Q1 2014 Retail Market Research Report

•Als PPTX, PDF herunterladen•

1 gefällt mir•207 views

Q1 2014 Retail Market Research Report

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Andere mochten auch

Andere mochten auch (20)

Ähnlich wie Q1 2014 Retail Market Research Report

Ähnlich wie Q1 2014 Retail Market Research Report (20)

Mehr von Colliers International | Houston

Mehr von Colliers International | Houston (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Q1 2014 Retail Market Research Report

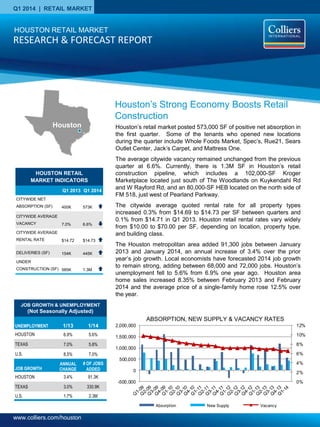

- 1. www.colliers.com/houston Q1 2014 | RETAIL MARKET HOUSTON RETAIL MARKET INDICATORS Q1 2013 Q1 2014 CITYWIDE NET ABSORPTION (SF) 400K 573K CITYWIDE AVERAGE VACANCY 7.0% 6.6% CITYWIDE AVERAGE RENTAL RATE $14.72 $14.73 DELIVERIES (SF) 154K 445K UNDER CONSTRUCTION (SF) 585K 1.3M Houston’s retail market posted 573,000 SF of positive net absorption in the first quarter. Some of the tenants who opened new locations during the quarter include Whole Foods Market, Spec’s, Rue21, Sears Outlet Center, Jack’s Carpet, and Mattress One. The average citywide vacancy remained unchanged from the previous quarter at 6.6%. Currently, there is 1.3M SF in Houston’s retail construction pipeline, which includes a 102,000-SF Kroger Marketplace located just south of The Woodlands on Kuykendahl Rd and W Rayford Rd, and an 80,000-SF HEB located on the north side of FM 518, just west of Pearland Parkway. The citywide average quoted rental rate for all property types increased 0.3% from $14.69 to $14.73 per SF between quarters and 0.1% from $14.71 in Q1 2013. Houston retail rental rates vary widely from $10.00 to $70.00 per SF, depending on location, property type, and building class. The Houston metropolitan area added 91,300 jobs between January 2013 and January 2014, an annual increase of 3.4% over the prior year’s job growth. Local economists have forecasted 2014 job growth to remain strong, adding between 68,000 and 72,000 jobs. Houston’s unemployment fell to 5.6% from 6.9% one year ago. Houston area home sales increased 8.35% between February 2013 and February 2014 and the average price of a single-family home rose 12.5% over the year. ABSORPTION, NEW SUPPLY & VACANCY RATES 0% 2% 4% 6% 8% 10% 12% -500,000 0 500,000 1,000,000 1,500,000 2,000,000 Absorption New Supply Vacancy Houston’s Strong Economy Boosts Retail Construction HOUSTON RETAIL MARKET RESEARCH & FORECAST REPORT Houston UNEMPLOYMENT 1/13 1/14 HOUSTON 6.9% 5.6% TEXAS 7.0% 5.8% U.S. 8.5% 7.0% JOB GROWTH ANNUAL CHANGE # OF JOBS ADDED HOUSTON 3.4% 91.3K TEXAS 3.0% 330.9K U.S. 1.7% 2.3M JOB GROWTH & UNEMPLOYMENT (Not Seasonally Adjusted)

- 2. RESEARCH & FORECAST REPORT | Q1 2014 | HOUSTON RETAIL MARKET SALES ACTIVITY Houston’s first quarter retail investment sales activity included 76 sales transactions. Total sales transaction volume totaled $52M and the average price per SF was $162. The average cap rate was 7.6%. Several of the more significant transactions that closed during the first quarter are highlighted on the left. LEASING ACTIVITY Houston retail leasing activity in the first quarter reached 1.2M SF. Overall, transactions under 10,000 SF comprised the largest group of retail leases, with the market recording eleven leases over 10,000 SF and only two over 20,000 SF in the first quarter. A partial list of the leases signed during the first quarter are listed in the table below. COLLIERS INTERNATIONAL | P. 2 Colony Plaza 4811 SH 6 S, Missouri City, TX Stafford Submarket RBA: 55,022 SF Built: 1996 Buyer: Texas Colony Plaza, LLC Seller: Everest Fund Ventures I, Ltd. Date: March 3, 2014 Price: $8.0M or $145/SF Cap: 9.5% Waterside Commons 9102-9825 S Mason Rd, Richmond, TX Far Southwest Submarket RBA: 39,779 SF Built: 2008 Buyer: Zenda Waterside Commons U.S. Seller: Mason Grand, Ltd. Date: March 18, 2014 Price: $8.85M or $222/SF Cap: N/A Windrose Plaza 20423 Kuykendahl Rd, Spring, TX Far North Submarket RBA: 28,715 SF Built: 2005 Buyer: Summit Dental Seller: American Spectrum Realty, Inc. Date: January 6, 2014 Price: $5.75M or $200/SF Cap: 8.15% RETAIL SALE TRANSACTIONS Tuscan Village Plaza 7214 FM 1488, Magnolia, TX Montgomery County Submarket RBA: 15,318 SF Built: 2007 Buyer: Private Investor Seller: 1488 Del Sul Investments LP Date: March, 2014 Price: $3.4M or $222/SF Cap: N/A Building Name/Address Submarket SF Tenant Lease Date Fairmont Junction Plaza Near Southeast 42,130 Bravo Ranch Supermarket Mar-14 Cypress Station Square Far North 31,622 Anthem College Jan-14 Portofino Center Montgomery County 22,500 Conn's Appliances Feb-14 Woodforest Shopping Center Pasadena/Galena Park 13,775 Chulas Jan-14 Quail Corner Stafford 12,779 King Dollar Feb-14 Pecan Park Plaza NASA/Clear Lake 12,500 Dollar Tree Feb-14 Uptown Park Uptown 11,384 Champps Americana1 Feb-14 Greenbriar Square Sugar Land 9,629 Pennywise Jan-14 E-1 - Sunrise Lake Village Far South 7,981 Title Boxing Club Feb-14 Tomball Marketplace Far Northwest 7,700 Five Below Jan-14 E-1 - Sunrise Lake Village Far South 6,736 Blue Lion Salon Studios Feb-14 Q1 2014 RETAIL LEASES 1 Renewal

- 3. RESEARCH & FORECAST REPORT | Q1 2014 | HOUSTON RETAIL MARKET RENTAL RATES The citywide average quoted rental rate for all property types increased 0.3% from $14.69 to $14.73 per SF between quarters and 0.1% from $14.71 in Q1 2013. Class A retail rental rates vary widely due to location and center type. Recent quoted rates for community centers and power centers range from $18.00 - $35.00 per SF while theme/ entertainment centers range from $25.00 - $35.00 per SF. Lifestyle centers in Class A locations such as High Street, Uptown Park and The Vintage range from $40.00 - $70.00 per SF. Strip centers range from $24.00 - $45.00 per SF and neighborhood centers range from $20.00 - $50.00 per SF. VACANCY & AVAILABILITY Houston’s retail vacancy remained at 6.6% over the quarter and fell 40 basis points from 7.0% in Q1 2013. By product type on a quarterly basis, theme/entertainment centers posted the largest decrease in vacancy, 540 basis points, followed by outlet centers decreasing 180 basis points and power centers decreasing 80 basis points. Strip center vacancy dropped 60 basis points and neighborhood center vacancy remained unchanged. Single-tenant, malls, community centers, and lifestyle center vacancy rose 10, 20, 70 and 170 basis points, respectively. Houston’s retail construction pipeline contains 1.3M SF and first quarter deliveries totaled 445,000 SF. ABSORPTION & DEMAND Houston’s retail market posted 573,000 SF of positive net absorption in the first quarter. Some of the tenants that moved into space during the first quarter are listed in the table at right. HOUSTON RETAIL MARKET STATISTICAL SUMMARY COLLIERS INTERNATIONAL | P. 3 Q1 2014 ABSORPTION Tenant/ Submarket SF Occupied Sears Outlet Center Southeast Outlier 33,494 Forgotten Angels Southeast Outlier 15,300 Spec’s Montgomery County 14,532 Rue21 Southeast Outlier 10,000 Pennywise Sugar Land 9,629 Bee Busy Wellness Center Southwest 8,640 Five Below Far Northwest 7,700 Adventure Kids Playcare Far New Territory 5,886 Urgent Care Southeast Outlier 4,800 Rentable Area Direct Vacant SF Direct Vacancy Rate Sublet Vacant SF Sublet Vacancy Rate Total Vacant SF Total Vacancy Rate Q1 2014 Net Absorption Q4 2013 Net Absorption Class A Rental Rates (in-line)* Strip Centers (unanchored) 32,506,790 3,104,212 9.5% 6,305 0.0% 3,110,517 9.6% 143,978 169,170 $25.00-$45.00 Neighborhood Centers (one anchor) 68,150,367 6,813,371 10.0% 98,296 0.1% 6,911,667 10.1% 92,464 525,305 $20.00-$50.00 Community Centers (two anchors) 43,531,464 2,864,950 6.6% 49,357 0.1% 2,914,307 6.7% (133,012) 144,775 $18.00-$35.00 Power Centers (3 or more anchors) 22,515,243 846,614 3.8% 23,483 0.1% 870,097 3.9% 40,847 99,229 $18.00-$35.00 Lifestyle Centers 3,692,644 180,013 4.9% 33,789 0.9% 213,802 5.8% 33,490 4,758 $40.00-$70.00 Outlet Centers 1,899,333 239,988 12.6% - 0.0% 239,988 12.6% 34,231 (8,728) $20.00-$40.00 Theme/Entertainment 752,640 229,731 30.5% - 0.0% 229,731 30.5% 40,200 (41,118) $25.00-$35.00 Single-Tenant 67,722,661 1,482,070 2.2% 64,554 0.1% 1,546,624 2.3% 283,192 174,343 N/A Malls 26,141,121 1,483,765 5.7% 54,750 0.2% 1,538,515 5.9% 37,219 54,882 N/A Greater Houston 266,912,263 17,244,714 6.5% 330,534 0.1% 17,575,248 6.6% 572,609 1,122,616

- 4. RESEARCH & FORECAST REPORT | Q1 2014 | HOUSTON RETAIL MARKET Accelerating success. COLLIERS INTERNATIONAL 1233 W. Loop South Suite 900 Houston, Texas 77027 Main +1 713 222 2111 LISA R. BRIDGES Director of Market Research | Houston Direct +1 713 830 2125 Fax +1 713 830 2118 lisa.bridges@colliers.com The Colliers Advantage Enterprising Culture Colliers International is a leader in global real estate services, defined by our spirit of enterprise. Through a culture of service excellence and a shared sense of initiative, we integrate the resources of real estate specialists worldwide to accelerate the success of our partners. When you choose to work with Colliers, you choose to work with the best. In addition to being highly skilled experts in their field, our people are passionate about what they do. And they know we are invested in their success just as much as we are in our clients’ success. This is evident throughout our platform—from Colliers University, our proprietary education and professional development platform, to our client engagement strategy that encourages cross-functional service integration, to our culture of caring. We connect through a shared set of values that shape a collaborative environment throughout our organization that is unsurpassed in the industry. That’s why we attract top recruits and have one of the highest retention rates in the industry. Colliers International has also been recognized as one of the “best places to work” by top business organizations in many of our markets across the globe. Colliers International offers a comprehensive portfolio of real estate services to occupiers, owners and investors on a local, regional, national and international basis. *Information herein has been obtained from sources deemed reliable, however its accuracy cannot be guaranteed. COLLIERS INTERNATIONAL | P. 4