-06 Jan-07 Feb-07 Apr-07 Jun-07 Jul-07 Aug-07 Sep-07 Oct-07 Dec-07 Projected Peak (YE 07) 3

- 5. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 4/17 Private Equity / Financial Investors Likely Themes for 2008 Increase in PIPEs / Hybrids / Convertibles — Examples: E*Trade, Countrywide Financial, Freddie Mac Portfolio company acquisitions with greater equity component Partnering with strategic buyers Smaller deals (generally, deals will be less than $5 billion in the near term) New players, such as sovereign wealth funds Financial and distressed assets are key focus areas Strong receptivity to monetization / sale of portfolio companies 4

- 6. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 5/17 Strategic Buyers – “Traditional Corporates” Equity Markets, Volatility and Strategic Imperatives Will Drive Appetite for Acquisitions M&A Volume is Positively Correlated with Equity Markets Corporates Continue to Have Balance Sheet Cash $300 1,600 12 Current $250 10 8.5% M&A Volume ($bn) $200 1,300 S&P 500 Cash/Assets (%) 8 $150 6 $100 1,000 30-yr average 5.9% 4 $50 $0 700 2 1999 2000 2001 2002 2003 2004 2005 2006 2007 Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- 0 Dec-73 Dec-75 Dec-77 Dec-79 Dec-81 Dec-83 Dec-85 Dec-87 Dec-89 Dec-91 Dec-93 Dec-95 Dec-97 Dec-99 Dec-01 Dec-03 Dec-05 Dec-07 All Other Deals greater than $10B S&P 500 But M&A Volume Inversely Related to Volatility Increasing Cost to Move Down Credit Curve US M&A Volume 350 296 VIX Differential (bps) 300 Indexed M&A/VIX 250 169 200 149 150 91 74 100 37 33 6 50 0 Average Maximum Minimum Today Jan-98 Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 1992 - 2007 A to BBB BBB to BB Source: Thomson Financial Securities Data, FactSet 5

- 7. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 6/17 Strategic M&A – Trends and Developments Strategic Buyer Activity is Now Driving M&A Strategic Deals are Still Happening (US Deals Since July 2007) Amt US Strategic M&A Volume $180 100% Acquiror Target ($bn) Strategic M&A as % of Total Announced Volume ($bn) Strategic M&A as % of Total $160 90% Basell Lyondell Chemical $18.8 $140 $120 80% Transocean GlobalSantaFe 17.4 $100 70% Ingersoll-Rand Trane 11.5 $80 $60 60% Vivendi Universal Games Activision 10.5 $40 50% Hexion Special Chemicals Huntsman 10.1 $20 $0 40% Petrochemical Industries Co Dow Chemicals 9.5 May-06 May-07 Mar-06 Nov-06 Mar-07 Nov-07 Jan-06 Feb-06 Apr-06 Jun-06 Jul-06 Aug-06 Sep-06 Oct-06 Dec-06 Jan-07 Feb-07 Apr-07 Jun-07 Jul-07 Aug-07 Sep-07 Oct-07 Dec-07 KSC (Petrochemicals) Toronto-Dominion Bank Commerce Bancorp 8.6 Siemens Medical Solutions Dade Behring Holdings 7.7 “Mergers of Equals” Have Received Positive Market Reactions Nokia NAVTEQ 7.6 27% National Oilwell Varco Grant PrideCo 7.5 24% % Change in Price (Day Announced) SAP Business Objects 5.7 18% 16% 12% Henkel National Starch & Chemical 5.5 10% (Adhesives business) 7% 6% 5% 5% Plains Exploration & Pogo Producing 5.4 Production Bank of New Bowater Compression Compressor Financial XM Satellite Transocean GlobalSantaFe Abitibi Sirius Satellite Mellon Philips Electronic Respironics 5.1 Hanover Universal York Radio SK Telecom Sprint Nextel 5.0 Source: Thomson Financial Securities Data, Capital IQ 6

- 8. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 7/17 Strategic Buyers – Observations From the Last Downturn M&A Will Continue, But Overall Volume Likely to Decline The First Half of 2007 Looked A Lot Like 2000’s Peak, So if LBOs are the New “Tech Bubble”… Opportunistic Hostile Activity Will Spike Post-“Crises” 1999-2000 1H2007 Hostile as a % of Total M&A 31% 6 Months Prior 6 Months After Non-Tech 24% LBOs 19% 50.9% 18% 17% 18% 31.0% 15% 10% 8% 7% 5% 4% 5% 5% Stock Gulf War Russia- Russian- Tech Bubble 9/11 & Hurricane Market Conflict Mexico- LTCM Crisis Burst (9/00- Invasion of Katrina Crash (12/14/90- Orange (8/18/98- 3/01) Afghanistan (8/26/05- Tech-Related Strategic M&A (10/14/87- 1/16/91) County 10/8/98) (9/11/01- 8/30/05) 49.1% 69.0% 10/19/87) (10/11/94- 12/7/01) 12/20/94) Traditional M&A Will Be Impacted (But Not As Much) P/E Multiples Will Likely Diverge Based on Credit Rating A- Or Higher Between BBB- & BBB+ Below BBB- 22.6x % Decline y-o-y 19.9x 18.4x 17.3x 18.1x 17.4x 17.4x 17.0x 17.5x 17.8x 17.0x Median P/E Multiple 17.8x 17.1x 17.3x 15.3x 15.5x 16.5x 16.2x 16.4x -33% 13.1x -38% 11.7x -64% -73% 2001 vs. 2000 2002 vs. 2001 Non-Tech Tech-Related 2001 2002 2003 2004 2005 2006 Current Source: Thomson Financial Securities Data 7

- 9. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 8/17 Cross-Border M&A Is Accelerating Cross-Border M&A is Nearly Half of Overall Activity Sovereign Wealth Funds – Key Investments Abu Dhabi Inv Authority Citigroup (4.9%), Advanced Micro Devices $2,200 Cross-Border Volume $2,053 50% (“ADIA”) (8.1%), Arab Banking Corporation (26.6%), Arab 2,000 % of Total M&A ($650-1,000 billion) International Bank (25%) Banque de Tunisie et 48% 1,800 des Emirats (38.9%), Union Cement (20.4%) Cross-Border Volume ($bn) 45% Percent of Total M&A 1,600 Barneys New York (100%), Standard 1,400 Chartered (2.7%), GLG Partners (3%), Time 40% Warner (2.4%), SpiceJet (3.34%), One 1,200 Istithmar $1,048 Trafalgar Square (100%) 1,000 ($8 billion) $920 35% 800 Och-Ziff (9.9%), Doncaster’s Group (100%), $589 35% 600 EADS (3%), HSBC (Undisclosed), Mauser $348 32% 30% (100%), Merlin Entertainment Group (20%), 400 $361 30% Dubai International Capital Travelodge (100%), Sony (Undiscl.) 200 29% 27% ($12 billion) 0 25% 2002 2003 2004 2005 2006 2007 Carlyle (7.5%), Ferrari (5%), Spyker Cars (17%) Mubadala Development, Developing World Acquiring Developed World Assets Abu Dhabi British Petroleum (Undisclosed), Daimler $166 Chrysler (7%) Kuwait Investment Authority ($213 billion) Volume ($bn) Barclays (2.1%), Standard Chartered (14%), Merrill Lynch (Undiscl.) $73 $48 Temasek, Singapore $25 ($108 billion) $22 $17 $22 $10 $12 $10 $7 China State Investment Morgan Stanley (9.9%), Blackstone (9.9%) Company ($200-400 billion) 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 Qatar Investment Authority Sainsbury (25%), London Stock Exchange ($50-70 billion) (20%), OMX (10%), Lagardere, (5.1%) Source: Thomson Financial Securities Data, FactSet, other public sources 8

- 10. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 9/17 Is the U.S. “For Sale”? Foreign acquisitions of U.S. companies has outpaced Illustrative Cost of US$1 Billion Cross-Border U.S. acquisitions of non-U.S. companies for the first time Acquisition Non-U.S. companies can now acquire U.S. assets (and Jan-06 Nov-2007 % Change Market P/E companies with substantial U.S. exposure) at significant 12.55x discounts to historical exchange rates € 0.84 bn € 0.69 bn (18.8)% (DJ Euro Stoxx 50) However, with exchange rates at a significant discount, 12.42x the value of earnings purchased is also less than it was ₤ 0.58 bn ₤ 0.50 bn (13.5)% (FTSE 100) previously 19.08x — Exchange rate dislocations historically have not been C$ 1.17 bn C$ 0.99 bn (15.3)% (S&P/TSX Composite) a principal driver of M&A 18.22x ¥ 118 bn ¥ 112 bn (5.0)% (Nikkei 225) BRIC Countries: For the First Time, Foreign Buying of US Companies 15.10x R$ 2.35 bn R$ 1.78 bn (24.3)% Represents Majority of US Cross-Border Flows (Bovespa) 13.46x US Acquisitions of Non-US Companies RUR 28.7 bn RUR 24.5 bn (14.8)% (Russian RTS $404 Non-US Acquisitions of US Companies Index) 27.88x $301 IDR 45.0 bn IDR 39.3 bn (12.5)% Volume ($bn) (BSE Sensex) $234 $217 $183 44.37x $163 CNY 8.1 bn CNY 7.3 bn (9.5)% (Shanghai SE $123 $135 Composite) $100 $82 18.64x $1 bn $1 bn N/A 2003 2004 2005 2006 2007 (S&P 500) Source: CapitalIQ; Thomson Financial Securities Data; Bloomberg 9

- 11. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 10/17 What Will Be The Deal Dynamics? Increased Tensions Regarding “Deal Certainty” Boards Will Assert More Control in M&A Processes in Negotiating LBOs Public scrutiny / risk of embarrassment Buyer Perspectives Seller Perspectives Acquirors and activist shareholders approaching board Reduced competition may lead Boards likely to demand more members directly with deal ideas to demands for less “seller- certainty in M&A contracts friendly” M&A terms More granularity /focus on Board involvement in discussing deals with shareholders Fewer carveouts to Material agreements with financing and ISS Adverse Effect clauses sources Potential “O’Neal effect” – Will CEOs be less likely to act Less willing to accept go-shop Increased reverse breakup fees without board authorization? clauses and reverse breakup fees Bottom Line: More focus on issues relating to deal completion More deals will fall apart Focus on Shareholder Support of M&A Deals Other Key Issues Attempts to bring large shareholders “under the tent” Emergence of new players prior to announcement, similar to U.K. transactions — SPACs (Special Purpose Acquisition Companies) – ISS’s Contentious List over $10 billion raised to date — List of deals which ISS is focused on that require a — Sovereign Wealth Funds shareholder vote — Funds paired with or formed by former executives — ISS recommends against a significant percentage of Shareholder vote dynamics transactions on this list — Stock lending and derivatives — Setting the record date — Getting out the vote Cross-border transactions — Flowback (stock deals) — CFIUS 10

- 12. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 11/17 Rule Changes Have Re-Opened Tenders as the Preferred Deal Structure Number of U.S. Tender Offers Emerging Themes Tender offers have become more common since the implementation of SEC guidance relating to the “Best 70 Price Rule” Tender offer provides tactical advantage for both sides — Smaller window for deal jump — Smaller window for opportunity to argue that a # of Tender Offers MAE has occurred More likely to get 50% approval — Shareholders are more likely to tender than vote 30 — Mitigates “dead shares” problem 27 — No ISS involvement (at this point) 21 Merger should be used if — Regulatory delay — Buyer shareholder vote is required (if more than 3 20% of shares issued) Can be used in LBOs, but not the preferred structure 2003 2004 2005 2006 2007 — Financing risk Source: FactSet MergerMetrics 11

- 13. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 12/17 Shareholder / Management / Board Dynamics Shareholder Activism Shareholder activism will continue — Perception of “alpha” returns has resulted in increased fundraising by activists — More direct engagement of boards, other shareholders and potential buyers — Focus likely to shift given market conditions divestiture of noncore assets or sale of company to strategic buyers vs. LBO or additional leverage — New Internet proxy rules, other regulatory proposals and the removal of takeover defenses will make it easier to pursue proxy fights Deals have become more difficult to get done — Rapidity of trading and stock lending impacting voting trends — Activism against transactions by hedge funds and traditional investors — ISS influence on M&A transactions — More topping bids / go-shops — Process litigation is the norm — Cross-border issues Corporate governance used as a “wedge” to achieve other ends — Pressure to remove takeover defenses — Attack compensation and related disclosures to undercut CEO — Threat of withhold votes – particularly at companies with “majority vote” requirements for director elections – to effect other changes or actions 12

- 14. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 13/17 Institutionalization of Activism How Have the Goals of Activism Evolved? Yesterday (Pre-Crunch) Today Sale of Company (sales to strategic buyers) LBO Leveraged Recapitalizations Change Management / Board Portfolio Changes (divestitures to strategic buyers) Monetization of Balance Sheet Change Governance 13

- 15. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 14/17 Post-Bubble, Post-Proxy Season Activism Current Drivers of Activism Post-Bubble Activism Situations CalPERS increasing investments in “activist” funds from $5 billion to $12 billion (Ramius) (Icahn) (Icahn) Success of targeted activism vehicles — Pershing Square raised $2 billion in two weeks to pursue activism at an unnamed (Chapman Capital) (Ramius) (Barington) $40 billion “U.S. icon” (later disclosed to be Target Corporation) Trian recently filed to raise $750 million for a SPAC (Breeden) (Knight Vinke) (S.A.C. Capital) Perception that activists have achieved “alpha” returns (Barington) (Red Mountain) (Steel Partners) ISS support of many dissident proxy fights leading to greater success More funds pursuing activism (Relational) (K Capital) (Sandell) Shifts in sector focus by activists — In: Sector consolidation — Out: Leveragability (Pershing Square) (Tracinda) (HealthCor) 14

- 16. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 15/17 Hostile Activity Has Increased and Fewer Companies Remain Independent, Driven by Buyer Opportunism and Fewer Defenses Hostile M&A Activity Continues to be High1 Outcome of Hostile Bids > $250mm $725 $620 Global Hostile/Unsolicited Volume ($bn) 30% 28% 29% 41% $264 $269 41% 30% $119 1997-2004 2005-2007 Remained Independent Sold to Third Party 2003 2004 2005 2006 2007 Sold to Unsolicited Bidder Source: Thomson Financial Securities Data 1 Hostile / unsolicited activity includes transactions that began as unsolicited. 15

- 17. ACTIVISMActivism and Anti-RaidStandard Activism MaterialsStandard Activism BookFall 2007 UpdateUpdate Materials v13.doc lawrdu 15 Jan 2008 11:04 16/17 What’s Next? Final Observations Strategic Buyers: Proactive, well-capitalized industry leaders can press their advantage(s) — Cash / certainty will be king Inbound activity into the U.S. Certain buyers will be aggressively opportunistic Financial Buyers: Sponsors will be more creative (PIPEs, divestitures, debt, LPDs) Financing terms will revert to prior periods with attendant impact on valuation (lower multiples, less exotics, market outs) Process: Tougher for sellers to generate broad auctions and competition Wider bid / asks and longer negotiations Low tolerance for risk Activism: Activism, driven by poor performance or industry dynamics — Continued deal scrutiny by investors Gap between boards and shareholders will continue to narrow 16