Cbre office leasing market report 2014

•

2 likes•4,940 views

office space toronto, toronto office space, office search toronto, office space in toronto, office rentals toronto, commercial office space, commercial real estate toronto, office rent toronto, toronto offices for lease

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Cbre office leasing market report 2014

Similar to Cbre office leasing market report 2014 (20)

More from Chris Fyvie

More from Chris Fyvie (20)

Recently uploaded

Recently uploaded (20)

Cbre office leasing market report 2014

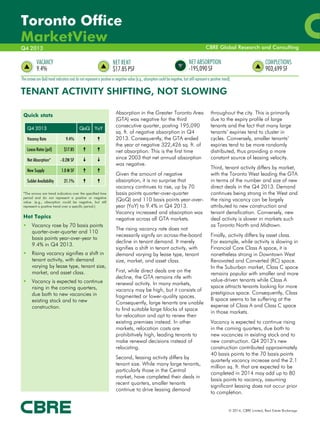

- 1. Toronto Office MarketView CBRE Global Research and Consulting Q4 2013 VACANCY 9.4% NET RENT $17.85 PSF NET ABSORPTION -195,090 SF COMPLETIONS 903,699 SF The arrows are QoQ trend indicators and do not represent a positive or negative value (e.g., absorption could be negative, but still represent a positive trend). TENANT ACTIVITY SHIFTING, NOT SLOWING Quick stats Q4 2013 QoQ YoY 9.4% Lease Rates (psf) $17.85 Net Absorption* - 0.2M SF New Supply 1.0 M SF 21.1% Vacancy Rate Sublet Availability *The arrows are trend indicators over the specified time period and do not represent a positive or negative value. (e.g., absorption could be negative, but still represent a positive trend over a specific period.) Hot Topics 1 Vacancy rose by 70 basis points quarter-over-quarter and 110 basis points year-over-year to 9.4% in Q4 2013. Rising vacancy signifies a shift in tenant activity, with demand varying by lease type, tenant size, market, and asset class. Vacancy is expected to continue rising in the coming quarters, due both to new vacancies in existing stock and to new construction. Absorption in the Greater Toronto Area (GTA) was negative for the third consecutive quarter, posting 195,090 sq. ft. of negative absorption in Q4 2013. Consequently, the GTA ended the year at negative 322,426 sq. ft. of net absorption. This is the first time since 2003 that net annual absorption was negative. Given the amount of negative absorption, it is no surprise that vacancy continues to rise, up by 70 basis points quarter-over-quarter (QoQ) and 110 basis points year-overyear (YoY) to 9.4% in Q4 2013. Vacancy increased and absorption was negative across all GTA markets. The rising vacancy rate does not necessarily signify an across-the-board decline in tenant demand. It merely signifies a shift in tenant activity, with demand varying by lease type, tenant size, market, and asset class. First, while direct deals are on the decline, the GTA remains rife with renewal activity. In many markets, vacancy may be high, but it consists of fragmented or lower-quality spaces. Consequently, large tenants are unable to find suitable large blocks of space for relocation and opt to renew their existing premises instead. In other markets, relocation costs are prohibitively high, leading tenants to make renewal decisions instead of relocating. Second, leasing activity differs by tenant size. While many large tenants, particularly those in the Central market, have completed their deals in recent quarters, smaller tenants continue to drive leasing demand throughout the city. This is primarily due to the expiry profile of large tenants and the fact that many large tenants’ expiries tend to cluster in cycles. Conversely, smaller tenants’ expiries tend to be more randomly distributed, thus providing a more constant source of leasing velocity. Third, tenant activity differs by market, with the Toronto West leading the GTA in terms of the number and size of new direct deals in the Q4 2013. Demand continues being strong in the West and the rising vacancy can be largely attributed to new construction and tenant densification. Conversely, new deal activity is slower in markets such as Toronto North and Midtown. Finally, activity differs by asset class. For example, while activity is slowing in Financial Core Class A space, it is nonetheless strong in Downtown West Renovated and Converted (RC) space. In the Suburban market, Class C space remains popular with smaller and more value-driven tenants while Class A space attracts tenants looking for more prestigious space. Consequently, Class B space seems to be suffering at the expense of Class A and Class C space in those markets. Vacancy is expected to continue rising in the coming quarters, due both to new vacancies in existing stock and to new construction. Q4 2013’s new construction contributed approximately 40 basis points to the 70 basis points quarterly vacancy increase and the 2.1 million sq. ft. that are expected to be completed in 2014 may add up to 80 basis points to vacancy, assuming significant leasing does not occur prior to completion. © 2014, CBRE Limited, Real Estate Brokerage

- 2. Submarket Inventory (SF) Vacancy Rate (%) Sublease as % of Vacant 4Q13 Net Absorption (SF) YTD Net Absorption (SF) 4Q13 New Supply (SF) 4Q13 Under Construction (SF) Net Rent ($ psf/yr) 81,438,380 6.1% 23.1% 21,316 -174,958 740,000 5,056,230 $23.77 Downtown 66,783,377 5.9% 23.8% 214,587 -185,119 740,000 5,056,230 $25.40 Financial Core 24,407,998 6.2% 27.7% -91,892 -419,816 0 1,923,546 $29.30 Greater Core 18,539,229 4.2% 22.0% 55,350 78,019 0 0 $21.63 Downtown South 4,096,442 5.0% 50.0% -22,114 -94,607 0 2,385,103 $23.34 Downtown North 7,693,967 8.5% 17.8% 335,084 331,113 740,000 0 $27.33 Downtown East 2,595,707 6.0% 16.8% -1,151 36,634 0 462,000 $19.03 Downtown West 9,450,034 6.5% 16.0% -60,690 -116,462 0 285,581 $18.90 14,655,003 7.4% 20.8% -193,271 10,161 0 0 $18.11 Bloor / Yonge 7,499,478 5.6% 16.6% -21,597 57,686 0 0 $20.92 St. Clair / Yonge 2,118,893 5.7% 24.6% -16,241 69,008 0 0 $18.28 Eglinton / Yonge 5,036,632 10.8% 23.2% -155,433 -116,533 0 0 $15.50 SUBURBAN 69,996,235 13.1% 20.1% -216,406 -147,468 163,699 1,645,839 $14.92 East 24,794,264 12.4% 13.7% -104,147 -22,792 0 0 $13.40 Scarborough 3,609,408 13.2% 4.5% 64,082 59,428 0 0 $12.19 Mark. N. / R. Hill 7,449,132 11.0% 23.2% -19,742 47,416 0 0 $15.97 Steeles / Woodbine 2,860,816 14.4% 4.4% -69,162 -98,316 0 0 $13.18 E. York / D. Mills S. 2,695,747 10.2% 32.0% -41,299 -43,116 0 0 $11.96 Don Mills North 2,707,278 8.0% 20.2% 7,115 23,350 0 0 $9.71 Consumers Road 3,862,867 15.8% 9.2% -67,886 -67,606 0 0 $12.67 G. Baker / Vic. Park 1,609,016 17.3% 2.0% 22,745 56,052 0 0 $14.34 11,947,937 7.3% 35.1% -79,097 -125,240 62,500 185,104 $17.49 North Yonge 7,707,955 7.5% 51.4% -132,486 -165,477 0 75,000 $18.08 North York West 2,170,968 5.2% 0.0% -8,816 2,484 0 0 $12.73 Vaughan 2,069,014 8.7% 4.5% 62,205 37,753 62,500 110,104 $17.29 33,254,034 15.7% 21.4% -33,162 564 101,199 1,460,735 $15.55 Bloor / Islington 1,497,663 10.7% 6.4% 64,414 90,360 0 0 $15.73 427 Corridor 2,208,002 8.7% 21.2% 24,716 26,734 0 0 $15.35 Airport Strip 3,209,910 22.8% 15.1% -24,158 -36,345 0 0 $13.62 Airport Corp. Centre 5,454,786 14.8% 44.4% -111,319 -136,440 0 382,708 $14.37 Mississauga South 1,893,118 13.8% 14.4% -43,004 -29,462 0 0 $16.15 City Centre 3,747,823 16.5% 16.2% -65,631 -84,193 0 56,324 $16.57 Hwy 10 / Hwy 401 3,849,275 11.9% 41.9% -29,613 11,905 36,199 689,594 $13.01 Meadowvale 4,041,272 15.0% 14.8% 164,415 79,861 0 159,761 $15.76 Brampton 1,277,281 27.7% 16.4% 15,733 137,171 0 75,000 $16.93 Oakville 2,832,177 16.5% 10.6% -969 126,988 65,000 64,000 $17.51 Burlington 3,242,727 17.6% 12.9% -27,746 -186,015 0 33,348 $16.05 151,434,615 9.4% 21.2% -195,090 -322,426 903,699 6,702,069 $17.85 Midtown North West 2 GTA Source: CBRE Limited Research, Q4 2013. © 2014, CBRE Limited, Real Estate Brokerage Toronto Office | MarketView CENTRAL Q4 2013 Table 1: Market Statistics 2

- 3. Submarket Project Developer Expected Completion Size (SF) % Pre-Leased Mississauga Gateway Centre Phase II HOOPP 146,863 Q1 2015 43% ACC Spectrum Square HOOPP 128,788 Q1 2015 0% Meadowvale 2455 Meadowpine Blvd Dorsay Development Corp. 114,761 Q3 2014 0% Vaughan 3100 Rutherford Rd Lorwood Homes Incorporated. 65,000 Q2 2014 25% Hwy 10/401 7020 Hurontario St Kallo Developments 60,000 Q1 2015 0% Hwy 10/401 Derrycrest Phase I Kenaidan 47,000 Q2 2014 100% Vaughan 9131 Keele Street Melrose Developments 45,104 Q2 2014 0% Hwy 10/401 Mississauga Gateway Centre Phase II HOOPP 44,751 Q3 2014 0% Burlington 1006 Skyview Dr United Lands 33,348 Q3 2014 50% Downtown East Globe and Mail Centre First Gulf Corporation 462,000 Q4 2016 39% Toronto Office | MarketView Hwy 10/401 Q4 2013 Table 2: Select Office Projects - Under Construction Source: CBRE Limited Research, Q4 2013. Chart 1: Market Outlook Absorption New Supply Vacancy 9% 2,000 6% 1,000 3% 0 0% -1,000 Vacancy 12% 3,000 SF (000s) 4,000 -3% Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014* Q2 2014* Q3 2014* Q4 2014* *FORECASTED Source: CBRE Econometric Advisors Chart 2: New Supply Central Suburban 1,200 SF (000s) 1,000 3 800 600 400 200 0 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Source: CBRE Limited Research, Q4 2013. © 2014, CBRE Limited, Real Estate Brokerage Downtown Toronto is currently in the midst of a construction cycle that will add 5.9 million sq. ft. of space through 2017. In Q4 2013 saw the commencement of this cycle with the completion of MaRS Phase 2, adding 740,000 sq. ft. of new supply to existing inventory and bringing current Downtown space under construction down to 5.1 million sq. ft. In addition to Downtown construction, three buildings totalling 163,699 sq. ft. were completed this quarter in the Suburban market, bringing total quarterly GTA new supply to 903,699 sq. ft. These completions significantly impacted both vacancy and absorption as they were delivered partiallyvacant, both increasing vacancy and contributing positively to absorption. The largest impact was felt in the Downtown North submarket, where the completion of MaRS Phase 2 contributed 5.2% to vacancy while also increasing absorption by 337,920 sq. ft. 3

- 4. Central Suburban Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Toronto Office | MarketView 14% 12% 10% 8% 6% 4% 2% 0% Vacancy in the GTA increased by 70 basis points, representing the highest single quarter vacancy increase in four years and the highest vacancy rate since 2010. Vacancy increased in both Central and Suburban markets, rising by 90 basis points and 40 basis points, respectively. The rise in vacancy is due to two major factors. First, the 903,699 sq. ft. of completions in Q4 2013 came online partially-vacant. The second contributor to rising vacancy is decreasing direct deal activity. In the Suburban market, tenant activity is strong for renewals with fewer direct lease deals done in Q4 2013. In the Central market, tenants have begun showing a slowdown in activity primarily due to their position within the expiry cycle. With many large tenants having already completed their deals in anticipation of the new builds, there is a shortage of large tenants on the market. Q4 2013 Chart 3: Vacancy Rates Source: CBRE Limited Research, Q4 2013. Chart 4: Rental Rates Central Suburban $25 $ psf $20 $15 $10 $5 $0 Average asking rental rates increased by $0.32 to $17.85 per sq. ft., rising most significantly in Class A space. The highest increase was felt in the Central market, where average asking rental rates increased by $0.52 to $23.77 per sq. ft. Rental rates in the Central market were most significantly affected by the completion of MaRS Phase 2, which pushed rental rates up by $8.65 to $27.33 per sq. ft. in the Downtown North submarket. Interestingly, even though vacancy is on the rise, landlords in the Central market have not yet softened on asking rates or concessions. Consequently, net effective rents have remained stable but are expected to soften in the coming quarters as landlords adjust their expectations. Conversely, in the Suburban market, average asking rental rates decreased by $0.20 to $14.92 per sq. ft. , driven by rate decreases in both the North and the West markets. Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Source: CBRE Limited Research, Q4 2013. Chart 5: Net Absorption 600 Central Suburban SF (000s) 400 4 200 0 -200 -400 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Source: CBRE Limited Research, Q4 2013. © 2014, CBRE Limited, Real Estate Brokerage As vacancy rates continue to rise, absorption remains negative for the third consecutive quarter. The Q4 2013 195,090 sq. ft. of negative absorption bring the net annual figure to negative 322,426 sq. ft. This is the first year since 2003 where the GTA has posted negative absorption. This negative figure would have been even lower had this quarter’s partially-leased completions not been included in the numbers. Quarterly absorption was negative in all GTA markets, with the exception of Downtown. However, a large contributor to positive absorption in the Downtown market is the completion of MaRS Phase 2. As previously noted, absorption figures do not necessarily paint a complete picture of the health of a market. While vacancies seem to be outpacing leasing, the GTA remains healthy in terms of renewal activity, particularly in the Suburban market. 4

- 5. The Downtown market exhibited the single largest quarterly vacancy increase since the Q3 2009. Vacancy rose by 80 basis points QoQ to end the year at 5.9%. While this is the highest vacancy in three years, it is nonetheless below the 10-year average of 6.9%. After fluctuating around 6.0% during the course of 2013, vacancy in the Midtown market is back up to 2012 levels, ending the year at 7.4% and rising by 130 basis points from Q3 2013. Leasing activity varies by class. Renovated and Converted (RC) product continues enjoying strong tenant demand. Conversely, vacancy in Class A space is on the rise as demand for large blocks of space diminishes. Class A sublease vacancy continues rising, up by 140 basis points QoQ to 26.2% of all vacancy. We anticipate vacancy to continue rising in the coming quarters and 2014 to be a muted year for large tenant deals. Vacancy increased in all submarkets, with the exception of the Greater Core. The largest vacancy increase occurred in the Downtown North submarket, due primarily to the addition of 402,080 sq. ft. of vacant space at the newlycompleted MaRS Discovery District’s 740,000 sq. ft. Phase 2. The Completion of MaRS Phase 2 in Q4 2013 signalled the commencement of the current Downtown construction cycle. An additional 5.1 million sq. ft. are expected to be completed through 2017. This vacancy increase comes on the back of 193,321 sq. ft. of negative absorption in Q4 2013. Absorption gains in the first half of 2013 were all but erased by negative absorption in the second half of the year, brining net annual absorption to a mere 10,161 sq. ft. The largest vacancy increase was felt in the Eglinton and Yonge Submarket, where vacancy rose by 310 basis points QoQ to end the year at 10.8%. The two largest contributors to this rise in vacancy are the Thomas Cook sublease at 75 Eglinton Avenue E and a number of new vacancies at 477 Mount Pleasant Road. Toronto Office | MarketView MIDTOWN MARKET Q4 2013 DOWNTOWN MARKET Leasing activity throughout the entire Midtown market remains confined to the sub-10,000 sq. ft. deals. In the St. Clair and Yonge submarket, this is caused by a shortage of large blocks of space. In the Bloor and Yonge and Eglinton and Yonge submarkets, this is caused by a lack of large tenants on the market. Consequently, vacancy is expected to remain flat in the coming quarters. Select Downtown market transactions this quarter include: • LinkedIn leased 37,000 sq. ft. at 250 Yonge Street • Shepell fgi expanded by 32,000 sq. ft. at 800 Bay Street • CNW Group leased 22,000 sq. ft. at 88 Queens Quay West Select Midtown market transactions this quarter include: • Crowe Soberman renewed 33,500 sq. ft. 2 St Clair Avenue East • Thomas Hannam Medicine Professional Corporation leased 21,500 sq. ft. at 160 Bloor Street East • UNICEF renewed 15,000 sq. ft. at 2200 Yonge Street FINANCIAL CORE DOWNTOWN WEST For the fourth consecutive quarter, vacancy in the Financial Core Submarket increased, up 40 basis points QoQ to 6.2% in Q4 2013. Vacancy in the Downtown West submarket continues its upward trajectory, up by 70 basis points QoQ to 6.5% in Q4 2013. Absorption is back in negative territory after posting moderate gains in Q3 2013, down to negative 60,690 sq. ft. in Q4 2013. This quarter’s 91,892 sq. ft. of negative absorption brought the net annual absorption figure up to negative 419,816sq. ft. This is the first time the Financial Core submarket posted negative annual absorption since 2008 and is the highest amount of negative annual absorption since 2003. Sublease vacancy as a percentage of total vacancy continues rising, up by 210 basis points to 27.7%. This figure is expected to increase further as futuredated available space becomes vacant in the coming quarters. Leasing activity has slowed somewhat, but demand factors remain. Lease expiry profiles continue to drive deal activity and tenants continue to look for office space. Net effective rents are holding firm, with landlords not sensing much downside risk yet. As more space comes on the market in future quarters, landlords’ Net Effective Rent expectations may moderate. Select Financial Core transactions this quarter include: • Sentry Investments renewed and expanded to 46,500 sq. ft. at 199 Bay Street • CIBC subleased 45,000 sq. ft. at 130 Adelaide Street West • Power Corp leased 17,000 sq. ft. at 161 Bay Street © 2014, CBRE Limited, Real Estate Brokerage The largest contributor to Downtown West vacancy is 277 Front Street West, where 112,985 sq. ft. of space has come on the market. This is former Royal Bank of Canada space, which the Bank is vacating to relocate into 180 Wellington Street West and RBC WaterPark Place. While overall vacancy is on the rise, vacancy in RC Class space decreased by 30 basis points since Q3 2013. The last two years have seen RC vacancy at historical lows, which speaks to the attractiveness of this class of space. Few available large blocks and heightened tenant demand will likely see this class of space continue to enjoy low vacancy rates. Class A vacancy is also on the decline, decreasing by over half from 7.3% to 3.1% QoQ. The completion of QRC West in 2015 will alleviate this supply crunch by adding 285,581 sq. ft. to inventory. Select Downtown West transactions this quarter include: • Shopify leased 28,500 sq. ft. at 80-82 Spadina Avenue • John Street Inc. renewed 21,500 sq. ft. at 172 John Street • Workplace One Consulting Inc. leased 20,00 sq. ft. at 901 King Street West 5

- 6. The vacancy increase was accompanied by 216,406 sq. ft. of net negative absorption for 2013. This increase was largely concentrated in the Toronto North market, due primarily to the 100,158 sq. ft. Proctor & Gamble sublease at 4711 Yonge Street. Despite the vacancy increase, leasing activity remains strong in the Suburban market, particularly in the West market, which enjoyed a number of large leasing transactions in Q4 2013. Three buildings totalling 163,699 sq. ft. were completed in Q4 2013– two in the West market and one in the North market. In addition to these completions, eight new buildings were announced this quarter. These announcements will see an additional 685,615 sq. ft. of space completed over the next two years. Select Suburban market transactions this quarter include: • Compass Group Canada leased 63,000 sq. ft. at 1 Prologis Boulevard, Mississauga • Worley Parsons leased 62,000 sq. ft. at 1004 Middlegate Road, Mississauga • MPAC leased 15,000 sq. ft. at 100 Via Renzo Drive, Richmond Hill Activity in the North market has slowed somewhat since Q3 2013, with vacancy rising by 120 basis points QoQ to end the year at 7.3%. Vacancy rose most significantly in the North Yonge Corridor submarket, due primarily to the 100,158 sq. ft. Procter & Gamble sublease at 4711 Yonge Street. This space is the main contributor to sublease vacancy in the North market, which rose by 125 basis points to 35.1% of all vacant space. This is the highest sublease vacancy of all GTA markets. 191 Creditview Road was completed this quarter, adding 62,500 sq. ft. to competitive inventory. Since the building was delivered fully-leased, it also contributed 62,500 sq. ft. to absorption. Without it, absorption in the North market would have been negative 141,597 sq. ft. instead of the negative 79,097 sq. ft. actually posted. Toronto Office | MarketView Vacancy in the Toronto Suburban market increased by 40 basis points to 13.1% in Q4 2013. This is the highest vacancy this market has experienced since Q2 2005. NORTH MARKET Q4 2013 SUBURBAN MARKET Average asking rental rates decreased by $0.90 to $17.49 per sq. ft. , dropping most significantly in Class A space in the North Yonge Corridor. This is due primarily to a $3.50 asking rent decrease at 36 York Mills Road. Select North market transactions this quarter include: • Mackenzie Health leased 6,500 sq. ft. at 7880 Keele Street, Vaughan • Money Express leased 5,500 sq. ft. at 5075 Yonge Street, Toronto • Shell leased 5,000 sq. ft. at 90 Sheppard Avenue East, Toronto EAST MARKET WEST MARKET Vacancy in the East market continues inching upwards, rising by 40 basis points QoQ to 12.4% in Q4 2013. This vacancy increases comes with 104,147 sq. ft. of negative absorption, the majority of which occurred in Class A space. Vacancy in the West market rose slightly, up by 10 basis points since Q3 2013 to end the year at 15.7%. Quarterly absorption dipped back into negative territory, registering at negative 33,162 sq. ft. and erasing gains seen in Q3 2013. While relocation deals still exist, tenant activity in the East market continues being skewed more heavily towards renewals than relocations. Given the relative lack of inter-submarket tenant migration activity, landlords are aggressive in seeking new tenants. Despite the relative shortage of relocations, net effective rents remain stable. Relocation costs are prohibitively high, allowing landlords to extract higher net effective rents on renewals. Construction activity remains muted in the East market, with no space under construction for the third consecutive quarter. A number of planned projects are expected to break ground in the coming quarters, particularly in the Markham North/Richmond Hill submarket. Select East market transactions this quarter include: • Scotiabank leased 81,000 sq. ft. at 300 Consilium Place, Scarborough • RBC renewed 78,000 sq. ft. at 260 East Beaver Creek, Richmond Hill • MPAC leased 15,000 sq. ft. at 100 Via Renzo Drive, Richmond Hill © 2014, CBRE Limited, Real Estate Brokerage Despite the rising vacancy, leasing activity is accelerating in the West market. The West market saw the highest number of large deals over 100,000 sq. ft. of all GTA markets. However, since many of these tenants were densifying and consolidating their space, the excess space they gave up contributed to negative absorption for the quarter. The completion of 7205 Hurontario Street and 3430 Superior Court added a total of 101,199 sq. ft. of new supply to the Toronto West market in Q4 2013, bringing overall 2013 completions to 505,911 sq. ft. Given the recent high levels of leasing activity coupled with new supply, we anticipate the Toronto West market to continue to experience increasing leasing velocity. Select West market transactions this quarter include: • Royal Bank of Canada renewed 800,000 sq. ft. at 6880 Financial Drive, Mississauga • Samsung Electronics Canada Inc. leased 125,000 sq. ft. at 2050 Derry Road W, Mississauga • Ericsson Canada leased 69,500 sq. ft. at 2425 Matheson Boulevard E, Mississauga 6

- 7. Q4 2013 Toronto Office | MarketView CONTACTS For more information about this Toronto MarketView, please contact: Toronto Research Masha Dudelzak, MBA Senior Research Analyst CBRE Limited 145 King Street West Suite 600 Toronto, Ontario M5H 1J8 t: +1 416 815 2316 e: masha.dudelzak@cbre.com FOLLOW US Global Research and Consulting This report was prepared by the CBRE Canada Research Team, which forms part of CBRE Global Research and Consulting – a network of preeminent researchers and consultants who collaborate to provide real estate market research, econometric forecasting, and consulting solutions to real estate investors and occupiers around the globe. Disclaimer 7 Information contained herein, including projections, has been obtained from sources believed to be reliable. While we do not doubt its accuracy, we have not verified it and make no guarantee, warranty or representation about it. It is your responsibility to confirm independently its accuracy and completeness. This information is presented exclusively for use by CBRE clients and professionals and all rights to the material are reserved and cannot be reproduced without prior written permission of the CBRE Global Chief Economist. © 2014, CBRE Limited, Real Estate Brokerage

- 8. CANADIAN MARKET OUTLOOK 2014

- 9. SELECT A MARKET YUKON TER RITORY NORTHWEST TER RITORIES NUN AV UT BRITISH COLUMBIA A L B E R TA EDMONTON S A S K ATC H E WA N M ANITOBA VICTORIA VANCOUVER CALGARY WINNIPEG THUNDE W CANADIAN MARKET OUTLOOK 2014

- 10. CLICK YELLOW DOT TO ACCESS MARKET INFO CLICK NAVIGATION BUTTON TO CONTINUE TO NATIONAL OVERVIEW NEWFOUNDLAND & LABR ADOR ST. JOHN’S QUÉBEC O N TA R I O MONCTON ER BAY NEW BRUNSWICK SAINT JOHN OTTAWA KITCHENER WATERLOO REGION WINDSOR PRINCE EDWA R D ISLAND NOVA SCOTIA HALIFAX MONTRÉAL TORONTO LONDON CLICK FOR .PDF (PRINTABLE COPY)

- 11. CLICK HERE FOR MARKET STATISTICS NATIONA Steady and stable may be the overall conjecture for Canada’s commercial real estate market in 2014, but that’s not to say there won’t be dynamic elements. In addition to tremendous development in many industrial markets across the country, pockets of retail and office space are expected to record increased demand for space in the coming year. For the first time in decades, multi-housing construction is on the rise and rental stock is growing in various markets across the board. CANADIAN MARKET OUTLOOK 2014

- 12. HOME AL OVERVIEW With Canada in the midst of a new development cycle, it’s safe to say most markets and property types are responding to healthy demand by building a significant amount of new commercial real estate. While the full impact of this new supply won’t be apparent for several years, the numbers are already impressive with some 6.0 million SF of office space coming into the market in 2014. In the meantime, a lack of volatility in the Canadian economy coupled with steady job growth continues to keep Canada on the radar for new capital investment. 5

- 13. THE PLACE TO KEEP INV Indications are that the U.S. Federal Reserve will begin to unwind monetary stimulus in 2014 and interest rates will rise. But Canada is expected to remain a hotspot for foreign and local investors nonetheless. With REITs pulling back on purchases, their retreat has private equity and pension funds clamouring to fill the void. This trend suggests that there is more depth and resilience to the purchaser pool than was initially expected. “It won’t become any easier to secure prime commercial real estate assets because domestic pension funds are increasing their allocation to real estate.” Peter Senst President Canadian Capital Markets CANADIAN MARKET OUTLOOK 2014

- 14. NVESTING Indications are that the U.S. Federal Reserve will begin to unwind monetary stimulus in 2014 and interest rates will rise. But Canada is expected to remain a hotspot for foreign and local investors nonetheless. With REITs pulling back on purchases, their retreat has private equity and pension funds clamoring to fill the void. This trend suggests that there is more depth and resilience to the purchaser pool than was initially expected. “We’re seeing the big global sovereigns trying to find a way to come into this country because we don’t have the volatility of other countries,” says Peter Senst, President of Canadian Capital Markets at CBRE Canada. “It won’t become any easier to secure prime commercial real estate assets because domestic pension funds are upping their allocation to real estate.” He believes the search for stable income producing investments will continue to attract capital throughout 2014. He also advises against “writing off” the REITs just yet. “The biggest and best will flourish,” he says. “But there’s no doubt we’ll still be delivering REIT offerings into the market.” Upcoming infrastructure development will also be a key factor in determining future capital investment in many sectors of the country—and where commercial development will take place. The growing trend towards urbanization will be dependent on solid transportation links, while ongoing expansion in Western Canada will rely on future oil sand development. 7

- 15. David Montressor Executive Vice President, National Apartment Group Multi-housing assets will continue to be appealing to investors, but as in previous years, a lack of product could be a challenge. “There’s a real appetite for ‘centre ice’ and quality Class B multi-residential properties,” says David Montressor, CBRE Limited’s Executive Vice President, National Apartment Group. This continued strong interest is due to the stable, predictable returns the asset class offers. Capital preservation with steady annual returns and debt repayment continues to be the driving force that attracts capital to multi-housing. “Going forward, interest in building purpose built rental is expected to increase due to the lack available quality properties.” Montressor thinks that there’s little that could shake this market in 2014 unless central banks lose control and interest rates skyrocket. That being said, if rates spike, there will be no place to hide and multi-housing would continue to be the best dirty shirt in the laundry basket, with low vacancies allowing for the ability to generate cash flow while building equity through debt repayment. “There’s a real appetite for ‘centre ice’ multi-residential properties.” CANADIAN MARKET OUTLOOK 2014

- 16. 9

- 17. A RETAIL EV “Never before in Canadian retail history has the department store segment been the subject of so much focus or been so heavily contested.” Tom Balkos Senior Vice President, Director, Retail Services Group CANADIAN MARKET OUTLOOK 2014

- 18. VOLUTION On the retail front, more and more U.S. and European retailers are looking at Canada as their next go-to destination. With high-end U.S. retailers like Nordstrom and Saks Fifth Avenue setting up shop in the next few years, big-anchor indoor mall concepts continue to garner significant attention from investors and tenants. “Never before in Canadian retail history has the department store segment been the subject of so much focus or been so heavily contested,” says Tom Balkos, Senior Vice President and a Canadian Director of the Retail Services Group. With Loblaws buying Shoppers Drug Mart, and Sobeys purchasing Safeway, sources of new demand for retail space and portfolio restructuring efforts are already underway. The past year has also shown the success of dominant centres in secondary markets, while second-tier retailers in the same arenas are having a harder time. With supply tight, those looking to enter the Canadian market are expected to come in smaller private label, store-in-store formats or by creating mall space with their own private brands and under their own banners. “With all the trading of large block retail space we’re witnessing, now is a unique period of time that only happens every 30 years,” says Balkos. As the U.S. economy continues to pick up speed, however, it’s also becoming a bigger competitor for retailer expansion dollars than we’ve seen in the past several years. While Balkos says retail space in Canada is highly sought after, he points to the possibility of higher interest rates as a potential game changer. “Interest rates will affect consumer confidence and while I think it will be a consistent year it may not be one of great retail sales growth,” he says. 1 1

- 19. MORE OFFICE MORE EFFICIE While a downtown office construction cycle is underway, many office tenants are reducing the size of their real estate footprint and embracing new workplace strategies. “These tenants are reducing square footage per employee and redesigning the workplace to drive collaboration and productivity,” says John O’Toole, Executive Vice President and Executive Managing Director at CBRE Limited. “Economics are clearly a primary driver but it’s also about tenants making better use of their physical environment - doing more with less.” With these new builds offering a whole different set of attributes in terms of performance, O’Toole says older buildings 2010 CANADIAN MARKET OUTLOOK 2014 will eventually have to be adapted to meet new workplace models. “Right now we’re keeping an eye on the new supply and the old as they both have their place, but it’s really a wait-and-see environment in the office space for the next year as new projects are completed,” he says. Whether there is too much office construction for the demand, as some critics suggest, remains to be seen. The development boom in the office sector reflects a calculated bet on future demand for space, steep competition for tenants and the fact that investors hope to reap more benefits from new construction than purchasing what is already built. 2013 In is g tha thro effi new dev wil inv new Ar the dol ab our reto ultr

- 20. E TOWERS, ENT TENANTS the meantime, the industrial sector going strong and is expected to stay at way in many parts of the country rough 2014. The lack of modern, high iciency space will continue to support w construction, however prohibitive velopment fees in some municipalities ll continue to prompt developers to vest in old buildings rather than build w. recent resurgence in manufacturing in e U.S., coupled with a weaker Canadian llar, also puts Canadian exporters in better position to compete; however, r manufacturing sector still needs to tool and reinvest to thrive in today’s ra-competitive manufacturing market. “Tenants are reducing square footage per employee and redesigning the workplace to drive collaboration and productivity.” 2017 John O’Toole Executive Vice President and Executive Managing Director, Toronto

- 21. THE TECHNO CANADIAN MARKET OUTLOOK 2014

- 22. OLOGY TREND The cumulative effect of technology on all aspects of the real estate market is not to be discounted. In the office sector, the condensed employee footprint is indicative of a more mobile workforce that is using technology to make business functions feasible from any location. In the retail market, the rise of online sales is negating the need for as many storefronts, and is also enabling standard retail centres to act as mini-warehouses to store the products that are being shipped cross-country. The industrial sector too is feeling the technology tug as retailers ramp up their online sales divisions and expand their fulfillment centres. Technology is capable of driving change in all sectors of the economy, but more than at any time in recent memory, commercial real estate decisions will be impacted by technological advancements and changing business practices. 15

- 25. CLICK HERE FOR MARKET STATISTICS VANCOUVER “When it comes to investment, Vancouver remains a highly liquid market compared to any other city in Canada, particularly in the urban core.” Mark Renzoni 2014 MARKET OUTLOOK President & CEO, CBRE Limited

- 26. R MARKET If a robust investment market is indicative of confidence in overall economic and leasing fundamentals, then 2014 looks promising for Vancouver. The investment market continues to thrive as demand for core real estate downtown and quality property in key suburban nodes persists from local and foreign investors. “When it comes to investment, Vancouver remains a highly liquid market compared to any other city in Canada,” says Mark Renzoni, President and CEO of CBRE Limited in Canada. “The money that comes here is betting on strong fundamentals and appreciation.” Further, Vancouver is one of the most expensive multi-residential markets in North America, and this market still maintains its strong appeal to foreign, private and institutional buyers. There continues to be a shortage of investable product across all asset classes and Renzoni is optimistic that we’ll see at least as many trades in 2014 as we saw in 2013.

- 27. Vancouver Investment Volume (millions) $4,500.0 sector and the trend is expected to continue through 2014. $4,000.0 $3,500.0 $3,000.0 $2,500.0 $2,000.0 $1,500.0 $1,000.0 $500.0 $2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 P F The industrial sector hit an encouraging note toward the end of 2013 with a distinct upward trend in leasing and sale velocity. “Our forecasts are showing that industrial demand is continuing to increase,” says Renzoni, noting that 2014 has the potential to be a strong industrial market, which will further support the current development cycle for 2014 through 2016. Source: CBRE Limited, RealNet Canada Office tower construction is at an all-time high in Vancouver, especially downtown. Pent-up demand for new office product has resulted in pre-leased rates of 70%—and demand for new office space is expected to continue in 2014. On the flip side, the recent lack of job growth and interprovincial migration has been disappointing, which has impacted the office market in the shortterm. There has been an uptick in subleases coming onto the market from the resource Construction in downtown Vancouver Robson St. , Vancouver The retail sector is also an area of strength as expansion in existing shopping centres and a handful of new projects is resulting in strong leasing activity. With Nordstrom coming into the market in 2015, Renzoni says there is a sense of urgency for retailers to position themselves in the centre of the action. “There’s lots of excitement with new projects and existing expansions, which should result in a very positive market in the CANADIAN MARKET OUTLOOK 2014

- 28. higher traffic nodes in urban and suburban areas,” he says. “These new stores act as a catalyst for change and rejuvenation.” We will see continued success for the higher-end retail concepts. Perimeter Road, which are all expected to positively impact the retail and industrial sectors. Substantial changes to key parts of metro Vancouver’s infrastructure, include the Evergreen SkyTrain Line, the completion of the Port Mann Bridge and the South Fraser PROJECTS TO WATCH THE EXCHANGE OFFICE TOWER PACIFIC CENTRE OFFICE DEVELOPMENT PARK ROYAL SHOPPING CENTRE EXPANSION YVR AIRPORT LUXURY OUTLET CENTRE SOUTHEAST FALSE CREEK NEIGHBOURHOOD 21

- 31. CLICK HERE FOR MARKET STATISTICS CALGARY MARKET “We’re 100% leased by the grand opening of a mall. That speaks to the fact that disposable incomes in Calgary continue to outpace the national average.” Greg Kwong Executive Vice President & Regional Managing Director, Alberta 2014 MARKET OUTLOOK

- 32. “While the outlook for Calgary’s commercial real estate market is looking relatively stable, ‘hot spots’ in the retail, industrial and suburban office markets should keep things hopping throughout 2014,” says Greg Kwong, Executive Vice President, Regional Managing Director for CBRE Limited’s Calgary operations. Alberta’s largest city is in the midst of a development cycle encompassing some 6.3 million SF and is expected to last for the next three to five years. In the interim, however, demand for office space is low and there is little expectation for any significant tenant moves in the downtown core for 2014. On the multi-residential side, the development of Seton Village is expected to have a positive impact on the downtown core, drawing a whole new population of people who are choosing a more urban lifestyle. “It will certainly change what is now deemed to be a tired and undesireable area,” says Kwong.

- 33. Despite ongoing issues involving the approval of the Keystone XL Pipeline Project, and talk of a pullback in the energy sector, Alberta’s largest city is still attracting up to 30,000 new residents a year. Kwong says the slowdown in the oil patch is a challenge and layoffs are a reality, but he is confident the market will bounce back as it has in previous years. “The market here is pretty resilient,” he says. Calgary Population Change 50,000 40,000 30,000 20,000 A notable infrastructure project that is expected to impact the market is the southeast ring road expansion, a network of freeways, interchanges and bridges. The expansion of the airport that is currently underway is also significant and will include a host of new hotels as well as one of the longest runways in the country. The Calgary retail market continues to show positive growth with low vacancy in both urban and suburban areas. “We’re 100% leased by the grand opening of a mall,” says Kwong. “That speaks to the fact that disposable incomes in Calgary continue to outpace the national average.” 10,000 (10,000) (20,000) 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 Population Increase International Migration Natural Increase Interprovincial Migration InterCity Migration Nordstrom will open its first store in Canada in Calgary’s Chinook Centre this year. “There are some other major U.S. retailers looking at Calgary and I suspect they are going to wait and see how Nordstrom does in its first Source: Conference Board of Canada CANADIAN MARKET OUTLOOK 2014

- 34. year,” says Kwong. And where there are major retailers like Nordstrom setting up shop, Kwong says that distribution operations are likely to follow. In fact, major players are expected to continue to open large distribution centres in Calgary. As a result, the area’s industrial market is expected to maintain stable rental rates in 2014. any other municipality in Canada, the government controls 80% of developable land in Calgary, and they distribute it as they see fit,” he says. Interest from Canadian and U.S. investors in a variety of commercial property types should stay strong. Calgary is holding to its reputation as a good place to do business. If there was one ongoing challenge in Calgary’s industrial market worth noting, it would be inadequate land supply and construction costs, says Kwong. “Unlike PROJECTS TO WATCH QUARRY PARK – SUBURBAN OFFICE PARK EAST VILLAGE CALGARY’S CHINOOK CENTRE CENTURY DOWNS RACETRACK AND CASINO IN BALZAC KEYSTONE XL AND NORTHERN GATEWAY PIPELINES CALGARY INTERNATIONAL AIRPORT $2.0 BILLION AIRPORT DEVELOPMENT PROGRAM 27

- 37. CLICK HERE FOR MARKET STATISTICS EDMONTON M “I’m expecting 2014 to be as good a year as the one just past for the industrial market, which was one of our best years ever.” Dave Young Executive Vice President & Managing Director, Edmonton 2014 MARKET OUTLOOK

- 38. MARKET Amidst modest expectations for the overall commercial real estate market in 2014, Canada’s energy powerhouse looks set to buck the trend. Even with some challenges facing Canada’s energy sector, Edmonton’s industrial market is booming, multi-housing development is increasing and suburban office continues to show impressive growth. “Global demand for our resources is insatiable,” says Dave Young, Executive Vice President and Managing Director of CBRE Limited’s Edmonton operations. “It’s not just extraction of raw materials which still is an important contributor to the economy but there is so much technology being developed here in our research and development facilities that is making energy extraction better—it is a huge industry in its own right.” The energy companies have made extremely large and long-term commitments to the region which will bode well for the overall Edmonton economy.

- 39. Construction costs and labour shortages aside, Young is confident the industrial market will drive the commercial market forward for the foreseeable future. Massive development projects underway in the central and northern parts of the province are also making way for the companies that service them. “As Fort McMurray and Northern Alberta grow, Edmonton grows, the province grows, the country grows,” believes Young. “I’m expecting 2014 to be as good a year as the one just past for the industrial market, which was one of our best years ever.” North American Industrial Markets Ranked by Rent (per SF per annum) 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 Market SAN JOSE SAN DIEGO EDMONTON OTTAWA CALGARY VANCOUVER ORANGE COUNTY HALIFAX LOS ANGELES WINNIPEG PHOENIX SEATTLE DENVER NEW JERSEY NORTHERN HOUSTON MIAMI MONTREAL SACRAMENTO TORONTO BALTIMORE MINNEAPOLIS/ST. PAUL NEW JERSEY CENTRAL INLAND EMPIRE WATERLOO REGION CLEVELAND Net Asking Rent ($CAD) 13.85 13.66 10.79 8.53 8.10 7.96 8.42 7.43 7.72 6.79 7.02 6.80 6.49 6.26 6.09 5.96 5.17 5.36 5.04 5.32 5.28 5.18 4.85 4.53 4.80 With the prevalence of construction, engineering and service companies setting up offices in Edmonton, Young expects growth in the suburban office market to stay positive in 2014, particularly on the south side of the city. “We’re continuing to see growth and demand in our suburban markets and we expect vacancy to decline even with the addition of new product to the inventory,” he says. The downtown office sector is a little more challenging, not for a lack of growth but because of the potential for excess supply. “There are two or three prospective towers downtown that could be potential game changers,” says Young. “With the advent of a number of new towers, current vacancy levels could rise above 14.0% based on our 10-year average annual absorption of 128,000 SF. The new space is needed as large users are unable to expand but there will be an impact to vacancy in the core.” With the construction of Edmonton’s new Roger’s Place (future home of the Edmonton Oilers), and the mixed-use development surrounding the arena set to begin in 2014, the city is poised to keep growing. “The arena district will change downtown and will be a catalyst for other development,” says Young. “The opportunity for downtown after 5 p.m. will be massive.” Other infrastructure projects, such as the expansion of the city’s LRT and various highway extensions, are also Source: CBRE Limited CANADIAN MARKET OUTLOOK 2014

- 40. expected to improve efficiencies and create more effective access to all areas of the city. On the retail front, the market is solid and Young says this growth is largely in tandem with the growth in the industrial and manufacturing industries. GDP growth of 3.2% and disposable income growing at 3.4% per annum in Edmonton makes for a very exciting environment for retailers. There are many new entrants to this market including, high-end retailers like Tiffany & Co and Samsung who have chosen West Edmonton Mall, Canada’s largest enclosed mall, for the first time as a viable place to set up shop. “Edmonton is a very affluent city and with all of the development in the region, we are forcast to lead the country in growth again in 2014. The retail business in the city will be strong and as the economy continues to grow, tenants will reap the benefits,” says Young. PROJECTS TO WATCH KELLY-RAMSEY BUILDING ROGERS PLACE KEYSTONE XL AND NORTHERN GATEWAY PIPELINES FORT MCMURRAY ENERGY PROJECTS 33

- 43. CLICK HERE FOR MARKET STATISTICS WINNIPEG MARKE “We’re not growing at an exponential rate but we have a stable economy and that’s spilling into most elements of the commercial market.” Trevor Clay Sales Associate, Winnipeg 2014 MARKET OUTLOOK

- 44. ET With a broad range of development projects underway and a population that keeps growing, the outlook for Winnipeg in 2014 is looking positive. “We’re not growing at an exponential rate but we have a stable economy and that’s spilling into most elements of the commercial market,” says Trevor Clay, Sales Associate for CBRE Limited’s Winnipeg operations. As a distribution hub for central Canada, Winnipeg’s industrial market is revealing a stark divide between demand for distributionfocused space versus manufacturing facilities. “There has been significant uptake of space in the distribution end of the market, but the older buildings and larger manufacturing spaces are tougher to fill,” he says. “We’re just not seeing large-scale deals done with manufacturing-focused tenants.”

- 45. Automotive and distribution companies are clearly driving the industrial sector. The recent completion of CentrePort Way, a highway in northeast Winnipeg is expected to be a huge boon for trucking companies and subsequent development in the CentrePort area. “The plan for CentrePort is to have that highway unlock large tracks of land for industrial development and provide access to rail transport as well,” he says. North American Industrial Markets Ranked by Availability Rate Market Availability Rate (%) 1 WINNIPEG 3.9 2 TORONTO 4.6 3 EDMONTON 4.7 4 ORANGE COUNTY 5.3 5 WATERLOO REGION 6.2 6 LOS ANGELES 6.2 7 HALIFAX 6.3 8 VANCOUVER 6.4 9 OTTAWA 6.5 10 DENVER 7.0 12 CALGARY 7.1 13 CINCINNATI 7.2 14 CLEVELAND 7.2 15 INLAND EMPIRE 7.6 16 MIAMI 7.8 17 MONTREAL 7.9 18 HOUSTON 8.2 19 CHICAGO 8.4 20 INDIANAPOLIS 8.5 21 PORTLAND 8.5 22 MILWAUKEE 8.6 23 COLUMBUS 8.7 24 SEATTLE 8.7 25 NEW JERSEY NORTHERN 9.5 Downtown, the $180.0 million expansion of the RBC Convention Centre is slated for completion in 2016 and is expected to completely transform the southern portion of the city centre. “With our airport completed and our football stadium now ready, I think the convention centre is the most substantial public project underway in Winnipeg by far,” says Clay. 6.8 11 MINNEAPOLIS/ST. PAUL The primary drivers for the office sector are less clear. “There’s really no one industry that I would tag as being the next big thing for Winnipeg on the office side,” says Clay. “It’s basically a tenant shuffle from downtown and back instead of new players coming into the market.” Demand for Class A property continues to be high with little vacancy, whereas dwindling demand for other classes is resulting in higher vacancy rates on the lower end. Source: CBRE Limited In terms of multi-housing, vacancy is increasing slightly in the rental market due to new supply. “As a lot of the older product is renovated and rents are pushed up, this has justified new construction,” says Clay. “We’ve had a lot of exciting projects come to Winnipeg in the last while as a result.” With commercial property ownership concentrated in the hands of a small number of local owners, Clay says larger players have little chance to break into the multi-housing arena. “For now, interest rates are still at CANADIAN MARKET OUTLOOK 2014

- 46. attractive levels and there is lots of local money looking for opportunities,” he says. The foray of major retail anchors like IKEA and Cabelas into Winnipeg has been a positive force for the retail sector as a whole. “The IKEA project at Seasons of Tuxedo has attracted the attention of a lot of retailers that hadn’t previously considered Winnipeg,” says Clay. With the next closest IKEA location some seven hours away in Minneapolis, Clay says the furniture giant is luring significant numbers of American as well as Canadian shoppers. Polo Park, the city’s largest enclosed mall, continues to draw significant interest from major retailers as well. PROJECTS TO WATCH SEASONS OF TUXEDO RBC CONVENTION CENTRE CENTREPORT 39

- 49. CLICK HERE FOR MARKET STATISTICS LONDON & KITCHENERWATERLOO REGION “In this mature market, I see opportunity ahead. No longer do I foresee anything that could be described as bleak.” Peter Whatmore Senior Vice President & Executive Director, Southwestern Ontario 2014 MARKET OUTLOOK

- 50. N When it comes to Southwestern Ontario’s commercial real estate outlook for 2014, it is a tale of two regions with very diverse prospects, says Peter Whatmore, Senior Vice-President and Executive Director of CBRE Limited’s Southwestern Ontario division. In the Kitchener and Waterloo areas, expectations are high that 2014 will be an active and robust year. Despite ongoing issues around one of the area’s biggest technology companies, consolidation of the tech sector is leading to growth in other areas says Whatmore, noting that it’s not a ‘gloom and doom’ scenario for the region by any means. “This is not a one-horse town and the reality of the tech sector here is that we have 30,000 employees in 800 companies,” he says. “In this mature market, I see opportunity ahead not anything that could be described as bleak.” Urban growth in the Kitchener and Waterloo area has been significant in terms of multi-residential and office developments, which is being largely driven by the tech sector and is expected to continue into 2014. In fact, there is an anticipated 400,000 SF of office space to be delivered in the next two to three years.

- 51. In the industrial sector, growth of the distribution market west of the Greater Toronto Area has been positive and continues to look promising for the coming year. A new light rail transit system in the works from north Waterloo to south Kitchener is also anticipated to have a big impact on future growth in Southwestern Ontario. “Wherever there is going to be a transportation hub there is the desire to acquire sites for future high density development,” says Whatmore. On a brighter note, with an abundance of prime industrial space being added to this sector, he says the future looks more promising for the London area than it has in a while. Whatmore points to the automotive sector, which is the strongest it has been since 2007, as an example. “Today everybody is at capacity, even if you look down the road to Windsor,” he says. “So conditions are certainly improving, but we still have challenges in the region.” Whereas investors are looking at KitchenerWaterloo as an area they can place bets on the future, Whatmore says they are viewing London with more trepidation. Plant closings and unemployment will continue to impact this market in 2014. “When the plants stop closing and people stop losing their jobs by the thousands, that’s when the stability will set in,” says Whatmore. Right-to-Work legislation in the U.S. also poses challenges from a competitive standpoint across the region. “We can’t ignore it and eventually we’re going to confront this or we won’t be cost-competitive.” Following Kitchener’s lead, academic institutions like Fanshawe College are acquiring buildings in the core, which is expected to bode well for urban growth. High office vacancy rates in London’s core can be attributed to several large retrofits, including the conversion of the Citi Plaza shopping mall into office space, but vacancies are expected to improve over the medium term. “It’s like new developments are being completed when demand isn’t all that robust,” says Whatmore. Unemployment Rate Canada London continues to experience solid demand from retailers. This largely stems from ongoing residential development in the area. Ontario Waterloo Region London 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% Source: Statistics Canada, December 2013 CANADIAN MARKET OUTLOOK 2014

- 52. The Tannery PROJECTS TO WATCH HANLON CREEK BUSINESS PARK NEW INTERNATIONAL TRADE CROSSING BRIDGE BETWEEN WINDSOR AND DETROIT 401 CORRIDOR ACCESS IMPROVEMENTS IN LONDON KITCHENER/WATERLOO KITCHENER – WATERLOO – CAMBRIDGE RAPID TRANSIT 45

- 55. CLICK HERE FOR MARKET STATISTICS TORONTO MA “We don’t know what business sector will emerge to dominate the market but we certainly see a steady increase in demand over the next five years as the economy expands.” John O’Toole Executive Vice President & Managing Director, Toronto 2014 MARKET OUTLOOK

- 56. ARKET It’s no secret that downtown Toronto is experiencing the largest office construction boom since the early 1990s. While anticipation mounts, the full impact of this building bonanza won’t be realized for several years yet. In the meantime, office sublet vacancy has risen steadily and is expected to continue increasing as the new buildings are completed and tenants relocate into them. With technology advancements and better workplace strategies, many office tenants are reducing their space per employee and frequently require less space when they relocate. “This is not a unique trend to Toronto. We’re seeing this all over the industrialized world,” says John O’Toole, Executive Vice President and Executive Managing Director at CBRE Limited. “Tenants are trying to get better performance out of their people and their buildings through better space optimization.”

- 57. While many large office tenants have already completed their renewal or relocation deals, sources of demand are not yet fully depleted. For one, small office tenants have typically been a steady source of demand for Class A downtown properties and this should remain constant through 2014. There are also those tenants with expiring leases who are waiting on the completion of new builds before making their real estate decisions. New Build Pre-lease Activity Million SF Leased 2009 10 Tenants Took an additional 764,000 SF of total space (31%) 3.2 2.4 Million SF Leased Leasing Giving Back 2014 trend for tenants moving downtown has already begun and the potential for U.S. companies moving into Toronto, and other Canadian industries needing more space as they grow, should not be underestimated. But landlords haven’t reduced rents or provided any notable concessions and aren’t expected to do so, at least for the first part of 2014. “The city has come a long way over the last few years in terms of multi-use buildings and amenities.” With retail construction on the rise (Toronto represents more than 50% of the total retail space under construction across the country), the Greater Toronto Area (GTA) continues to rank in the top tier of most desirable locations for foreign and domestic retailers. While demand is high, large blocks of available space remain a rare commodity. 15 Tenants Giving back 498,000 SF of total space (15%) 2.7 Leasing 3.3 Giving Back Source: CBRE Limited With many large tenants having already completed their deals, there is some uncertainty as to where new sources of demand will come from. “We don’t know what business sector will emerge to dominate the market but we certainly see a steady increase in demand over the next five years as the economy expands,” says O’Toole. The Infrastructure developments like the Union Station revitalization and Metrolinx bode well for all sectors. For the industrial sector, Metrolinx will have the single largest impact on the way the GTA functions as it creates more routes for the transportation of goods,” says CBRE Limited’s Senior Vice President & Managing Director John Haire. From an investment point of view, he says the Region of Durham has become an unexpected hotspot for manufacturing and the inevitable retail and residential growth that is sure to follow. “We’ve seen a real CANADIAN MARKET OUTLOOK 2014

- 58. resurgence in land sales and that bodes well for the east side of the GTA,” he says. Vaughan and Mississauga are other suburban industrial nodes that will continue to perform well not only because of the available industrial space in these municipalities, but also due to their pro-business mentality. However, all municipalities face development barriers as Haire points to prohibitive developmental charges that are prompting developers to invest in existing older buildings rather than building new. Although availability is below 5% in the industrial sector, Haire says landlords are also struggling. “Rental rates have to increase to the level that would make it economically viable for landlords to build.” PROJECTS TO WATCH 1 YORK, 100 ADELAIDE (ERNST & YOUNG TOWER), BAY ADELAIDE CENTRE EAST AND RBC WATERPARK PLACE THE BUTTONVILLE REDEVELOPMENT WEST DON LANDS UNION/SPADINA METROLINX THE BIG MOVE (SEVERAL PROJECTS) UNION STATION REVITALIZATION 51

- 61. CLICK HERE FOR MARKET STATISTICS OTTAWA MAR “A lot of U.S. retailers are establishing themselves in Ottawa before testing larger markets like Montreal.” Greg Clark Vice President & Managing Director, Ottawa 2014 MARKET OUTLOOK

- 62. RKET With the public sector continuing to relocate some of its operations to the suburbs and loosen their grip on the downtown market, Ottawa’s office market continues to feel the effects. “We’re certainly softening in the core and while it won’t be catastrophic, the impact will be most pronounced in the Class B and C properties in 2014,” says Greg Clark, Vice-President, Managing Director of CBRE Limited’s operations in the National Capital Region. “We’re in a tenant’s market for the first time in 15 years.”

- 63. Ottawa Downtown Vacancy Rate 8.0% 7.0% 6.0% 5.0% 4.0% 3.0% 2.0% 1.0% 0.0% 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Source: CBRE Limited While the private sector is leading the way in terms of office space efficiency, the public sector is also making the shift by implementing the Government of Canada Workplace 2.0 Fit-up Standards and reducing office space per government employee. Clark says growth in private sector and its corresponding demand for office space in downtown Ottawa has been minimal. However, some deals are still occurring and, while several large companies are relocating offices in the core, many are simply recalibrating to make better use of space. “Some of these companies have been captive audiences just waiting for available space but they’re not increasing their square footage,” says Clark. Demand for condos in the core has also been shrinking over the past year. In terms of investment, Clark expects the appetite for Class A product to stay strong despite the current softening in the market. “I think that everyone believes that once the budget gets nailed down, the federal government will come back and bolster the market,” he says. Ottawa is constantly undergoing infrastructure updates, but Clark says it’s the $2.13 billion light rail transit now under construction that has the most potential to change where the future growth of the city will occur. “Ottawa is currently a bus city, but I see intensification and the creation of mixed-use development around those LRT stations,” he says. Highway 417, which is one of Ottawa’s major highways, is also being widened to ease traffic flow. As a smaller market, Ottawa’s industrial sector is expected to stay relatively stable for the coming year. Ottawa’s industrial inventory is aging, but continues to boast some of the highest rental rates in the country because of limited stock and CANADIAN MARKET OUTLOOK 2014

- 64. limited development. Pockets of space are becoming available outside the greenbelt; however, demand for this newer product is still relatively low. “There are a lot of people who would say Ottawa is suffering because it doesn’t have an ample supply of strategically located employment land,” says Clark. The retail sector has proven solid over the last while, and Clark says we can expect that trend to continue in 2014. “A lot of U.S. retailers are establishing themselves in Ottawa before testing larger markets like Montreal,” he says. The new Tanger Outlet Mall, set to open in Kanata in 2014, is an upscale project that has lured big name retailers like Brooks Brothers and Nike. Furthermore, Nordstrom will be launching its Ottawa location in the Rideau Centre, downtown, in early 2015. “It’s no longer just Montreal that is the fashion destination in the region,” says Clark. PROJECTS TO WATCH 150 ELGIN OTTAWA OTTAWA LIGHT RAIL TRANSIT SYSTEM TANGER OUTLET MALL/KANATA 57

- 67. CLICK HERE FOR MARKET STATISTICS MONTREAL MA “Montreal is committed to a number of investments in infrastructure which are expected to improve efficiencies and continue to bring the population downtown as these projects progress.” Alexandre Sieber Senior Vice President & Senior Managing Director, Quebec 2014 MARKET OUTLOOK

- 68. ARKET Moderate growth across all real estate sectors should result in an overall stable market for Montreal in 2014. With a number of large buildings trading hands in 2013, and several office towers now under construction, activity in the office sector is expected to be modest over the coming year. As in other Canadian centres, office footprints are decreasing in the downtown core as companies downsize and seek alternate space elsewhere. The market is watching closely as the volume of sublet space approaches its highest peak since the recession. However, downtown sublet space as a percentage of overall vacant space, at 22.2% in Montreal, remains just below the downtown national average of 23.5%.

- 69. Montreal Percentage of Vacant Space for Sublet 30.0% 25.0% 20.0% 15.0% 10.0% 5.0% 0.0% 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Montreal Downtown All Classes National Downtown All Classes Source: CBRE Limited In the meantime, areas like midtown Montreal are gaining momentum as “companies are getting wiser about space utilization and efficiency gains are becoming more and more part of the strategic decisions,” says Alexandre Sieber, Senior Vice-President and Senior Managing Director of CBRE’s Quebec operations. “If I’m a bank with seven floors, do I need my back-office downtown or can I relocate it to midtown?—that’s the question tenants are considering,” says Sieber. On the other hand, demand for downtown office space is coming from new sources, such as national and International banks, who are setting up operations or coming back to the core because they see it as one of the few places left where they can still grow and take market share from local players. He also points to large tenants seeking to move from older buildings to new generation space as a trend that should continue in the coming year. As home to the second-largest aeronautic industry in the world, Sieber says logistics and transportation related spin-off companies are finding a home in Montreal. He believes IT outsourcing businesses and the gaming industry, which has almost 100 companies operating in the province, are other sources of potential growth. With several large transportation projects in the works, including the reconstruction of the Champlain Bridge and improvements to several major highway access points, employment is on track to keep rising. In terms of research and development, the fact that the area boasts four universities and two mega hospitals close to completion is another selling point for new business. “These are all positives for our city,” says Sieber. “Montreal is committed to a number of investments in infrastructure which are expected to improve efficiencies and continue to bring the population downtown as these projects progress.” The retail and industrial sectors are expected to remain stable on the back of moderated growth in the Greater Montreal Area (GMA) economy and ongoing employment gains. Leasing activity is looking positive for the industrial sector, but an aging building stock is an ongoing issue. While multi-family construction slowed in 2013, strong international migration has kept CANADIAN MARKET OUTLOOK 2014

- 70. the population growing and the recent condo boom is expected to continue bringing new people, investment and energy to downtown Montreal. Beyond quality product, Sieber says tenants are also looking for solid leasing options. “It’s no longer a price per pound mentality, but whether there are viable long-term leasing options available to them,” he says. A number of negative factors have created some headwinds in the GMA economy generating sub-par growth (corruption allegations, challenged economy worldwide, tax modifications are a few examples). With the Charbonneau Commission well underway, stronger growth expected in the U.S., increased manufacturing and exports, the hope is the market will rebound in 2014 and surprise to the upside. PROJECTS TO WATCH NEW DOWNTOWN TOWER ANNOUNCEMENTS: TOUR AIMIA, DELOITTE TOWER AND L’AVENUE TOWER CHAMPLAIN BRIDGE TWO MEGA HOSPITALS TURCOT INTERCHANGE GRIFFINTOWN MONTREAL PREMIUM OUTLETS 63

- 73. CLICK HERE FOR MARKET STATISTICS HALIFAX MARKE “To move the downtown office sector back into balance is going to take years, it starts with more urban residential density.” Robert Mussett Senior Vice President & Senior Managing Director, Halifax 2014 MARKET OUTLOOK

- 74. ET Tightening vacancy in downtown office space may be the norm in many major Canadian markets, but Halifax is one metropolitan area where the suburban office market continues to hold more appeal than the more established downtown core. In fact, Robert Mussett, Senior Vice President and Senior Managing Director of CBRE for Atlantic Canada, says the suburban office market is significantly outperforming the urban one—and it is expected to stay that way for a while. It is no surprise then that the urban vacancy rate is expected to remain high for the foreseeable future as well. “We are not a head office market so the desire or need to be clustered in the downtown core is not as great as it is for other cities in Canada,” he says.

- 75. Downtown vs. Suburban Class A Rents (Halifax vs. National) 25.68 18.14 17.37 16.68 Downtown Suburban Halifax Downtown Suburban National Source: CBRE Limited The decades long increase in residential suburban development also means having offices in the suburbs is more conducive to employee satisfaction. “Employee recruitment and retention is important to all users, and in many cases staff are saying ‘we can park for free and get there faster’ in the suburbs,” says Mussett. That’s not to say the city isn’t investing in the downtown core. A new multi-sports facility is generating lots of buzz, as are some large multi-residential developments and proposed office towers. “People like downtown and it’s a lively place, but to move the downtown office sector back into balance is going to take years, it starts with more residential density,” he says. On the plus side, employment opportunities in the area and several large-scale projects on the horizon, point to a potentially faster growing urban housing market, which should help spur office sector growth. As the economic hub of Nova Scotia and Atlantic Canada, job creation in Halifax is looking better than in many other parts of the country. With a breadth of institutions and a large public sector that includes one of the largest RCMP facilities in the country, infrastructure investments are ongoing, albeit more slowly due to recent fiscal pressures. Projects such as The Bedford Waterfront Development and government shipping contract are expected to generate thousands of future jobs. With the Deep Panuke offshore natural gas field almost at full production, the Gross Domestic Product (GDP) is forecast to grow from 1.1% in 2013 to 2.9% in 2014. Shell and BP have committed some $2.0 billion to oil exploration and drilling activities starting in 2014, which in turn could result in some demand for office space locally as companies service these projects. As a renter’s market primarily, with relatively high levels of discretionary income, Halifax’s retail sector continues to reap the benefits. Mussett says, by and large, the retailers do well because shoppers don’t have big mortgages and therefore more disposable income to draw from. With retail density (SF per person) exceeding the Canadian CANADIAN MARKET OUTLOOK 2014

- 76. average, he expects the development of large box retail centres is coming to an end and will be replaced with small-box in-fill opportunities. The slowdown of REIT purchasing activity in mid-2013 had a more dramatic effect in Atlantic Canada than in other parts of the country. “In smaller markets like ours, we are very susceptible in that we are the first ones to feel the pullback in investment by the REITs and the last to feel the positive reactions,” says Mussett. “However, we expect REITs will be more active in 2014 as the outlook is for continued rate stability.” PROJECTS TO WATCH TD CENTRE EXPANSION, NOVA CENTRE AND WATERSIDE CENTRE WEST BEDFORD SUBURBAN OFFICE SHELL AND BP OFFSHORE OIL EXPLORATION DARTMOUTH CROSSING DOWNTOWN STREET FRONT RETAIL 69

- 77. CANADIAN MARKET OUTLOOK 2014 MARKET

- 78. CANADIAN MARKET OUTLOOK 2014 STATISTICS

- 79. MARKET COMMENTARY CANADA MARKET STATISTICS OFFICE INDUSTRIAL DOWNTOWN 2012 2013 2014F 6.1% 7.8% 8.4% $25.28 $25.68 $26.73 Absorption (SF in millions) 2.47 (3.20) 2.60 Sale Price (psf) New Supply (SF in millions) 2.43 0.88 4.48 Under Construction (SF in millions) 9.22 14.05 11.12 Class A Net Rental Rate (psf) SUBURBAN 2012 2013 2014F 6.1% 5.8% 5.6% $5.59 $6.00 $6.04 $97.34 $105.82 $108.61 Absorption (SF in millions) 19.16 19.86 16.52 New Supply (SF in millions) 15.38 16.68 13.38 Under Construction (SF in millions) Vacancy Rate YoY 15.24 12.72 10.95 2012 2013F 2014F Availability Rate Net Rental Rate (psf) 2012 2013 2014F 11.4% 12.1% 13.1% $17.68 $17.37 $17.77 Absorption (SF in millions) 1.74 1.53 1.03 TRANSACTIONS New Supply (SF in millions) 3.23 3.31 3.46 Office $9,284 $5,574 $5,513 Under Construction (SF in millions) 8.72 7.40 5.11 Industrial $5,058 $5,856 $5,647 ICI Land $4,350 $3,891 $4,221 Retail $4,931 $5,441 $4,821 $6,023 $4,293 $4,075 YoY Vacancy Rate Class A Net Rental Rate (psf) OVERALL YoY INVESTMENT 2012 2013 2014F 8.4% 9.7% 10.8% Multi-housing $20.80 $21.00 $21.75 Hotel $916 $1,781 $670 Absorption (SF in millions) 4.22 (1.68) 3.63 Total $30,562 $26,836 $24,947 New Supply (SF in millions) 5.65 4.19 7.94 Under Construction (SF in millions) 17.94 21.45 16.24 Vacancy Rate Class A Net Rental Rate (psf) YoY (in $millions) CANADIAN MARKET OUTLOOK 2014 YoY

- 80. MARKET COMMENTARY MARKET STATISTICS VANCOUVER OFFICE INDUSTRIAL DOWNTOWN 2012 2013 2014F 4.2% 6.1% 7.0% $34.66 $33.12 $34.78 (0.16) (0.43) (0.06) 4.50-5.25 4.50-5.25 4.50-5.25 New Supply (SF in millions) 0.01 0.02 0.15 Class A&B Cap Rate (%) Under Construction (SF in millions) 1.46 1.68 1.91 Class A Net Rental Rate (psf) Absorption (SF in millions) Class A Cap Rate (%) SUBURBAN 2012 2013 2014F Vacancy Rate 12.2% 11.5% $19.97 0.47 0.15 5.75-6.25 5.75-6.50 0.43 0.09 2.16 1.40 6.2% $7.60 $7.96 $8.36 $179.00 $192.00 $195.00 3.72 2.43 1.62 5.50-6.25 5.25-6.25 5.25-6.25 New Supply (SF in millions) 2.56 2.31 1.45 1.99 2.28 2.08 2012 2013 2014F 1.8% 2.1% 2.2% 3.50-5.00 3.50-5.00 3.50-5.00 Absorption (SF in millions) 0.80 Under Construction (SF in millions) 6.4% Sale Price (psf) 5.75-6.50 New Supply (SF in millions) 6.6% Net Rental Rate (psf) 0.45 Class A & B Cap Rate (%) 2014F $20.97 Absorption (SF in millions) 2013 Availability Rate 12.4% $20.78 2012 Under Construction (SF in millions) Vacancy Rate YoY YoY 0.60 Class A Net Rental Rate (psf) YoY MULTI-HOUSING Overall Vacancy Rate** Apartment Cap Rate (%) YoY **Canada Mortgage and Housing Corporation INVESTMENT 2012 2013F 2014F $1,015 $482 $408 Industrial $789 $711 $907 0.38 ICI Land $607 $593 $843 0.11 0.95 Retail $793 $1,347 $730 3.08 2.51 Multi-housing $815 $475 $308 Hotel $79 $141 $54 Total OVERALL $4,097 $3,747 $3,249 2012 2013 2014F 8.1% 8.8% 9.8% $22.49 $22.79 $24.13 Absorption (SF in millions) 0.31 (0.28) New Supply (SF in millions) 0.45 Under Construction (SF in millions) 3.62 Vacancy Rate Class A Net Rental Rate (psf) YoY Office RETAIL 2012 Retail Sales (YoY)* Neighbourhood Cap Rate (%) 2013 2014F 0.4% 4.4% 5.50-6.00 (in $millions) YoY 3.7% 5.50-6.00 TRANSACTIONS YoY 5.75-6.25 * Conference Board of Canada 73

- 81. MARKET COMMENTARY CALGARY MARKET STATISTICS OFFICE INDUSTRIAL 2012 2013 2014F 4.9% 7.1% 6.4% $8.05 $8.10 $8.15 $150.00 $175.00 $180.00 3.58 0.28 2.59 5.50-7.00 5.50-6.75 5.50-6.75 New Supply (SF in millions) 3.82 3.09 1.90 Under Construction (SF in millions) DOWNTOWN 3.33 1.55 1.50 2012 2013 2014F 1.3% 0.8% 1.2% 4.50-6.25 3.50-5.25 4.00-5.25 2012 2013 2014F 5.0% 9.1% 9.5% $40.58 $36.76 $37.25 2.06 (1.60) 0.61 5.00-6.25 5.00-6.00 5.50-6.25 New Supply (SF in millions) 1.90 0.00 0.84 Class A&B Cap Rate (%) Under Construction (SF in millions) 1.66 4.67 3.83 Vacancy Rate Class A Net Rental Rate (psf) Absorption (SF in millions) Class A Cap Rate (%) SUBURBAN 2012 2013 2014F Vacancy Rate 10.8% 11.0% $24.51 0.37 0.78 5.75-7.50 5.75-7.00 0.77 0.94 0.34 Under Construction (SF in millions) 1.82 1.63 1.29 2012 2013 2014F 7.0% 9.8% 10.1% $30.38 $30.32 $31.13 Absorption (SF in millions) 2.43 (0.82) 0.89 New Supply (SF in millions) 2.67 0.94 1.18 Under Construction (SF in millions) 3.48 6.30 Absorption (SF in millions) 5.75-7.00 New Supply (SF in millions) Sale Price (psf) 0.27 Class A & B Cap Rate (%) Net Rental Rate (psf) $25.00 Absorption (SF in millions) Availability Rate 11.1% $24.30 YoY 5.12 Class A Net Rental Rate (psf) YoY MULTI-HOUSING Overall Vacancy Rate** Apartment Cap Rate (%) INVESTMENT Class A Net Rental Rate (psf) Neighbourhood Cap Rate (%) 2014F 0.3% Retail Sales (YoY)* 2013 4.2% 5.50-6.25 2014F $1,973 $1,148 $750 $626 $674 $750 ICI Land $661 $368 $450 Retail $733 $129 $225 Multi-housing $486 $227 $300 $108 $293 $150 $4,587 $2,839 $2,625 4.8% 5.50-6.50 TRANSACTIONS Office RETAIL 2012 2013F Industrial YoY 2012 Total Vacancy Rate YoY **Canada Mortgage and Housing Corporation Hotel OVERALL YoY YoY 5.75-6.25 * Conference Board of Canada CANADIAN MARKET OUTLOOK 2014 (in $millions) YoY

- 82. MARKET COMMENTARY EDMONTON MARKET STATISTICS OFFICE INDUSTRIAL DOWNTOWN 2012 2013 2014F 8.3% 9.7% 10.4% $24.54 $24.28 $24.50 0.25 (0.21) 0.13 5.50-7.00 5.25-7.25 5.25-7.25 New Supply (SF in millions) 0.00 0.00 0.25 Class A&B Cap Rate (%) Under Construction (SF in millions) 0.25 0.25 0.60 Class A Net Rental Rate (psf) Absorption (SF in millions) Class A Cap Rate (%) SUBURBAN 2012 2013 2014F Vacancy Rate 11.5% 11.8% $19.91 $21.27 0.39 0.33 6.25-7.25 6.25-7.25 0.26 0.43 1.07 0.28 3.2% $9.88 $10.79 $10.85 $133.33 $144.21 $145.00 2.39 4.33 3.68 5.50-7.25 5.50-7.00 5.50-7.00 New Supply (SF in millions) 3.35 4.48 2.28 1.66 2.28 1.67 2012 2013 2014F 1.7% 1.0% 1.3% 4.00-6.25 4.50-6.25 4.50-6.25 Absorption (SF in millions) 0.44 Under Construction (SF in millions) 4.7% Sale Price (psf) 6.25-7.25 New Supply (SF in millions) 4.7% Net Rental Rate (psf) 0.25 Class A & B Cap Rate (%) 2014F $21.00 Absorption (SF in millions) 2013 Availability Rate 12.9% Class A Net Rental Rate (psf) 2012 Under Construction (SF in millions) Vacancy Rate YoY YoY YoY 0.56 MULTI-HOUSING Overall Vacancy Rate** Apartment Cap Rate (%) YoY **Canada Mortgage and Housing Corporation INVESTMENT 2012 2013F 2014F Office $380 $385 $250 $23.61 Industrial $324 $398 $330 0.12 0.38 ICI Land $761 $1,463 $1,000 0.26 0.43 0.69 Retail $570 $310 $250 1.32 0.53 1.16 Multi-housing $122 $348 $300 Hotel $159 $155 $50 Total OVERALL $2,315 $3,060 $2,180 2012 2013 2014F 9.5% 10.5% 11.4% $23.72 $23.67 Absorption (SF in millions) 0.63 New Supply (SF in millions) Under Construction (SF in millions) Vacancy Rate Class A Net Rental Rate (psf) YoY RETAIL 2012 Retail Sales (YoY)* Neighbourhood Cap Rate (%) 2013 2014F 1.2% 4.8% 5.75-6.25 (in $millions) YoY 4.5% 5.75-6.50 TRANSACTIONS YoY 5.75-6.25 * Conference Board of Canada 75