Dividend Policy and Dividend Decision Theories.pptx

25 March Daily market report

1. Page 1 of 6

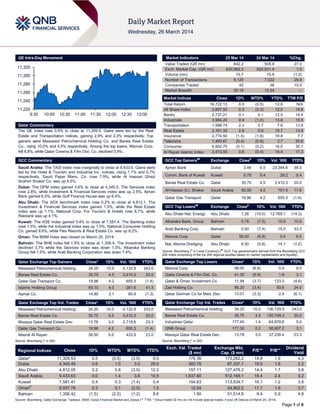

QE Intra-Day Movement

Qatar Commentary

The QE index rose 0.5% to close at 11,309.5. Gains were led by the Real

Estate and Transportation indices, gaining 2.9% and 2.3% respectively. Top

gainers were Mesaieed Petrochemical Holding Co. and Barwa Real Estate

Co., rising 10.0% and 4.5% respectively. Among the top losers, Mannai Corp.

fell 6.8%, while Qatar Cinema & Film Dist. Co. declined 5.9%.

GCC Commentary

Saudi Arabia: The TASI index rose marginally to close at 9,433.6. Gains were

led by the Hotel & Tourism and Industrial Inv. indices, rising 1.1% and 0.7%

respectively. Saudi Paper Manu. Co. rose 7.9%, while Al Hassan Ghazi

Ibrahim Shaker Co. was up 4.5%.

Dubai: The DFM index gained 0.6% to close at 4,345.5. The Services index

rose 2.8%, while Investment & Financial Services index was up 2.5%. Ajman

Bank gained 6.5%, while Gulf Finance House was up 6.4%.

Abu Dhabi: The ADX benchmark index rose 0.2% to close at 4,812.1. The

Investment & Financial Services index gained 1.5%, while the Real Estate

index was up 1.1%. National Corp. For Tourism & Hotels rose 8.7%, while

Rakbank was up 4.1%.

Kuwait: The KSE index gained 0.4% to close at 7,581.4. The Banking index

rose 1.5%, while the Industrial index was up 1.0%. National Consumer Holding

Co. gained 9.6%, while Flex Resorts & Real Estate Co. was up 8.2%.

Oman: The MSM index was closed on March 25, 2014.

Bahrain: The BHB index fell 1.5% to close at 1,356.4. The Investment index

declined 3.7% while the Services index was down 1.5%. Albaraka Banking

Group fell 7.5%, while Arab Banking Corporation was down 7.4%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Mesaieed Petrochemical Holding 34.25 10.0 4,132.8 243.0

Barwa Real Estate Co. 35.75 4.5 3,410.3 20.0

Qatar Gas Transport Co. 19.96 4.2 655.3 (1.4)

Islamic Holding Group 65.10 4.0 281.6 41.5

Aamal Co. 14.80 3.1 80.9 (1.3)

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Mesaieed Petrochemical Holding 34.25 10.0 4,132.8 243.0

Barwa Real Estate Co. 35.75 4.5 3,410.3 20.0

Mazaya Qatar Real Estate Dev. 13.78 3.0 2,718.6 23.3

Qatar Gas Transport Co. 19.96 4.2 655.3 (1.4)

Masraf Al Rayan 38.50 0.0 433.9 23.0

Source: Bloomberg (* in QR)

Market Indicators 25 Mar 14 24 Mar 14 %Chg.

Value Traded (QR mn) 642.2 505.8 27.0

Exch. Market Cap. (QR mn) 630,962.2 624,831.4 1.0

Volume (mn) 15.7 15.8 (1.2)

Number of Transactions 9,125 7,022 29.9

Companies Traded 42 38 10.5

Market Breadth 20:18 12:24 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 16,722.13 0.5 (0.5) 12.8 N/A

All Share Index 2,897.50 0.5 (0.3) 12.0 14.6

Banks 2,737.21 0.1 0.1 12.0 14.4

Industrials 3,984.20 0.9 (1.0) 13.8 15.5

Transportation 1,998.74 2.3 0.7 7.6 13.9

Real Estate 2,161.33 2.9 0.6 10.7 13.9

Insurance 2,774.50 (1.5) (1.8) 18.8 7.7

Telecoms 1,493.67 (0.4) (0.9) 2.7 20.6

Consumer 6,902.75 (0.1) (0.2) 16.0 30.1

Al Rayan Islamic Index 3,473.50 0.6 (0.4) 14.4 17.3

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Ajman Bank Dubai 3.46 6.5 23,344.6 39.5

Comm. Bank of Kuwait Kuwait 0.78 5.4 29.2 5.4

Barwa Real Estate Co. Qatar 35.75 4.5 3,410.3 20.0

Al-Hassan G.I. Shaker Saudi Arabia 82.00 4.5 751.0 17.6

Qatar Gas Transport Qatar 19.96 4.2 655.3 (1.4)

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Abu Dhabi Nat. Energy Abu Dhabi 1.26 (10.0) 12,769.1 (14.3)

Albaraka Bank. Group Bahrain 0.78 (7.5) 15.9 10.0

Arab Banking Corp Bahrain 0.50 (7.4) 15.0 33.3

Mannai Corp. Qatar 98.00 (6.8) 0.4 9.0

Nat. Marine Dredging Abu Dhabi 8.50 (5.6) 14.1 (1.2)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Mannai Corp. 98.00 (6.8) 0.4 9.0

Qatar Cinema & Film Dist. Co. 41.35 (5.9) 1.8 3.1

Qatar & Oman Investment Co. 11.94 (3.7) 123.3 (4.6)

Zad Holding Co. 86.20 (3.4) 50.6 24.0

Qatar German Co for Med. Dev. 13.01 (3.3) 2.4 (6.1)

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Mesaieed Petrochemical Holding 34.25 10.0 136,729.5 243.0

Barwa Real Estate Co. 35.75 4.5 120,749.3 20.0

Industries Qatar 177.40 1.4 64,879.6 5.0

QNB Group 177.30 0.2 58,607.2 3.1

Mazaya Qatar Real Estate Dev. 13.78 3.0 37,238.4 23.3

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 11,309.53 0.5 (0.5) (3.9) 9.0 176.36 173,262.2 14.8 1.9 4.3

Dubai 4,345.49 0.6 1.0 3.0 29.0 360.78 87,337.1 19.0 1.6 2.2

Abu Dhabi 4,812.05 0.2 0.6 (3.0) 12.2 157.11 127,476.2 14.4 1.7 3.8

Saudi Arabia 9,433.63 0.0 1.4 3.6 10.5 1,837.60 512,169.1 19.4 2.4 3.2

Kuwait 7,581.41 0.4 0.3 (1.4) 0.4 154.63 113,534.7 16.1 1.2 3.8

Oman#

6,937.78 0.3 0.1 (2.5) 1.5 12.04 24,902.2 11.1 1.6 3.7

Bahrain 1,356.42 (1.5) (2.2) (1.2) 8.6 1.90 51,514.8 9.4 0.9 4.8

Source: Bloomberg, Qatar Exchange, Tadawul, MSM, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) (# Data as of March 24, 2014)

11,220

11,240

11,260

11,280

11,300

11,320

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QE index rose 0.5% to close at 11,309.5. The Real Estate

and Transportation indices led the gains. The index rose on the

back of buying support from non-Qatari shareholders despite

selling pressure from Qatari shareholders.

Mesaieed Petrochemical Holding Co. and Barwa Real Estate Co.

were the top gainers, rising 10.0% and 4.5% respectively.

Among the top losers, Mannai Corp. fell 6.8%, while Qatar

Cinema & Film Dist. Co. declined 5.9%.

Volume of shares traded on Tuesday fell by 1.2% to 15.7mn

from 15.8mn on Monday. However, as compared to the 30-day

moving average of 14.2mn, volume for the day was 10.5%

higher. Mesaieed Petrochemical Holding Co. and Barwa Real

Estate Co. were the most active stocks, contributing 26.4% and

21.8% to the total volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Ratings, Earnings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Dar Al Arkan Real

Estate

Development Co.

(DAAR)

S&P

Saudi

Arabia

LT B+ B+ – Positive –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC –

Local Currency)

Earnings Releases

Company Market Currency

Revenue

(mn) 4Q2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

% Change

YoY

Sharjah Insurance Company

(SICO)*

UAE AED 37.2 (27.3) – – 5.3 (3.4)

Abu Dhabi National Energy

Company (TAQA)*

Abu Dhabi AED 25,757.0 (7.3) – – (1,768.0) NA

Source: Company data, DFM, ADX, MSM (*FY2013 results)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

03/25 US FHFA FHFA House Price Index MoM January 0.50% 0.60% 0.70%

03/25 US S&P/Case-Shiller S&P/CS 20 City MoM SA January 0.85% 0.60% 0.74%

03/25 US S&P/Case-Shiller S&P/CS Composite-20 YoY January 13.24% 13.34% 13.38%

03/25 US S&P/Case-Shiller S&P/CaseShiller Home Price Index January 165.5 165.7 165.6

03/25 US Conference Board Consumer Confidence Index March 82.3 78.5 78.3

03/25 France INSEE Production Outlook Indicator March -11.0 – -6.0

03/25 France INSEE Manufacturing Confidence March 100.0 100.0 100.0

03/25 France INSEE Business Confidence March 95 95 94

03/25 Germany IFO Institute IFO Business Climate March 110.7 110.9 111.3

03/25 UK ONS CPI MoM February 0.50% 0.50% -0.60%

03/25 UK ONS CPI YoY February 1.70% 1.70% 1.90%

03/25 UK ONS CPI Core YoY February 1.70% 1.60% 1.60%

03/25 UK ONS Retail Price Index February 254.2 253.9 252.6

03/25 UK ONS RPI MoM February 0.60% 0.50% -0.30%

03/25 UK ONS RPI YoY February 2.70% 2.60% 2.80%

03/25 UK ONS PPI Input NSA MoM February -0.40% 0.30% -0.90%

03/25 UK ONS PPI Input NSA YoY February -5.70% -5.30% -2.90%

03/25 UK ONS PPI Output NSA MoM February 0.00% 0.20% 0.30%

03/25 UK ONS PPI Output NSA YoY February 0.50% 0.70% 0.90%

03/25 UK ONS ONS House Price YoY January 6.80% 6.60% 5.50%

03/25 UK BBA BBA Loans for House Purchase February 47550 50000 49341

03/25 Spain INE PPI MoM Feb -0.70% – -1.40%

03/25 Spain INE PPI YoY Feb -2.90% – -1.90%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 58.66% 62.98% (27,717,084.28)

Non-Qatari 41.34% 37.02% 27,717,084.28

3. Page 3 of 6

News

Qatar

Qatar now a major financial center – Qatar’s Finance Minister

HE Ali Shareef al Emadi said the country has emerged as one of

the leading financial centers in the world with a steady GDP

growth rate of above 6%. Al Emadi added that Qatar's GDP

grew by 6.5% in 2013 and is estimated to grow up to 6% in

2014. The private sector in Qatar is expected to grow more than

10% in 2014 as policies and strategies adopted by the Qatari

government have given a major boost to the non-hydrocarbon

sector. (Qatar Tribune)

QE upgrade to bring in QR3bn funds, reflects global

confidence – The Qatar Exchange’s (QE) upgrade to emerging

market status by both MSCI and Standard & Poor’s Dow Jones

is likely to see as much as QR3bn foreign funds inflow, reflecting

global investment institutions’ growing confidence in the bourse.

The QE’s Chief Executive Rashid bin Ali al-Mansoori said these

upgrades are likely to enhance the trustworthiness of the market

and consequently attract large foreign portfolios. Both MSCI and

S&P Dow Jones decided to upgrade the QE to emerging market

from the current frontier status, effective from June 2014 and

September 2014 respectively. (Gulf-Times.com)

Qatar budget to see higher infrastructure outlay – The

Government of Qatar, which is rapidly diversifying its economy

away from hydrocarbons, said its general budget for 2014-15

will have higher allocation for infrastructure, logistics, education

and health sectors. The Finance Minister HE Ali Sherif al-Emadi

said ample allocations have also been made for sports-related

activities in view of the country hosting the 2022 FIFA World

Cup. According to him, the higher allocations would encourage

the private sector in a big way to contribute to Qatar’s economy.

Recently, the Advisory Council discussed a report of the

financial & economic affairs on the draft budget of the state’s

major public projects of FY2014-15, and decided to refer its

recommendations to the cabinet. (Gulf-Times.com)

Zad Holding posts net profit of QR125mn in 2013 – Zad

Holding (ZHCD) has posted a net profit of QR125mn in 2013

versus QR110mn in 2012. Earnings per Share (EPS) amounted

to QR5.81 in 2013 compared to QR5.11 in 2012. The Board of

Directors has proposed cash dividends of 35% subject to the

General Assembly approval. (QE)

QFB reports 24% rise in net income in 2013 – Qatar First

Bank (QFB) reported a net income of QR140.5mn in 2013, up

24%. Meanwhile, the AGM approved the distribution of 8% of

paid-up share capital to QFB’s shareholders. (Bloomberg)

RasGas: Qatar well-placed for stable LNG supply – RasGas

Company’s CEO Hamad Rashid Al Mohannadi said that Asia’s

growing energy requirements call for supply from a diverse

portfolio of established LNG producers with a proven record of

reliability. Al Mohannadi highlighted the fact that Asian

customers need to remain focused on projects with strong and

economically viable resources that are serviced by experienced

developers and operators. Al Mohannadi said Qatar’s stable

political and economic environment provides the platform for the

continued reliable supply of LNG from its existing LNG

production facilities. He added that the country is ideally

positioned to lead the global shift towards an increased use of

gas and to meet the expanding requirements for LNG in Asia.

(Peninsula Qatar)

QIBK seeks strategic stake in Bank Asya – Qatar Islamic

Bank (QIBK) is contemplating to acquire a strategic stake in

Turkey-based Bank Asya as part of its international expansion.

A QIBK spokesman confirmed that the bank has entered into an

exclusive discussion with the Turkish lender. QIBK intends to

support Bank Asya’s medium to long-term growth strategy for

positioning it as the leading Islamic bank in Turkey. QIBK plans

to finalize the transaction within the next few months, subject to

obtaining the required regulatory approvals. Meanwhile, QInvest

is acting as financial adviser to QIBK on this acquisition. (Gulf-

Times.com)

Laffan Refinery set to become world’s largest condensate

facility – The Laffan Refinery 2 (LR2) will process 146,000

barrels per stream day (bpsd) of condensate feedstock, doubling

the refining capacity of LR1 once it is completed in 3Q2016.

Chief Operating Officer, Refinery Ventures at Qatargas, Salman

Ashkanani said combining LR1 and LR2 operations will make

the whole Laffan Refinery the largest condensate facility in the

world. Ashkanani said that LR2 is expected to process 71,000

bpsd of naphtha, 60,800 bpsd of kerosene, 27,000 bpsd of

gasoil and 850 tons of LPG, including butane and propane. He

noted that LR2, along with other projects, will strengthen the

country’s capacity to meet increasing demand for transport fuels

especially Jet A-1 (low sulfur jet fuel). Besides major refinery

products, he said LR-related projects such as the diesel

hydrotreater will also produce low sulfur diesel that will serve the

local market. However, refined products from LR2 will be

exported to different countries. (Gulf-Times.com)

QE suspends trading in QNNS, MERS shares on March 26 –

The Qatar Exchange (QE) has announced a suspension in the

trading of shares of the Qatar Navigation Company (QNNS) and

Al Meera Consumer Goods Company (MERS) on March 26,

2014 due to the companies’ AGM being held on that day. (QE)

MPHC’s AGM to be held on April 9 – Mesaieed Petrochemical

Holding Company’s (MPHC) AGM is scheduled to be held on

April 9, 2014 at La Cigale Hotel. The AGM’s agenda includes

approving the board’s recommendation of distributing QR0.35

per share, among others. (QE)

MARK to disclose 1Q2014 results on April 23 – Masraf Al

Rayan (MARK) will disclose its 1Q2014 financial results on April

23, 2014. (QE)

IHGS to disclose 1Q2014 results on April 8 – The Islamic

Holding Group (IHGS) will disclose its 1Q2014 financial results

on April 8, 2014. (QE)

QCFS’ AGM approves 20% dividend – Qatar Cinema & Film

Distribution Company’s (QCFS) AGM has approved the

distribution of 20% cash dividend equivalent to QR2.00 per

share. (QE)

QOIS’ AGM approves 6% dividend – Qatar Oman Investment

Company’s (QOIS) AGM has approved the board’s

recommendation for distributing 6% cash dividend (QR0.60 per

share). (QE)

International

Bullish consumers, rising home prices brighten US

economy – The US consumer confidence surged to a six-year

high in March 2014 and house prices rose solidly in January,

positioning the economy for a stronger growth after a weather-

induced soft spot. The upbeat outlook, however, was dimmed by

other data showing new home sales at a five-month low in

February, partly because of cold weather. A senior economist at

Moody's Analytics stated that the US economy is showing signs

of shaking off the weather effect and a big lift is expected in the

second quarter. The Conference Board said its index of

consumer attitudes rose to 82.3 from 78.3 in February. That is

the highest level since January 2008, which beat economists'

4. Page 4 of 6

expectations for a reading of 78.6. The jump in confidence

bodes well for the economy's prospects, even though

consumers were less upbeat about the labor market. (Reuters)

Bundesbank opens door to QE in Europe – Germany's

central bank, Bundesbank said the European Central Bank

(ECB) could buy loans and other assets from banks to help

support the Eurozone economy, which marks a radical change

of its stance on the contested policy. The ECB has promised to

keep its interest rates low for some time, having already flooded

the banking system with cheap crisis loans. However, the

Eurozone economy is still weak and inflation remains stuck well

below the central bank's target. With the debate over possible

alternative measures picking up pace, Bundesbank President

Jens Weidmann said the ECB could consider purchasing

Eurozone government bonds or top-rated private sector assets.

That has opened the door to one of the most divisive policy

options – quantitative easing (QE) – to which the German

central bank was consistently averse to. (Reuters)

UK inflation hits new four-year low, wages still lag –

Consumer price inflation in the UK fell to its lowest in more than

four years in February, easing pressure on Britons' living

standards ahead of next year's election and dipping further

below the Bank of England's 2% target. Prices have been rising

faster than pay almost continuously since the start of the

financial crisis in early 2008, and the fall in living standards

despite recent strong economic growth was a major line of

attack by the opposition Labor Party. The Office for National

Statistics said after inflation fell to 1.7%, its lowest since October

2009, and a small pick-up in wage growth, the gap between the

two is at its narrowest since April 2010. February's drop in

inflation was in line with economist expectations and largely

driven by the biggest drop in fuel prices since September 2009,

as well as smaller increases in clothing prices, electricity and

heating bills. It follows a sharp fall over the past six months in

inflation, which dipped below the BoE's 2% target in January for

the first time in more than four years. (Reuters)

Reuters: Spooked by defaults, China banks begin retreat

from risk – Some of China's struggling firms are finally getting

the reception that regulators have been hoping for – a cold

shoulder from banks in the form of smaller and costlier loans.

Reuters contacted around 80 companies with elevated debt

ratios or problems with overcapacity. These interviews showed

that more discriminate lending – long a missing ingredient of

China's economic transformation – has become a reality. Up

against a cooling Chinese economy and signs that authorities

will not step in every time a loan goes bad, banks are becoming

more hard-nosed and selective about whom they lend to. There

are signs that even state-owned firms, have to contend with

higher rates, lower lending limits and more onerous checks by

banks. (Reuters)

Regional

NWC plans SR2bn water projects in Taif – National Water

Company (NWC) is planning SR2bn worth of water-

infrastructure projects in the tourist region of Taif. The utility is

working to increase capacity in the City of Roses near the

mountainous Al Hada area to meet rising demand for water. Taif

already has 30 water projects that started last year including

supply networks, sewage systems, treatment plants and a

reservoir. Dams are planned as well for Makkah and Riyadh.

OPEC’s biggest oil producer expects to complete the world’s

largest desalination plant by 2018 in Rabigh on the Red Sea

near Taif that will be able to supply 600,000 cubic meters of

water a day. It is already the largest producer of desalinated

water in the world. (Bloomberg)

Tadawul deposits Al Jouf’s bonus shares – The Saudi Stock

Exchange (Tadawul) announced the addition of Al Jouf

Agricultural Development Company’s (Al Jouf) bonus shares

into its investors’ portfolios. Earlier, Al Jouf’s EGM approved an

increase in the company’s capital via bonus shares. The

fluctuation limits for Al Jouf’s shares on March 25, 2014 will be

based on a stock price of SR43.30. (Tadawul)

Weqaya Takaful to raise capital via SR150mn rights issue –

Weqaya Takaful Insurance & Reinsurance Company’s (Weqaya

Takaful) board of directors has recommended an increase in the

company's capital by offering a rights issue worth SR150mn.

The rights issue will be limited to those shareholders who are

registered at the close of trading on the extraordinary general

assembly day, which will be determined later. (Tadawul)

Eaton appoints SETRA as its systems integrator – Eaton has

signed a MoU to appoint Saudi Electronic Trading Company

(SETRA) as its local system integrator in the data center market.

In partnership with SETRA, Eaton will provide localized

uninterruptable power supply (UPS) solutions to the Saudi

market. (GulfBase.com)

Saudi cabinet approves new company for industrial

investment – According to sources, Saudi Arabia's cabinet has

approved the creation of a new company to invest in various

manufacturing industries with a capital of SR2bn. The new

company will focus on conversion industries that rely on

petrochemicals, plastics, fertilizers, steel, aluminum and basic

industries and that achieve economic diversification. The new

company will be a JV between the finance ministry's Public

Investment Fund, Saudi Aramco and Saudi Basic Industries

Corporation. (GulfBase.com)

Hanco acquires rental firm Byrne for $163mn – Al Tala'a

International Transportation Company Ltd (Hanco) has acquired

Byrne Investments and its subsidiaries from Havenvest Private

Equity Middle East and HSBC Bank Middle East, for a value of

$163mn. The subsidiaries include Byrne Equipment Rental and

Spacemaker. Venture Capital Bank has joined Hanco in the

acquisition and will acquire a 25% stake in Byrne. The

transaction was partly financed by UAE’s First Gulf Bank, while

GIB Capital and Baker & Mckenzie advised Hanco on the

transaction. (GulfBase.com)

Etihad Rail forms JV with Deutsche Bahn – The UAE’s

railway developer Etihad Rail has signed a JV deal with a unit of

Germany’s Deutsche Bahn to operate and maintain the

country’s planned AED40.4bn rail network. The JV, Etihad Rail-

DB will manage operations for the first stage of the railway,

transporting granulated sulfur on a 264km route from Shah and

Habshan to the port of Ruwais. The JV will further act as

consultant for future stages of the project. (GulfBase.com)

Tabreed declares 5 fils dividend – The National Central

Cooling Company’s (Tabreed) Annual General Assembly has

approved the board’s recommendation for the distribution of

dividend worth 5 fils per share. (DFM)

Dubai airport traffic up 11.7% in February – According to the

traffic statistics issued by operator Dubai Airports, passenger

traffic at Dubai International reached 5.67mn in February 2014,

up 11.7% from 5.08mn recorded during February 2013. YTD

passenger traffic rose 13.5% to 12.07mn passengers, up from

10.64mn during the first two months of 2013. (GulfBase.com)

SICO’s BoD proposes 10% cash dividend – Sharjah

Insurance Company’s (SICO) board of directors has proposed

the distribution of 10% cash dividend for 2013. (ADX)

5. Page 5 of 6

Gulf Capital plans to sell remaining GMS stake – Gulf Capital

plans to sell off its remaining stake in offshore contractor Gulf

Marine Services (GMS) over the next two years after generating

gains of $600mn through the firm’s IPO. Through its buyout

fund, Gulf Capital reduced its shareholding in GMS from 80% to

49.7% last week through an IPO on the London Stock

Exchange. (GulfBase.com)

Kuwait allows foreign banks open more branches – Kuwait

will allow foreign banks to open multiple branches in the country

to spur growth, though analysts doubt many banks will take

advantage of the offer unless the government accelerates its

long-postponed investment projects. For years, the OPEC

member's economic performance has lagged other Arab oil

exporters as ingrained political tensions between the cabinet

and parliament, and entrenched bureaucracy have delayed

business reforms and multi-billion-dollar infrastructure plans.

The Central Bank of Kuwait said that it has formulated new

rules, which will have a positive impact on the local market as

they enrich the type of services being offered. Previously, each

foreign bank was limited to opening one branch in Kuwait; that

restriction will now be removed, though the central bank will still

approve new branches on a case-by-case basis. (Reuters)

AHEC wins OMR50mn EPC contract – Al Hassan Engineering

Company (AHEC) has won an EPC contract for Rabab Harweel

power plant and the HRSG project from PDO for an amount of

OMR50mn. The work is expected to be completed by August

2018. (GulfBase.com)

Orpic awards $40mn PMC contract to EIL – Engineers India

Ltd (EIL) has been awarded a project management consultancy

(PMC) contract worth $40mn by Oman Refineries & Petroleum

Industries Co (Orpic) for its Liwa Plastics Project in Sohar. The

contract scope also includes the gas extraction plant at Fahud

as well as transfer of natural gas liquids from Fahud to Sohar

(GulfBase.com)

AUB declares 18% dividend, 5% bonus shares – Ahli United

Bank’s (AUB) AGM and EGM have approved the board’s

proposal for the distribution of 18% cash dividend and 5% bonus

shares. (Bahrain Bourse)

UFC declares 6 baizas dividend – The United Finance

Company’s (UFC) AGM has approved the distribution of cash

dividend at the rate of 6 baizas per share. (Bahrain Bourse)

PineBridge acquires 50% stake in Romatem – PineBridge

Investments Middle East (PBME) has acquired a 50% equity

stake in Romatem, a leading physical therapy and rehabilitation

services chain in Turkey. The investment will support

Romatem’s growth strategy, which includes establishing more

hospitals and clinics across Turkey as well as international

expansion. (GulfBase.com)

Batelco plans further buy-back of 2020 bonds – Bahrain

Telecommunications (Batelco) is planning to buy back a third of

outstanding bonds due in 2020, using excess liquidity from a

scrapped acquisition to lower its debt servicing costs. The

company has offered to buy back up to $200mn in principal

amount of its 4.25%, $604.4mn guaranteed notes maturing in

2020, with the price being determined by a modified Dutch

auction process. Batelco began buying back its 2020 notes,

through which it had originally raised $650mn in November

2013. (Reuters)

6. Contacts

Saugata Sarkar Keith Whitney Sahbi Kasraoui

Head of Research Head of Sales Manager - HNWI

Tel: (+974) 4476 6534 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg (*Market closed on March 25, 2014)

Source: Bloomberg (*Market closed on March 25, 2014) Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13

QE Index S&P Pan Arab S&P GCC

0.0%

0.5% 0.4%

(1.5%)

0.0%

0.2%

0.6%

(2.0%)

(1.6%)

(1.2%)

(0.8%)

(0.4%)

0.0%

0.4%

0.8%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman*

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,311.20 0.2 (1.8) 8.8 DJ Industrial 16,367.88 0.6 0.4 (1.3)

Silver/Ounce 19.99 0.2 (1.7) 2.7 S&P 500 1,865.62 0.4 (0.0) 0.9

Crude Oil (Brent)/Barrel (FM

Future)

106.99 0.2 0.1 (3.4) NASDAQ 100 4,234.27 0.2 (1.0) 1.4

Natural Gas (Henry

Hub)/MMBtu

4.50 1.9 4.2 3.5 STOXX 600 328.57 1.3 0.2 0.1

North American Spot LPG

Propane Price*

102.00 0.0 (2.6) (19.2) DAX 9,338.40 1.6 (0.0) (2.2)

North American Spot LPG

Normal Butane Price*

127.12 0.0 (1.4) (6.9) FTSE 100 6,604.89 1.3 0.7 (2.1)

Euro 1.38 (0.1) 0.2 0.6 CAC 40 4,344.12 1.6 0.2 1.1

Yen 102.26 0.0 0.0 (2.9) Nikkei 14,423.19 (0.4) 1.4 (11.5)

GBP 1.65 0.2 0.3 (0.2) MSCI EM 958.49 0.5 1.4 (4.4)

CHF 1.13 (0.2) 0.0 1.2 SHANGHAI SE Composite 2,067.31 0.0 1.0 (2.3)

AUD 0.92 0.4 0.9 2.8 HANG SENG 21,732.32 (0.5) 1.4 (6.8)

USD Index 79.94 0.0 (0.2) (0.1) BSE SENSEX 22,055.21 (0.0) 1.4 4.2

RUB 35.60 (1.4) (1.8) 8.3 Bovespa 48,180.14 0.4 1.7 (6.5)

BRL 0.43 0.4 0.6 2.3 RTS 1,170.20 3.4 3.0 (18.9)

162.5

147.4

134.6