Marketing To The Have-Less (A Viable Business Strategy) - An A.I.M. Article

•

0 gefällt mir•864 views

Revolutionary marketing concepts that revolutionize development management do not require new sets of skills nor competencies; rather they require a change in mindset and heartset: the poor is not just a beneficiary, but also a customer with particular needs that can be addressed by the for-profit companies.

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (19)

Ähnlich wie Marketing To The Have-Less (A Viable Business Strategy) - An A.I.M. Article

Ähnlich wie Marketing To The Have-Less (A Viable Business Strategy) - An A.I.M. Article (20)

Mehr von Dickie Aguado, Executive Director - Magna Kultura Foundation

Mehr von Dickie Aguado, Executive Director - Magna Kultura Foundation (6)

Marketing To The Have-Less (A Viable Business Strategy) - An A.I.M. Article

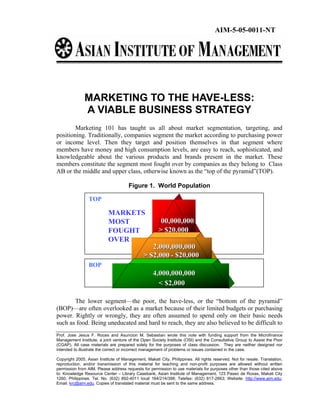

- 1. AIM-5-05-0011-NT MARKETING TO THE HAVE-LESS: A VIABLE BUSINESS STRATEGY Marketing 101 has taught us all about market segmentation, targeting, and positioning. Traditionally, companies segment the market according to purchasing power or income level. Then they target and position themselves in that segment where members have money and high consumption levels, are easy to reach, sophisticated, and knowledgeable about the various products and brands present in the market. These members constitute the segment most fought over by companies as they belong to Class AB or the middle and upper class, otherwise known as the “top of the pyramid”(TOP). Figure 1. World Population TOP MARKETS MOST 100,000,000 FOUGHT > $20,000 OVER 2,000,000,000 > $2,000 - $20,000 BOP 4,000,000,000 < $2,000 The lower segment—the poor, the have-less, or the “bottom of the pyramid” (BOP)—are often overlooked as a market because of their limited budgets or purchasing power. Rightly or wrongly, they are often assumed to spend only on their basic needs such as food. Being uneducated and hard to reach, they are also believed to be difficult to Prof. Jose Jesus F. Roces and Asuncion M. Sebastian wrote this note with funding support from the Microfinance Management Institute, a joint venture of the Open Society Institute (OSI) and the Consultative Group to Assist the Poor (CGAP). All case materials are prepared solely for the purposes of class discussion. They are neither designed nor intended to illustrate the correct or incorrect management of problems or issues contained in the case. Copyright 2005, Asian Institute of Management, Makati City, Philippines. All rights reserved. Not for resale. Translation, reproduction, and/or transmission of this material for teaching and non-profit purposes are allowed without written permission from AIM. Please address requests for permission to use materials for purposes other than those cited above to: Knowledge Resource Center – Library Casebank, Asian Institute of Management, 123 Paseo de Roxas, Makati City 1260, Philippines. Tel. No. (632) 892-4011 local 164/214/398; Telefax: (632) 817-2663; Website: http://www.aim.edu; Email: krc@aim.edu. Copies of translated material must be sent to the same address.

- 2. AIM-5-05-0011-NT Marketing to the Have-Less: A Viable Business Strategy 2 serve. These assumptions, however, are worth re-examining because some companies have already proven them wrong. Grameen Telecom launched the Village Phone Program which aimed to provide mobile phones service in the rural areas of Bangladesh, where around 80 million people resided and earned an average annual per capita income of US$171 as of 2003. The Village Phone (VP) worked as an owner-operated payphone that provided telephone service in rural areas where no such facilities were available previously. Grameen Telecom earned around US$21 in service charges and US$41 in phone bills per VP per month, making the average revenue per VP subscriber twice that of the average business user. By 2003, there were 39,000 VP operators serving 50 million rural Bangladeshis. For Grameen Telecom these figures easily translated to US$9.8 million in service charges and US$19 million in call fees per year. Citibank launched its Suvidha Account specially designed for all employees of small- and medium-scale enterprises (SMEs) in India in 1998. The bank required a minimum deposit of $20 to open an account and all banking transactions were done over the phone or through automated teller machines (ATMs). In 2002, after four years of operations, Citibank served 250,000 depositors in Bangalore alone, which meant that the bank had generated at least US$5 million in deposits from these SME employees. In the Philippines, cellular phone services became affordable to the low-income sector with the advent of prepaid cards and the availability of second-hand phones in the market. The number of subscribers grew from 60,000 in 1992, to 1.1 million in 1997, which marked the launch of the first prepaid program in the market. Prepaid subscribers easily accounted for up two percent of the market that year. By October 2004, there were around 30 million mobile phone subscribers in the country, of whom 97 percent were prepaid subscribers. While the number of subscribers continued to grow, what was established was that on average, each subscriber sent eight short or “text” messages per day, with each message costing Php0.50 to Php1.00. Thus, the industry generated at least Php120 million (US$2 million) in gross revenues per day. By the third quarter of 2004, the two giant mobile phone companies, Smart Communications and Globe Telecom, had earned gross revenues of Php50 billion (US$909 million) and Php39 billion (US$709 million), respectively. Citibank in India and cellular phone services in the Philippines are but a few examples of companies that have started paying attention to the traditionally unattractive market. They have proved that doing business with the have-less could be a viable strategy. Why Market to the Have-Less Why market to the have-less? Though the answers are simple, they may not yet be evident to all: Asian Institute of Management Copyright 2005

- 3. AIM-5-05-0011-NT Marketing to the Have-Less: A Viable Business Strategy 3 • The have-less pay more. • They are not expensive to serve and maintain. • They comprise the largest segment of the market. • Yet, they have limited options. The have-less pay more. To illustrate this contention, take cigarette buying on the streets in the Philippines. As smokers from the low-income class, earning on average Php100 (less than US$2) a day, 1 cannot afford to make a one-time purchase of a cigarette pack at Php10 (roughly US$0.18), they buy cigarettes from street vendors instead, at Php2.00 per stick. By doing so they pay Php1.00 more, or 100 percent higher than if they bought cigarettes one pack at a time from supermarkets, on an on-demand basis. Over-the-air pre-paid load in the Philippines is yet another example. A Php25- load entitles a subscriber to send 25 text messages (or Php1.00 per message). However, the subscriber has only two days to use up the entire load as the load expires thereafter. Since a person on average sends eight messages a day or 16 messages in two days, the Php25-load translates to a cost of Php1.56 per text message. Meanwhile, if a subscriber bought a Php500-valued pre-paid card, he would be entitled to 550 text messages consumable in 60 days, which translates to only Php0.90 per message. Further, even if the subscriber sent an average of eight messages per day, he would have paid only Php1.04 per message. But the low-income group could not afford an upfront cash outlay of Php500 for a prepaid card so they prefer to buy the Php25-over- the-air load as this fits their daily cash flow, never mind that it means having to pay 50 percent more and having to go to the loading centers several times in a week. Upfront Number of Number of Cost per Average usage rate Effective payment messages days before message given expiry date cost per allowed load expires and assuming a message consumption rate of 8 messages per day Php25 25 2 days Php1.00 16 messages Php1.56 Php 300 330 30 days Php0.91 240 messages Php1.25 Php 500 550 60 days Php0.91 480 messages Php1.04 The have-less are not expensive to serve and maintain. Unlike the more sophisticated customers, the have-less are generally after the functionality of the core product and hardly demand frills. For example, hardly would a have-less call the manufacturer of a mobile phone to complain about the poor performance of his unit and demand its immediate replacement. A have-less would also not tend to complain about the delay of his billing statement nor about his non-inclusion in the company’s recent promotional gimmick involving loyal customer rewards, for instance. Hardly, too, if at all, would a have-less threaten not to pay his bill when he receives less-than-perfectly 1 According to Poverty in the Philippines: Income, Assets, and Access (Asian Development Bank, 2005), 44 percent of the Philippine population in 2003 belonged to this income class. Asian Institute of Management Copyright 2005

- 4. AIM-5-05-0011-NT Marketing to the Have-Less: A Viable Business Strategy 4 pleasing customer service, and certainly, neither would he threaten to file a case against the company which may have unwittingly offended him. Instead, the have-less sector, by availing of prepaid phone services, actually cut costs for communications companies due to the lack of a need for billing statements. Further, the sector, by patronizing prepaid services, improves the cash flow of the cell companies through upfront collections. The have-less comprise the largest segment of the market. While over two billion people or a third of the world’s population belong to the most fought-over segment as they earn US$2,000 or more annually, those who earn less than this amount and therefore belong to the have-less segment number four billion. The Philippine population follows the same trend: around 22 million Filipinos or 27 percent of the population earns US$2,000 or more annually, while the remaining 60 million or so Filipinos, who make up 70 percent of the population, earn less than this amount. The same trend has been noted in Brazil. (See Table 3) Figure 2 . Philippine Population TOP Markets Markets Most Most Fought 7,000,000 > $20,000 Fought Over Over 15,000,000 > $2,000 $20,000 - 40,000,000 > $2,000 $1,000 - BOP 20,000,000 < $1,000 Table 3 Brazilian Stratification Breakdown Economic Population Household Inhabitants per Segment (millions / percentage) (millions) Household A 7.3 / 4.15 2.5 2.9 B 21.6 / 12.73 5.4 4.0 C 48.9 / 27.78 12.6 4.0 D 44.2 / 25.11 9.4 4.7 E 54.3 / 30.68 7.6 7.1 Source: C.K. Prahalad, The Fortune at the Bottom of the Pyramid, 2004 Asian Institute of Management Copyright 2005

- 5. AIM-5-05-0011-NT Marketing to the Have-Less: A Viable Business Strategy 5 Finally, the have-less have limited options. When middle-class Filipinos go out for their afternoon snack their choices are limtless: McDonalds’, Jollibee, Wendy’s, Burger King, Chowking, Starbucks, KFC, and so on. But when have-less Filipinos feel the pangs of hunger, all they can afford are five pieces of squid balls worth Php10 and a Php5-cold drink (normally a simple combination of water, sugar, and food color), given their Php20-(US$0.36)daily food allowance. (Note, however, that a squid ball vendor in the Visayas who runs 50 stalls in her area has been able to buy a 200-square-meter residential lot in Metro Manila out of her profits.) The members of the middle class receive at least two pre-approved credit cards in their lifetime: all they have to do is to sign the back of their cards and these become ready for use—no joining fees, no annual fees for the first year, a totally hassle-free credit facility. The monthly interest rates of these credit cards range from 2.5 percent to 3.5 percent applied only on the outstanding balance past the monthly due. So if one were to purchase something on day 1 and repay it on day 30, the due date, s/he would not be charged interest during the days when the credit was outstanding. The have-less, however, have neither a regular income nor a credit history that would warrant creditworthiness. Thus, for their financial needs, they turn to the informal lenders (more popularly known in the Philippines as 5/6 because for every Php5 loan they give, these lenders receive a Php-6 repayment), who charge a flat interest rate of 20 percent per week for a loan of Php500 (US$9) or less, amortized daily. The lenders also charge 20 percent per month for loans amounting to Php1,000 (US$18) or higher, and collect weekly amortizations. The have-less are usually never able to save up for their purchases in banks as these institutions require an initial deposit of Php3,000 (US$54), and a daily maintaining balance of the same amount. Moreover, before applicants may open an account, the banks also require them to present two identification cards such as a company and/or school ID, a passport, a driver’s license, a tax identification number (TIN) card, a social security, or a health card. The administrative and financial requirements for securing these identification cards ultimately make financial services unaffordable to the have-less. And so goes the vicious cycle which allows the loan sharks to prosper. How to Market to the Have-Less Experience shows that the have-less do buy products and avail of services; however, their spending behavior or pattern is certainly different from that of the have- more. Three elements affect the spending decisions of the have-less: • fit of purchase into their cash flow; • affordability; and • access. Asian Institute of Management Copyright 2005

- 6. AIM-5-05-0011-NT Marketing to the Have-Less: A Viable Business Strategy 6 Companies have tried to address these concerns through the following means and have proved successful: • “tingi” or sachet marketing or the offering of smaller packages; • allowing purchases requiring smaller but more frequent cash outlays; and • bringing the products and services right to the customers’ doorstep. Sachet Marketing Even if a have-less earning Php3,000 a month has a 10 percent disposable income per month (the remainder has been allocated to basic necessities), it does not follow that the have-less can afford to buy Php300’s worth of consumer items. The have-less earn this amount not in lump sum but in varying amounts spread over 30 days. Thus the disposable income only translates to Php10 every day on average so that a company which is selling to the have-less market must consider the fact that the have-less have a Php10 daily disposable cash rather than a Php3,000-monthly income. Because of this fit- in-the-cash-flow principle, sachet marketing thrives in the have-less market where shampoo, coffee, face powder, mobile phone load, even landline rates in “tingi” form are ubiquitous. But by offering small quantities, manufacturing companies have to deal with the high cost of packaging, which could be higher than the cost of the product itself. Take Sakto Coke, a 200-milliliter (6.76 ounces) packaging of Coke sold in selected rural areas and some parts of Metro Manila, for example. Because buyers normally split the 12- ounce bottle worth Php10 into two servings, its manufacturer has thought of packaging Coke in bottles with half the content of the original product. Thus the new product variant is called “Sakto,” which is a Filipino colloquial term for “exact,” referring to the amount of serving the product offers. For every Sakto Coke sold at Php5, however, a buyer needs to pay an additional Php4 as deposit for the glass bottle. One gets back the deposit once the bottle is returned to the store or the distribution agent. Improving Affordability The have-less’ income or cash flow pattern does not prevent them from wanting to meet their other needs, including communications, housing, and other high-value items that can improve their quality of life. Casas Bahia of Brazil, in its desire to make furniture and home appliances affordable to the have-less (the class C, D, and E of the Brazilian Stratification Breakdown), has put up a system that allows its customers to purchase merchandise on installment. The repayment period ranges between one and 15 months, and the average monthly interest rate charged on purchases made on installment is 4.13 percent. The result: 70 percent of Casas Bahia customers belong to class E; financed sales are responsible for 90 percent of the company’s total sales volume; and the default rate is 8.5 percent, which is lower than the competitors’ 16 percent. Asian Institute of Management Copyright 2005

- 7. AIM-5-05-0011-NT Marketing to the Have-Less: A Viable Business Strategy 7 Improving Access Even if products and services were made affordable to the have-less, there could yet be another problem involved in marketing to them: access. Health insurance in the Philippines has been made affordable to the masses at a monthly premium of only Php100 (less than US$2), yet some people are discouraged from availing of it because of the absence of hospitals and health care service providers within a 14-kilometer radius of their residence. Another example would be telecommunications in Bangladesh. In the late 1990s, the Bangladeshis in the rural areas were willing to spend at least 1.5 percent or US$ 2.57 of their per capita income on fixed telephone lines, but the expansion of these facilities from the urban areas to the rural areas remained limited because of an interconnection problem with the main system. As mentioned earlier, Grameen Telecom tried to overcome this problem of access to telecommunications by launching its VP program by bringing mobile phones within the reach, both financial and geographical, of the rural Bangladeshis. Door-to-door selling has proven to be one of the most effective modes of marketing, regardless of the geographic location and economic class of customers, because it addresses the problem of access. It has worked well for Avon and other multi- level marketing companies as well as for the “sorbetero”, the traditional ice cream seller in the Philippines. The sorbetero pushes a cart of ice cream around the neighborhood, rings a bell to call the people’s attention, and manually scoops the ice cream into a cone for a buyer. A regular serving costs Php5 while a bigger one sells for Php10. Unsurprisingly, big ice cream manufacturers such as Selecta Walls, Inc. and Nestle have followed suit by having their own distribution agents, who ride a bicycle laden with a box of various, individually-packed ice cream products. These agents go around the neighborhood accompanied by a loud, distinct jingle announcing their presence. They use the same selling concept as the traditional sorbetero but with a tinge of sophistication. The Five Principles of Innovation In addressing the abovementioned obstacles, companies should keep the five principles of innovation 2 in mind, as have the sachet manufacturers, Casas Bahia, Grameen Telecom, and the “sorbetero” clones: 1. Understand the product functionality needed by the have-less. Serving the have- less is similar to doing business with the top of the pyramid in the sense that it should start with understanding their needs. Lost limbs due to accidents, war, and polio are common cases in India which has about 5.5 million amputees, most of them poor and illiterate. Their number increases at 25,000 to 30,000 per year. However, imported prosthetics from the developed 2 Based on C.K. Prahalad’s Twelve Principles of Innovation for BOP Markets. Asian Institute of Management Copyright 2005

- 8. AIM-5-05-0011-NT Marketing to the Have-Less: A Viable Business Strategy 8 countries are not only unaffordable to the poor at US$7,000 to US$8,000 per foot, but also fail to serve the needs of the market. Indians do not wear shoes to the temple nor in the kitchen. Moreover, they also squat on the floor, sit cross-legged, work in the field, and stand in water for about eight hours every day, and walk on uneven ground and long distances of about eight to ten kilometers per day. Because of the Indians’ way of life and the have-less’ incapability to obtain frequent replacements or make frequent hospital visits, the prosthetic must be comfortable, durable, and quick to make. Jaipur Foot is able to meet all these requirements and sells prosthetics at less than US$30 per foot. 2. Focus on the price performance of products and services. Lowering prices by 10 percent or so is not enough; serving the have-less may require improving the price performance 30 to 100 times over. Jaipur Foot and Auroloab present good examples of this price performance principle. Aurolab manufactures affordable, high-quality ophthalmic consumables, including intra ocular lenses (IOLs) which are artificial lenses implanted in the eye during a cataract operation. Since its establishment in 1992, the average price of IOLs made by the other companies has dropped from between $300 and $400, to between $100 and $150. Meanwhile, Aurolab makes these lenses available for $3 to $8 per lens. Instead of using the traditional cost-plus-margin method of setting prices, Aurolab first set a target selling price to ensure the affordability of its products for its target market, which consists of the poor and the middle class in developing countries. Then it computed its cost and margin to fit the target selling price after which it hired personnel who ensured that the products were of high quality. After more than a decade, the company has become one of the world’s largest producers of intraocular lenses, with a 10-percent market share. It sells more than 600,000 units per year to 120 countries. 3. Ensure that products and services reach the have-less. Distribution is also critical in marketing to the have-less who are mostly located in the rural areas, the hard-to- reach highlands and islands where infrastructure is, more often than not, inadequate. ICICI Bank of India started as an institutional lender in 1994 before going into retail banking in 1997. In the process it veered away from traditional branch banking and installed 1,750 automated teller machines (ATMs), acquired The Bank of Madura which had established a rural distribution network through self-help groups (10,000 of them serving around 200,000 customers), and partnered with rural marketers, kiosk operators, non-government organizations (NGOs), and microfinance organizations. By 2003 ICICI had a retail base of 9.8 million accounts. 4. Make products able to withstand a hostile environment. Given the inadequate infrastructure where the have-less are located, products must be designed to withstand a hostile environment and to remain functional in one. Asian Institute of Management Copyright 2005

- 9. AIM-5-05-0011-NT Marketing to the Have-Less: A Viable Business Strategy 9 ITC established E-Choupal (which means “the village meeting place”) to connect Indian villages in a “seamless supply chain.” More often than not the villagers used computers in the Internet kiosks to check farm prices. However, to make the rural network application work, ITC had to contend with voltage fluctuations which ranged from 90 to 350 volts against a rated 220-volt transmission. The supply of electricity was also irregular, lasting only two to three hours some days. Thus ITC installed an uninterruptible power supply system, which consisted of surge protectors and solar panels, as well as a satellite network for communications purposes. Greenstar, a for-profit organization founded in 1998, builds solar-powered community centers that deliver services to villages in the developing world. Using solar power generated by large photovoltaic panels, the centers could drive a water purifier, a small clinic, a vaccine cooler, a classroom, a digital studio, and a satellite or wireless link to the Internet. The centers are owned by the villagers themselves. By 2004 the organization had completed pilot installations in a remote Bedouin settlement on the West Bank in the Middle East; in a small community in the Blue Mountains of Jamaica; in the central Indian village of Parvatapur; in a traditional Ashanti community in Ghana; and in over 60 other communities on all continents of the world. 5. Conserve resources: eliminate, reduce, and recycle. Since the have-less comprise the biggest segment of the market and are likely to become the biggest user of retail or sachet products, it follows that the products sold to them would also require the biggest volume of packaging materials. Waste management thus becomes a major concern. Further, the developed markets are accustomed to resource wastage. All innovations must therefore focus on conserving resources. It is believed that installing a recycling system may not be practical as rural markets are dispersed and the collection of waste resources may not be economically viable. So far, no company has as yet come up with a solution to this potential waste management problem. Principles on Marketing to the Have-Less Marketing to the have-less poses challenges in terms of discovering the peculiarities of the emerging have-less market as this segment has consumption and spending patterns different from the have-more. Moreover, marketing to the have-less means having to contend with a different kind of physical environment. However, the age-old principles of marketing remain: well-defined segmentation; accurate targeting; and clear positioning, which leads to innovations in product development, packaging, pricing, and distribution. Ultimately, the challenge to companies doing business with the have-less is to mine the fortune held in small quantities by the huge number of the yet-to- be tapped customers. Asian Institute of Management Copyright 2005

- 10. AIM-5-05-0011-NT Marketing to the Have-Less: A Viable Business Strategy 10 References Asian Development Bank. 2005. Poverty in the Philippines: Income, Assets, and Access, Greenstar Solar Community Center, <http://www.greenstar.org/> Herbst, Kris. “Compassionate Manufacturing: Aurolab Does Business with the Poor.” <http://www.changemakers.net/journal/03january/herbst/cfm> Prahalad, C.K. 2004. The Fortune at the Bottom of the Pyramid. New Jersey: Wharton School Publishing. Richardson, Don et al. 2000. Grameen Telecom’s Village Phone Programme in Rural Bangladesh: a Multi-Media Case Study. Asian Institute of Management Copyright 2005