South Indian Bank

At the CMP of Rs 33, the stock is trading at an Adj P/BV of 1.3x and 1.1x for FY15E and FY16E, respectively. With the new government stepping-up reforms and making efforts to remove the bottlenecks in the economy, we expect the economic growth to pick up going forward. Consequently, we expect the strong growth momentum seen in SIB over past few years to continue. We expect advances and deposits to grow at a CAGR of ~19% each over the forecasted period of FY14-16E. With business further expected to grow at CAGR of 19.5% over FY14-16E; NIMs remaining stable at ~3.0% and cost-to-income ratio improving to ~45% (currently ~50%), we expect a robust PAT growth of 22.6% CAGR over FY14-16E to Rs 763 crore. Asset quality of SIB has improved in FY14 with GNPA and Net NPA standing at 1.2% and 0.8% in FY14 against 1.4% and 0.8% in FY13, respectively (which compares favourably with peers). On the capital adequacy front, SIB is comfortably placed to support the future business needs of the bank over the period FY14-16E. The management has stated that it does not require any Tier-I capital funding during the current year. However, it plans to raise Tier-II capital of Rs 200 crore in FY15 to fund future growth.

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Andere mochten auch

Andere mochten auch (13)

Ähnlich wie South Indian Bank

Ähnlich wie South Indian Bank (20)

Mehr von Vinit Bolinjkar LION bolinjkar.vinit@gmail.com

Mehr von Vinit Bolinjkar LION bolinjkar.vinit@gmail.com (20)

South Indian Bank

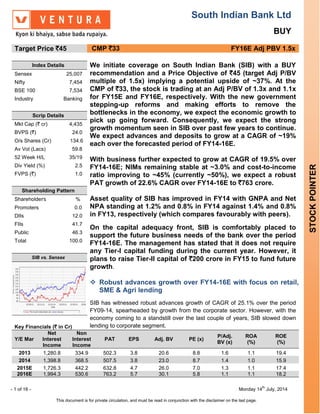

- 1. South Indian Bank Ltd BUY - 1 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. STOCKPOINTER Target Price `45 CMP `33 FY16E Adj PBV 1.5x Index Details We initiate coverage on South Indian Bank (SIB) with a BUY recommendation and a Price Objective of `45 (target Adj P/BV multiple of 1.5x) implying a potential upside of ~37%. At the CMP of `33, the stock is trading at an Adj P/BV of 1.3x and 1.1x for FY15E and FY16E, respectively. With the new government stepping-up reforms and making efforts to remove the bottlenecks in the economy, we expect the economic growth to pick up going forward. Consequently, we expect the strong growth momentum seen in SIB over past few years to continue. We expect advances and deposits to grow at a CAGR of ~19% each over the forecasted period of FY14-16E. With business further expected to grow at CAGR of 19.5% over FY14-16E; NIMs remaining stable at ~3.0% and cost-to-income ratio improving to ~45% (currently ~50%), we expect a robust PAT growth of 22.6% CAGR over FY14-16E to `763 crore. Asset quality of SIB has improved in FY14 with GNPA and Net NPA standing at 1.2% and 0.8% in FY14 against 1.4% and 0.8% in FY13, respectively (which compares favourably with peers). On the capital adequacy front, SIB is comfortably placed to support the future business needs of the bank over the period FY14-16E. The management has stated that it does not require any Tier-I capital funding during the current year. However, it plans to raise Tier-II capital of `200 crore in FY15 to fund future growth. Robust advances growth over FY14-16E with focus on retail, SME & Agri lending SIB has witnessed robust advances growth of CAGR of 25.1% over the period FY09-14, spearheaded by growth from the corporate sector. However, with the economy coming to a standstill over the last couple of years, SIB slowed down lending to corporate segment. Sensex 25,007 Nifty 7,454 BSE 100 7,534 Industry Banking Scrip Details Mkt Cap (` cr) 4,435 BVPS (`) 24.0 O/s Shares (Cr) 134.6 Av Vol (Lacs) 59.8 52 Week H/L 35/19 Div Yield (%) 2.5 FVPS (`) 1.0 Shareholding Pattern Shareholders % Promoters 0.0 DIIs 12.0 FIIs 41.7 Public 46.3 Total 100.0 SIB vs. Sensex Key Financials (` in Cr) Y/E Mar Net Interest Income Non Interest Income PAT EPS Adj. BV PE (x) P/Adj. BV (x) ROA (%) ROE (%) 2013 1,280.8 334.9 502.3 3.8 20.6 8.8 1.6 1.1 19.4 2014 1,398.8 368.5 507.5 3.8 23.0 8.7 1.4 1.0 15.9 2015E 1,726.3 442.2 632.8 4.7 26.0 7.0 1.3 1.1 17.4 2016E 1,994.3 530.6 763.2 5.7 30.1 5.8 1.1 1.1 18.2

- 2. - 2 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. To mitigate this loss of business from corporate loans, SIB has been concentrating on the Retail / SME & Agri lending. The management is aiming for 60% contribution of the total loan portfolio from this segment by FY16 as compared to 50% at end of FY14. To cater to this new growth thrust, SIB has set up a separate profit center to concentrate on housing, auto and retail loans which are the pivotal sub segments. We expect overall advances to grow at a CAGR of 19.5% to `51,736 crore by FY16E. Robust deposit growth to continue; CASA to witness significant traction Over FY09-14, deposits have grown at a CAGR of 21.3% and we expect this brisk pace of growth to be maintained over the forecast period. With SIB planning to add 50 new branches every year and taking initiatives like priority banking (80 centres) and NRE banking (NRE/NRO) CASA deposits are expected to grow at a faster clip of 31.4% which should help boost CASA ratio to 25% (from the current 20.7%) by FY16. This in turn should help bring down cost of deposits. Overall we expect total deposits to grow at a CAGR of 19.5% to `67,817 crore by FY16E. Stable asset quality is an added comfort In this adverse economic scenario, where most of the banks are suffering from asset quality issues, SIB with 1.2% GNPA and 0.8% NNPA in FY14 is better placed than most peers in terms of the asset quality. With a slew of measures being undertaken to improve asset quality and the overall economic environment also expected to improve, we do not expect any further aggravation in the asset quality Valuation We initiate coverage on South Indian Bank with a BUY recommendation and a Price Objective of `45 (target Adj P/BV multiple of 1.5x) implying a potential upside of ~37%. At the CMP of `33, the stock is trading at an Adj P/BV of 1.3x and 1.1x for FY15E and FY16E, respectively.

- 3. - 3 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. Company Background Incorporated in 1929, South Indian Bank (SIB) is a leading mid-sized bank in the private sector space. It operates a network of ~800 branches and ~1000 ATMs. With about half of its branches located in Kerala, SIB’s business is largely skewed towards the Southern state. The bank is looking to maintain a geographic spread (1:1 Kerala: outside Kerala) and expand its pan-India foot-print. The total business done has scaled to `83,721 in FY14 at a CAGR of 29.3% over a five year period, spearheaded by the strong brand recall it enjoys among the Keralite NRI diaspora. SIB is among the better capitalized banks in the industry with a total CAR of 12.5%. Gross NPAs were reported at 1.2% with provision coverage ratio of 62.7%. South Indian Bank – Loan Portfolio Source: SIB, Ventura Research (Rs 36,230 cr in FY14)

- 4. - 4 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. Key Investment Highlights Robust advances growth over FY14-16E with focus on retail and SME & Agri lending SIB has witnessed robust advances growth with a CAGR of 25.1% over the period FY09-14 spearheaded by corporate sector lending. However, with the economy coming to a standstill over the last couple of years, SIB slowed down lending to the corporate segment. To mitigate this loss of business from corporate loans, SIB has been concentrating on the Retail / SME & Agri lending. The management is aiming for 60% contribution of the total loan portfolio from this segment by FY16 as compared to 50% at end of FY14. To cater to this new growth thrust SIB has set up a separate profit center to concentrate on housing, auto and retail loans which are the pivotal sub segments We expect overall advances to grow at a CAGR of 19.5% to `51,736 crore by FY16E. Robust deposit growth to continue; CASA to witness significant traction Over FY09-14, deposits have grown at a CAGR of 21.3% with term deposits growing at a CAGR of 22.3% while demand deposits and savings deposits have clocked a growth of 17.4% and 18.1% respectively. SIB is taking initiatives like priority banking (80 centres) and NRE banking (NRE/NRO savings bank deposits constitute 20% of the total CASA of SIB) to improve the CASA ratio currently at 20.7%. This is expected to spearhead faster CASA growth (of 31.4%) over FY14-16E, while the CASA ratio to improve to 25% Advances to grow at CAGR of 19.5% Advances Break-up Trend 0% 5% 10% 15% 20% 25% 30% 35% 0 10000 20000 30000 40000 50000 60000 FY11 FY12 FY13 FY14 FY15E FY16E Rs Crore Advances Growth (RHS) 0 10000 20000 30000 40000 50000 60000 FY11 FY12 FY13 FY14 FY15E FY16E Rs.Crore Corporate Retail and SME & Agri Source: SIB, Ventura Research Source: SIB, Ventura Research

- 5. - 5 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. (from the current 20.7%) by FY16. This should help bring down cost of deposits. SIB is expected to add 50 branches and more than 100 ATMs every year over the next couple of years. As can be seen in the chart, SIB has further scope of improvement in CASA as compared to similar sized banks. We expect total deposits to grow at a CAGR of 19.5% to `67,817 crore by FY16E. Growing contribution from CASA accounts Scope for improvement in CASA as compared to peers 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 0 10000 20000 30000 40000 50000 60000 70000 80000 FY11 FY12 FY13 FY14 FY15E FY16E Rs.Crore Term Deposit CA SB CASA Ratio (RHS) 15 30.81 33.4 25.4 20.6 20.7 0 5 10 15 20 25 30 35 40 CUB Federal ING Vysya Karnataka Karur Vysya SIB (%) Source: SIB, Ventura Research Source: SIB, Ventura Research Deposits to grow at CAGR of 19.5% Branch Expansion ahead 0% 5% 10% 15% 20% 25% 30% 35% 0 10000 20000 30000 40000 50000 60000 70000 80000 FY11 FY12 FY13 FY14 FY15E FY16E Rs Crore Deposits Growth (RHS) 641 700 750 800 850 900 0 100 200 300 400 500 600 700 800 900 1000 FY11 FY12 FY13 FY14 FY15E FY16E Nos. Source: SIB, Ventura Research Source: SIB, Ventura Research

- 6. - 6 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. Profitability to improve on the back of high NII growth, stable NIMs and improvement in cost to income ratio SIB has registered a robust profit growth of 20.2% CAGR over the period FY11-14 on the back of robust business growth seen over the same period (CAGR of 18.6%). With business further expected to grow at CAGR of 19.5% over FY14-16E and NIMs remaining stable at ~3.0% and cost-to-income ratio improving to ~45%, we expect a robust PAT growth at 22.6% CAGR over FY14-16E. Return ratios ROE and ROA are also expected to improve to 18.2% and 1.1%, respectively. NII to clock a CAGR of 19.4% over FY14-16E Robust advances growth and deposit growth has helped SIB register NII growth of 20.9% over FY11-14. With robust growth in advances expected to continue and contribution from retail rising, we expect NII growth to sustain at a CAGR of 19.4% to `1,989 crore over FY14-16E. Stable NIMs and lower cost to income to boost profitability Despite sluggish economic growth, SIB has managed to maintain NIMs at ~3.0%. Going forward, we expect the NIMs to remain stable above 3.0% with renewed focus on the growth of higher yielding retail business and thrust on mobilization of low cost CASA deposits. The cost-to-income ratio for SIB had deteriorated from 47.5% in FY13 to 50.0% in FY14 due to higher provision for wages according to IBA guidelines (most of which has already been accounted for). Also, out of 50 new branches to be added this year, 25 branches will be full-fledged branches and remaining will be extension NII Quarterly Trend NII to grow at a CAGR of 19.2% 0 50 100 150 200 250 300 350 400 Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 Rs.Crore 0 500 1000 1500 2000 2500 FY11 FY12 FY13 FY14 FY15E FY16E Rs.Crore Source: SIB, Ventura Research Source: SIB, Ventura Research

- 7. - 7 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. counters which have lower operating costs. According to RBI guidelines, 25% of the new branches have to be opened in the rural and un-banked areas, which will have lower operating costs. This is expected to improve the C/I ratio by 515 bps to 44.8% by FY16 With stable NIMs and lower cost-to-income ratio going forward, we expect profitability to improve to Rs 763 crore. As a result ROE is expected to improve from 15.9% in FY14 to 17.0% in FY16. NIM and Cost to Income-Quarterly Trend NIM and Cost to Income Annual Trend 3.0% 3.1% 3.1% 3.1% 3.1% 3.1% 3.2% 3.2% 3.2% 3.2% 0% 10% 20% 30% 40% 50% 60% Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 (%) Cost to Income NIM (RHS) 2.8% 2.9% 2.9% 3.0% 3.0% 3.1% 3.1% 3.2% 3.2% 42% 43% 44% 45% 46% 47% 48% 49% 50% 51% FY11 FY12 FY13 FY14 FY15E FY16E (%) Cost to Income NIM (RHS) Source: SIB, Ventura Research Source: SIB, Ventura Research Yield on Adv and Cost of Dep Quarterly Trend Yield on Adv and Cost of Dep Annual Trend 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% Q4FY12 Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 Yield on Advances Cost of Deposits 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% FY11 FY12 FY13 FY14 FY15E FY16E Yield on Avg Advances Cost of Avg Deposits Source: SIB, Ventura Research Source: SIB, Ventura Research

- 8. - 8 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. Other income to reduce earnings volatility SIB’s other income has grown at a CAGR of 17.5% over FY09-14. Going forward, we expect the same to grow at a 20% CAGR over next two years driven by the income from the card business and insurance commission business. SIB acts as a corporate agent for the distribution of insurance products of both LIC and Bajaj Alliance for life insurance and general insurance respectively. Further SIB has a tie-up with 13 leading Mutual Funds, and has also enrolled as a NIM Cost to Income compares favorably with peers Source: SIB, Ventura Research 47.8 47.7 64.0 54.2 57.6 55.6 3.3 3.6 3.7 2.4 2.7 3.0 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0 CUB Federal ING Vysya Karnataka Karur Vysya SIB (%) Cost to Income NIM (RHS) Quarterly 45.2 49.3 57.0 56.1 54.7 50.0 3.5 3.3 3.5 2.4 2.6 3.0 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 0.0 10.0 20.0 30.0 40.0 50.0 60.0 CUB Federal ING Vysya Karnataka Karur Vysya SIB (%) Cost to Income NIM (RHS) Annually Yield on Advances and Cost of Deposit comparison with peers Source: SIB, Ventura Research 13.1 11.6 11.7 12.1 12.0 12.4 7.2 7.9 7.2 7.6 8.1 8.1 0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 CUB Federal ING Vysya Karnataka Karur Vysya SIB (%) Yield on Advances Cost of Deposit Quarterly 13.4 11.4 11.6 12.2 12.3 12.4 7.4 8.6 7.3 7.9 8.2 8.1 0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0 CUB Federal ING Vysya Karnataka Karur Vysya SIB (%) Yield on Advances Cost of Deposit Annually

- 9. - 9 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. Channel Partner for the distribution of bonds issued by different companies. With an array of avenues to generate fee income, we expect it to grow at a CAGR of 20% to `531 crore by FY16E. Stable asset quality is an added comfort In this adverse economic scenario, where most of the banks are suffering from asset quality issues, SIB with 1.2% GNPA and 0.8% NNPA in FY14 is better placed than most peers in terms of asset quality. The provision coverage ratio improved from 53% in FY13 to 63% in FY14 and provides additional comfort. It is further expected to improve to 67% in FY15. GNPA of SIB has improved from 1.3% in FY13 to 1.2%, which under a worst case scenario can increase to 1.3% in FY15. Net NPA has remained stable at 0.8% over the past two years and can increase to 0.9% in FY15 in a worst case scenario. The bank is taking prudent measures like reducing aggregator funding in the case of the gold loans and approving gold loans for real end use (individual requirements and small ticket size loans). Such measures will help it to keep the NPA in check in future. The bank has also gone slow on infrastructure lending with infrastructure constituting 14.3% of its total loan portfolio in FY14 as compared to 15.0% in FY13. SIB has recovered NPAs to the extent of `533 crore in FY14, (recovery including upgradation of `301 crore), surpassing its target of `250 crore. The recovery during FY14 also surpassed the recovery of `270 crore for FY13. The sustained thrust on selection of credit, adequate due diligence and improvement in credit administration ensured improvement in quality of assets. SIB has also constituted a committee which meets once every quarter to review all Other Income Quarterly Trend Other Income to grow at a CAGR of 20% 0 20 40 60 80 100 120 140 Q4FY12 Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 Rs. Crore 0 100 200 300 400 500 600 FY11 FY12 FY13 FY14 FY15E FY16E Rs.Crore Source: SIB, Ventura Research Source: SIB, Ventura Research

- 10. - 10 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. NPA Accounts above `50 lakh. Restructured assets of the bank currently stands at `1725 crore which can further deteriorate to `1900 crore in the worst case scenario. Comfortably placed to raise Tier-II capital for future growth With capital adequacy of 12.5% (Tier-I capital stood at 10.9%, while Tier-II capital stood at 1.6% in FY14), SIB is comfortably placed to support the future business needs during FY14-16E. The management has stated that it does not require any Tier-I capital funding during the current year. However, it plans to raise Tier-II capital of `200 crore in FY15 to fund future growth (The management has expressed confidence that it can easily raise Tier-II capital upto `800 crore). Asset Quality remaining Stable in challenging environment Source: SIB, Ventura Research 0% 10% 20% 30% 40% 50% 60% 70% 80% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5% Q4FY12 Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 (%) Gross NPA Net NPA PCR (RHS) 40% 45% 50% 55% 60% 65% 70% 75% 80% 0.0% 0.2% 0.4% 0.6% 0.8% 1.0% 1.2% 1.4% 1.6% FY11 FY12 FY13 FY14 FY15E FY16E (%) Gross NPA Net NPA PCR Asset quality comparison with peers Source: SIB, Ventura Research, RA: Restructured Assets 1.8 2.5 1.8 2.9 0.8 1.21.2 0.7 0.3 1.9 0.4 0.8 0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 CUB Federal ING Vysya Karnataka Karur Vysya SIB (%) Gross NPA Net NPA Annually 1.7% 5.5% 1.4% 5.6% 3.6% 4.8% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% CUB Federal ING Vysya Karnataka Karur SIB CUB Federal ING Vysya Karnataka Karur SIB

- 11. - 11 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. For the current year, the bank is focusing on the retail segment, where risk weights are low as compared to the corporate book and current capital will be sufficient to fund the growth. The management expects Tier-I capital to be around 9.5% to 10%, by the end of FY15. Return Ratios SIB has been successful in maintaining healthy return ratios over the years given its strong track record. With the buoyant economic growth expected, we expect ROE to improve to 18.1% in FY16 as compared to 15.9% in FY14. Tier-II capital infusion will be required for B/S growth Source: SIB, Ventura Research 10.9% 12.3% 11.8% 12.1% 11.9% 11.4% 10.7% 10.9% 2.3% 2.1% 2.1% 1.9% 1.8% 1.8% 1.7% 1.6% 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% Q1FY13 Q2FY13 Q3FY13 Q4FY13 Q1FY14 Q2FY14 Q3FY14 Q4FY14 (%) Tier I Tier II 11.3% 11.5% 12.0% 10.9% 10.6% 10.1% 2.7% 2.5% 1.9% 1.6% 1.5% 1.7% 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% FY11 FY12 FY13 FY14 FY15E FY16E (%) Tier I Tier II Capital Adequacy as compared to peers Source: SIB, Ventura Research 14.5 14.6 14.6 10.8 11.6 10.9 0.6 0.6 2.1 2.5 1.2 1.6 0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0 CUB Federal ING Vysya Karnataka Karur Vysya SIB (%) Tier I Tier II Quarterly 14.5 14.6 14.6 10.8 11.6 10.9 0.6 0.6 2.1 2.5 1.2 1.6 0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0 18.0 CUB Federal ING Vysya Karnataka Karur Vysya SIB (%) Tier I Tier II Annually

- 12. - 12 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. Key Risks and Concerns SIB has traditionally had major presence in southern India especially Kerala which houses almost 55% of its branches. However, going forward, as a strategy, SIB has set a target of having 50% branches outside Kerala. In FY15, SIB plans to open branches in Maharashtra, Gujarat and North-East India. SIB has high exposure to gold loans which it is trying to bring down especially when it comes to gold aggregator lending. The exposure to total gold loans has come down to 14.3% in FY14 from 20.2% in FY13. Financial Performance In Q4FY14, SIB’s advances grew at 13.9% YoY (8.7%QoQ) to `36,230 crore amidst contraction in retail advances (10.5% YoY, 0.3%QoQ). However, SME & Agri (38.6%YoY, 12.7%QoQ) and Corporate (16.2%YoY, 10.9%QoQ) supported loan growth. Consequently, the share of retail advances declined (600 bps YoY, 200 bps QoQ) to 22%, while the share of SME & Agri improved (500 bps YoY, 100 bps QoQ) to 28%. Decline in retail advances was led by de-growth in gold loans (29.4%YoY) and Vehicle loans (3%YoY), while housing loans continued to strengthen (24.2%YoY). Over the same period, deposits growth remained lacklustre at 7.3%YoY, (6.4%QoQ) at `47,490 crore amidst slower growth in CASA deposits (3.8% QoQ) at `9,830 crore. Consequently, the share of CASA deposits declined 50 bps QoQ at 20.7%, while the share of NRI deposits stood at ~25%. NIM remained stable at 3.0% in the Q4FY14 owing to improvement in yield on advances (1 bps QoQ) and stable cost of funds. The management expects NIMs to remain stable at ~3% levels in FY15. ROE and ROA Annual Trend ROA/ROE comparison with peers 0.9% 1.0% 1.0% 1.1% 1.1% 1.2% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0% 20.0% 22.0% FY11 FY12 FY13 FY14 FY15E FY16E ROE ROA (RHS) CUB Federal ING Vysya Karnataka Karur Vysya SIB 0.6 0.8 1 1.2 1.4 1.6 10 12 14 16 18 20 ROA(%) ROE (%) Source: SIB, Ventura Research Source: SIB, Ventura Research

- 13. - 13 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. Asset Quality improved as absolute GNPA’s decreased (7.7% YoY, 29.4% QoQ) to `434 crore (1.2% of advances), whilst NNPA’s declined by 27.5% QoQ to `290 crore (0.8% of advances). Cost to Income increased 199 bps QoQ to 49.9% led by higher wage cost. Hence, net profit declined (19% YoY, 11.8% QoQ) to `124 crore. Financial Outlook We expect NII to grow at a CAGR of ~21% over FY14-16E to `1,989 crore with NIM improving to 3.1% (v/s 3.0% in FY14). PAT is expected to grow at ~22% CAGR over FY14-16E to `759 crore. On the balance sheet front, advances are expected to grow at a CAGR of ~19% to `51,736 crore by FY16E, while deposits are likely to grow at a CAGR of ~19% to `67,817 crore over the same period. Quarterly Financial Performance (` in crore) Particulars Q4FY14 Q4FY13 FY14 FY13 NII (Net Interest Income) 364.7 333.7 1398.8 1280.8 Non ‐ interest income 96.6 121 368.5 334.9 Total income 461.3 454.7 1767.2 1615.8 Total Operating expenses 256.3 248.6 882.9 767.2 Pre provision opt profit 205.0 206.1 884.3 848.6 Provisions 28.3 65.9 155.4 192.7 Profit before tax 176.7 140.2 728.9 655.9 Tax 52.0 -13.6 221.4 153.6 PAT 124.7 153.8 507.5 502.3 Business parameters Deposits (Cr) 47,500 44,300 47,500 44,300 Advances (Cr) 36,200 31,800 36,200 31,800 CD (%) 76.2% 71.8% 76.2% 71.8% CASA Deposits (Cr) 9,800 8,200 9,800 8,200 CASA (%) 20.6 18.5 20.6 18.5 P&L Ratio (%) NIM (%) 3.0 3.2 3.0 3.2 Cost/Income ratio (%) 55.6 54.7 55.6 54.7 RoA (%) 1.0 1.2 1.0 1.1 RoE (%) 16.2 19.2 15.9 19.4 Asset quality GNPL (%) 1.2 1.4 1.2 1.4 NNPL (%) 0.8 0.8 0.8 0.8 Capital Adequacy (%) CAR 12.5 13.9 12.5 13.9 Tier I 10.9 12.1 10.9 12.1 Tier II 1.6 1.8 1.6 1.8 Source: Axis, Ventura Research

- 14. - 14 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. Valuation We initiate coverage on South Indian Bank with a BUY recommendation and a Price Objective of `45 (target Adj P/BV multiple of 1.5x) implying a potential upside of ~37%. At the CMP of `33, the stock is trading at an Adj P/BV of 1.3x and 1.1x for FY15E and FY16E, respectively. Revenue & Profitability 0% 5% 10% 15% 20% 25% 30% 35% 40% 0 200 400 600 800 1000 1200 1400 1600 1800 2000 FY11 FY12 FY13 FY14 FY15E FY16E Rs Crore NII PAT NII growth (RHS) PAT growth (RHS) Source: SIB, Ventura Research 2 Yr EPS CAGR vs Adj P/BV CUB Federal ING Vysya Karnataka Karur Vysya SIB 0.5 0.8 1.1 1.4 1.7 12.0 17.0 22.0 27.0 32.0 37.0 42.0 2YrAdj.P/BV (2 Yr EPS CAGR %) Source: SIB, Ventura Research

- 15. - 15 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. 1 Year forward P/E chart 0 10 20 30 40 50 60 Mar-07 Jul-07 Nov-07 Mar-08 Jul-08 Nov-08 Mar-09 Jul-09 Nov-09 Mar-10 Jul-10 Nov-10 Mar-11 Jul-11 Nov-11 Mar-12 Jul-12 Nov-12 Mar-13 Jul-13 Nov-13 Mar-14 SIB 3x 5x 7x 9x 11x Source: SIB, Ventura Research 1 Year forward P/Adj BV chart 0 5 10 15 20 25 30 35 40 45 Mar-07 Jul-07 Nov-07 Mar-08 Jul-08 Nov-08 Mar-09 Jul-09 Nov-09 Mar-10 Jul-10 Nov-10 Mar-11 Jul-11 Nov-11 Mar-12 Jul-12 Nov-12 Mar-13 Jul-13 Nov-13 Mar-14 SIB 0.5x 0.75x 1x 1.25x 1.5x Source: SIB, Ventura Research

- 16. - 16 of 16 - Monday 14 th July, 2014 This document is for private circulation, and must be read in conjunction with the disclaimer on the last page. Financials and Projections Y/E March, Fig in Rs. Cr FY 2013 FY 2014 FY 2015e FY 2016e Y/E March, Fig in Rs. Cr FY 2013 FY 2014 FY 2015e FY 2016e Profit & Loss Statement Ratio Analysis Interest Income 4,434.3 5,015.1 5,770.8 6,760.8 Efficiency Ratios (%) Interest Expense 3,153.5 3,616.3 4,044.5 4,766.5 Int Exp / Int Earned 71.1% 72.1% 70.1% 70.5% Net Interest Income 1,280.8 1,398.8 1,726.3 1,994.3 Int Income / Tot Funds 8.9% 9.1% 8.9% 8.7% YoY change (%) 25.4% 9.2% 23.4% 15.5% NII/ Total Income (%) 26.9% 26.0% 27.8% 27.4% Non Interest Income 334.9 368.5 442.2 530.6 Other Income / Tot Income 7.0% 6.8% 7.1% 7.3% Total Net Income 1,615.8 1,767.2 2,168.4 2,524.9 Op Exp / Tot Income 16.1% 16.4% 16.3% 15.5% Total Operating Expenses 767.2 882.9 1,011.5 1,131.5 Net Profit / Tot funds 1.0% 0.9% 1.0% 1.0% Pre Provision profit 848.6 884.3 1,156.9 1,393.4 Credit-Deposit 71.9% 76.3% 76.3% 76.3% YoY change (%) 30.2% 4.2% 30.8% 20.4% Investment / Deposit 28.3% 30.2% 28.5% 28.6% Provisions and contingencies 192.7 155.4 198.4 237.1 NIM 3.2% 2.9% 3.1% 3.1% Profit Befor Tax 655.9 728.9 958.6 1,156.2 Cost to Income 47.5% 50.0% 46.6% 44.8% YoY change (%) 14.6% 11.1% 31.5% 20.6% Taxes 153.6 221.4 325.8 393.0 Solvency Net profit 502.3 507.5 632.8 763.2 Gross NPA (Rs. Cr) 433.9 432.6 565.4 672.4 YoY change (%) 25.1% 1.0% 24.7% 20.6% Net NPA (Rs. Cr) 249.5 281.7 391.0 461.7 Gross NPA (%) 1.4% 1.2% 1.3% 1.3% Balance Sheet Net NPA (%) 0.8% 0.8% 0.9% 0.9% Cash & Balances with RBI 1,696.7 2,200.8 2,681.3 3,229.4 Capital Adequacy Ratio (%) 13.9% 12.5% 12.1% 11.8% Inter bank balance 2,639.2 1,017.1 1,638.6 1,973.5 Tier I Capital (%) 12.0% 10.9% 10.6% 10.1% Investments 12,523.5 14,351.8 16,088.0 19,376.3 Tier II Capital (%) 1.9% 1.6% 1.5% 1.7% Advances 31,815.5 36,229.9 43,113.5 51,736.2 Other Assets 1,120.1 1,186.4 1,413.7 1,619.4 Per Share Data (Rs.) Total Assets 49,795.0 54,986.0 64,935.1 77,934.8 EPS 3.8 3.8 4.7 5.7 Deposits 44,262.3 47,491.1 56,514.4 67,817.3 Dividend Per Share 0.7 0.8 0.9 1.0 Demand Deposit 1,547.4 1,888.3 2,825.7 3,390.9 Adjst. Book Value 20.6 23.0 26.0 30.1 Savings Deposit 6,685.5 7,936.6 10,172.6 13,563.5 Term Deposit 36,029.5 37,666.2 43,516.1 50,863.0 Borrowings 1,284.6 2,730.8 3,070.7 3,946.6 Valuation ratios Other Liabilties 1,242.0 1,393.7 1,467.9 1,659.9 Price/Earnings(x) 8.8 8.7 7.0 5.8 Equity 136.5 136.7 136.7 136.7 Price/ Adjst. Book Value(x) 1.6 1.4 1.3 1.1 Reserves 2,869.8 3,233.7 3,745.5 4,374.3 Total Liabilities 49,795.0 54,986.0 64,935.1 77,934.8 Return Ratios Dupont Analysis RoA(%) 1.1% 1.0% 1.1% 1.1% % of Avg Assets RoE(%) 19.4% 15.9% 17.4% 18.2% Net Interest Income 2.8% 2.7% 2.9% 2.8% Non Interest Income 0.7% 0.7% 0.7% 0.7% Growth Ratios (%) Net Income 3.6% 3.4% 3.6% 3.5% Interest Income 23.7% 13.1% 15.1% 17.2% Operating Expenses 1.7% 1.7% 1.7% 1.6% Interest Expenses 23.1% 14.7% 11.8% 17.9% Operating Profit 1.9% 1.7% 1.9% 2.0% Other Income 35.6% 10.0% 20.0% 20.0% Provisions & Contingencies 0.4% 0.3% 0.3% 0.3% Total Income 24.5% 12.9% 15.4% 17.4% Taxes 0.3% 0.4% 0.5% 0.6% Net profit 25.1% 1.0% 24.7% 20.6% RoAA(%) 1.1% 1.0% 1.1% 1.1% Deposits 21.3% 7.3% 19.0% 20.0% Avg assets/Avg equity(x) 356.7 383.6 438.6 522.6 Advances 16.6% 13.9% 19.0% 20.0% Ventura Securities Limited Corporate Office: C-112/116, Bldg No. 1, Kailash Industrial Complex, Park Site, Vikhroli (W), Mumbai – 400079 This report is neither an offer nor a solicitation to purchase or sell securities. The information and views expressed herein are believed to be reliable, but no responsibility (or liability) is accepted for errors of fact or opinion. Writers and contributors may be trading in or have positions in the securities mentioned in their articles. Neither Ventura Securities Limited nor any of the contributors accepts any liability arising out of the above information/articles. Reproduction in whole or in part without written permission is prohibited. This report is for private circulation.