FirstPartner UK Mobile Advertising Market Map 2013 evaluation

A PDF of the map can be downloaded from: http://firstpartner.net/downloads and the on-line version can be explored at: http://firstpartner.net/content/research-showcase-0 This updated Market Map provides an essential visual overview of how it all fits together, who the key players are and which important trends are impacting the sector. FirstPartner’s ever popular Mobile Advertising Market Map has been completely redrawn to reflect current developments in Mobile Real Time Advertising, data driven targeting and the fast cementing relationship between mobile advertising, payments and commerce - and it’s now available in an on-line interactive format. The mobile advertising landscape is becoming significantly more complex as specialist networks, exchanges, DSPs, SSPs and mediators handle increasing amounts of inventory and on-line players expand their operations into mobile. Mobile video and messaging have seen significant growth during 2012 and are becoming recognised by brands as important formats and the launch of Weve, the UK Mobile Network Operator backed JV, is a notable step in the development of ad targeting and, ultimately, the integration of mobile advertising and commerce. This updated Market Map provides an essential visual overview of how it all fits together, who the key players are and which important trends are impacting the sector.

Empfohlen

Weitere ähnliche Inhalte

Andere mochten auch

Andere mochten auch (6)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

FirstPartner UK Mobile Advertising Market Map 2013 evaluation

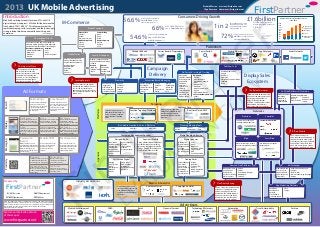

- 1. 2013 UK Mobile Advertising FirstPartner r Richard Warren rwarren@firstpartner.net Olga Kosareva okosareva@firstpartner.net www.firstpartner.net +44 (0)870 874 8700 Introduction Consumers Driving Growth Mobile Advertising accounts for around 7% of of UK M-Commerce 56.6% Of UK Consumers used a Smartphone in the 3 months to May 2012 (1) £1.6billion FirstPartner forecast UK UK Mobile Advertising Revenue Forecast 2012-2016 e digital ad spend, and grew 132% like for like between the Smartphone owners have 1 in 2 1,600 followed up an advert or Mobile Advertising revenue for first halves of 2011 & 2012*. This Map summarises the Of UK 16 to 24 year olds 1,400 rapidly developing sector ecosystem and the increasingly strong relationship between mobile advertising and Mobile Payments 66% own a Smartphone (2) recommendation on their mobile phone (3) 2016 (4) 1,200 1,000 800 Mobile Content (Video & Game) Messaging Point of Sale Carrier Billing 600 commerce. Of consumers with access to Search 72% (*source IAB/PwC) Sources: Of UK Consumers used an 54.6% -ISIS (US) -Boku 1) comScore MobiLens 400 -PayPal -Zong a tablet use them weekly to 2) Ofcom CMR 2012 200 Display (Banners Transactional Sites & app and 54.6% used a 3) IAB & Text Links -Project Oscar (UK) -Mach make purchases (3) 4) FirstPartner 0 Apps Mobile Acceptance Remote Payment mobile browser (1) 2012 2013 2014 2015 2016 n PY Optimised sites and apps allow retailers to -iZettle -PayPal monetise rapidly growing mobile traffic and -Square -Paythru provide effective destinations for campaigns Developers & Platforms Retailers -Verifone -Skrill Publishers -MoPowered (MoBank) -Asos -Net Biscuits -eBay Outdoor & Venue Carrier Reward Programmes Carrier Portals Mobile Websites App Developers Social Networks t -Usablenet -Marks & Spencer Mobile Wallet Loyalty & Coupons -Wapple Brings payment, loyalty & Mobile is a key channel for account functionality into a coupon distribution & loyalty single branded experience. schemes ? The Impact of Weve -Apple Passbook Vendors Schemes r CO -Google Wallet Publisher Sales The JV between the 3 largest UK -O2 Wallet -PayPal -Eagle Eye -Yoose -Foursquare -Mobiqa (NCR) -Groupon -Vouchercloud Campaign -Guardian Media Group MNOs will create a common -Visa V.me 3rd Party Ad Serving & Tracking platform for payments, advertising and data driven targeting and analytics. It is set to significantly -Nectar Delivery Manage the selection, delivery Ad Servers -AdTech -Google -O2 Media -Sky Media Display Sales boost and drive convergence between advertising & commerce. ? Leading Formats Proximity Permission Based Messaging & tracking of ads on behalf of publishers, -Atlas (Microsoft) -doubleclick (Google) -MADS -Everything Everywhere/Blyk -Vodafone -Yahoo Ecosystem aION Search accounts for the highest Deliver advertising -bluepod Provide platforms -Acision -Netsize advertisers , -MediaMind percentage of mobile ad spend at triggered by -JCDecaux & managed -Amobee -OpenMarket agencies and -Mediaplex 73% for the first half of 2012. proximity to an -Proxama services for carrier -Blyk -Sybase 365 ? networks. -Mobile Commmerce -Scanbuy -Incentivated -Upstream Ad Formats Banners and text links account for 23% and other formats 4%. (source IAB UK/PwC) access point, PoS or outdoor display -Screach & enterprise services. -mBlox -Velti CDNs efficiently host & deliver -OpenX -RightMedia (Yahoo!) Content Delivery Networks The Role of Networks Sell Side Platforms & Mediators Used by Publishers graphical & rich Specialist mobile ad networks form Admeld(Google) MoPub media creative -Akami the heart of the trading ecosystem to manage AdMarvel PubMatic -Brightcove bringing togther publishers & networks & Paid Listings Local Search Burstly Rubicon Project exchanges & PAT buyers & reselling remnant Mobclix (Velti) smaato inventory. Leading networks have optimise yield. Search Advertisers bid for high listings Location targeted ads served against selected key words. when a user includes a location Targeting global reach & are the fastest Paid search uses a cost per click in a search, searches in a map growing companies in the sector. model and is dominated by application or has usable Location Audience Data location information enabled on Google with an estimated 95% Real-time Data & DMP Platforms Location targeting is a key Location Targeting Providers Data Aggregators and Data + market share. their device. Management Platform (DMP) Networks t differentiator for mobile. It is being increasingly applied providers deliver audience alongside other targeting profile data to allow real time Premium Specialist Web Banner In App Rich Media data. targeting. Text or static graphical banners Banner, video or interstitial served Delivers additional experience served into mobile web pages. into a mobile App. Accounts within the ad. Includes Sell premium inventory on Consumer Incentivised: Display Click through to a landing page around 50% of display spend. expandable banners, embedded specified media properties games and video or site. Rich Media Creation & Delivery Platforms Planning & Buying Tools Video Tablet Optimised 2nd Screen Video: s ALU Preroll, post roll or interstitial Normally rich media ad optimised Emerging format viewed on the -Celtra -PointRoll -Media Lets -Adobe -Digilant -TubeMogul video that may also be served into an app. Fast growing from a small base for the greater screen space offered by the tablet format mobile device but synchronised with & complementing broadcast or timeshifted TV streams -Adform -IgnitionOne -Turn ? RTA on Mobile Campaign Management Agenices Media Planning & Buying Real Time Advertising uses automted bidding and matching to Permission Mobile CRM Text Response Design & Build Specialist Mobile Media Agencies Blind Semi-Blind allow advertisers to optimise the Messaging r Based Focussed on -Agency Republic Having pioneered the development Develop the -Carat price they pay for a target audience Broker sales of high volume Mix blind and site specific and publishers to optimise their MNO Subscribers opt in to Service and/or promotional Use of text short codes as a creative strategy -Grapple of mobile display and messaging media strategy -Isobar receiving highly targeted offers messages sent by brands & response mechanism in other inventory targeted by channel targeted sales yield. RTA is emerging in mobile & delivering -isobar mobile advertising, these agencies provide for advertisers & -MediaCom from third party advertisers. UK enterprises to opted in media, widely in promotional but volumes traded are still small. i MNOs are investing in the customers in their own competitions & to request media assets -mobile5 strategy, creative , technology and brands & -Mindshare Media foramt which is gaining traction databases additional information across display, -We Love Mobile media services under one roof. purchase media -Target Media with advertisers mobile websites on their behalf. -WPP Agencies & apps -Zenith Optimedia Bluetooth QR Code/NFC Additional content is broadcast QR codes or NFC tags are Full Service Digital Trading Desks Proximity to bluetooth enabled phones scanned to deliver enhanced - within range of an access point. web, or video content. Manage -AKQA (WPP) Established by a -Accuen multi-format -BBH (Publicis) number of (Omnicom) F Augmented Reality 2nd Screen digital -Mindshare agencies to -Cadreon (IPG) Demand Side Platforms Ad Exchanges Ad Exchanges Delivers overlay content on an campaigns on -Ogilivy Advertising optimise RTB by -Harvest image of a location, print media The phone is used to interact Manage real time -Adfonic Mediate between -doubleclick ad exchange or video viewed through the with and control outdoor digital behalf of -Razorfish providing a -Media Innovation purchasing on -dataXu DSPs & SSPs to (Google) advertsing screens brands managed bid- Group (WPP) phone camera behalf of the -Invite Media (Google) trade audiences -Jemm Group based service buyer by matching -MediaMath and manage the -Microsft Advertising Exchange bids & requests -StrikeAd RTB process. -Nexage Prepared by Industry Associations ? V Metrics & Analytics Non Display Buying FirstPartner App Marketing Platforms Provide the audience and Audience Metrics Campaign Analytics Display is the most complex buying tracking analysis necessary to Enable App -Fiksu E ecosystem. Typically Permission Developers to -Tapjoy plan media buying and to call us on find us at based messaging is purchased optimise evaluate the effectiveness of +44 (0) 870 874 8700 www.firstpartner.net directly from the Mobile Network distribution & campaigns. Operator’s sales team and search marketing spend email us at follow us hello@firstpartner.net @firstpartner directly from the provider, often optimised via a buying platform. The map includes information compiled from interviews and information available in the public domain. As information sources are outside our control, FirstPartner makes no representation as to its accuracy or completeness. Responsibility for any interpretation or actions based on this map lies solely with the reader. Advertisers Copyright FirstPartner Ltd 2012 Media & Entertainment FMCG Retail Financial Services Technology & Telecoms Automotive Travel & Hospitality Fashion Explore an Interactive Version of this map at: www.firstpartner.net