VVIP Pune Call Girls Katraj (7001035870) Pune Escorts Nearby with Complete Sa...

9 January Daily Market Report

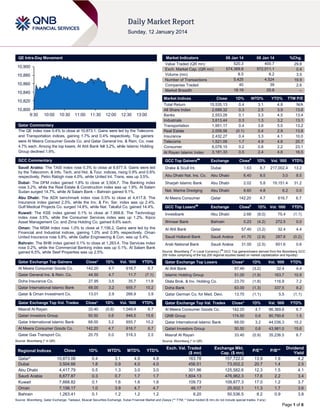

1. QE Intra-Day Movement

Market Indicators

10,900

10,880

10,860

10,840

Market Indices

10,820

10,800

9:30

09 Jan 14

520.3

574,369.8

8.5

5,425

40

18:19

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 0.4% to close at 10,873.1. Gains were led by the Telecoms

and Transportation indices, gaining 1.7% and 0.4% respectively. Top gainers

were Al Meera Consumer Goods Co. and Qatar General Ins. & Rein. Co. rose

4.7% each. Among the top losers, Al Ahli Bank fell 3.2%, while Islamic Holding

Group declined 1.9%.

08 Jan 14

400.7

572,011.1

8.2

4,524

39

25:8

%Chg.

29.8

0.4

3.5

19.9

2.6

–

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

15,535.13

2,689.32

2,553.28

3,613.44

1,951.17

2,009.56

2,432.27

1,521.09

6,078.15

3,181.33

0.4

0.3

0.1

0.3

0.4

(0.1)

0.4

1.7

0.2

0.5

3.1

2.5

3.3

1.3

3.6

0.4

3.3

4.9

0.8

2.4

4.8

3.9

4.5

3.2

5.0

2.9

4.1

4.6

2.2

4.8

N/A

13.6

13.4

13.1

13.2

13.8

10.0

20.7

23.1

16.5

GCC Commentary

GCC Top Gainers##

Exchange

Close#

Saudi Arabia: The TASI index rose 0.3% to close at 8,677.9. Gains were led

by the Telecomm. & Info. Tech. and Hot. & Tour. indices, rising 0.9% and 0.8%

respectively. Petro Rabigh rose 4.0%, while United Int. Trans. was up 3.5%.

Drake & Scull Int.

1D%

Vol. ‘000

YTD%

Dubai

1.63

8.7

217,002.4

13.2

Abu Dhabi Nat. Ins. Co.

Abu Dhabi

6.40

8.5

3.0

8.5

Dubai: The DFM index gained 1.8% to close at 3,504.7. The Banking index

rose 3.2%, while the Real Estate & Construction index was up 1.9%. Al Salam

Sudan surged 14.7%, while Al Salam Bank – Bahrain gained 9.1%.

Sharjah Islamic Bank

Abu Dhabi

2.02

5.8

19,151.4

31.2

Nat. Marine Dredging

Abu Dhabi

8.60

4.8

6.2

0.0

Abu Dhabi: The ADX benchmark index rose 0.5% to close at 4,417.8. The

Insurance index gained 2.5%, while the Inv. & Fin. Ser. index was up 2.4%.

Gulf Medical Projects Co. surged 14.8%, while Nat. Takaful Co. gained 14.4%.

Al Meera Consumer

Qatar

142.20

4.7

616.7

6.7

GCC Top Losers

Exchange

Kuwait: The KSE index gained 0.1% to close at 7,668.8. The Technology

index rose 3.5%, while the Consumer Services index was up 1.2%. Kipco

Asset Management Co. and Zima Holding Co. gained 8.6% each.

Investbank

Abu Dhabi

2.66

(8.0)

75.4

(1.1)

Ithmaar Bank

Bahrain

0.23

(4.2)

272.5

0.0

Oman: The MSM index rose 1.0% to close at 7,156.2. Gains were led by the

Financial and Industrial indices, gaining 1.0% and 0.9% respectively. Oman

United Insurance rose 5.8%, while Galfar Engineering & Con. was up 5.4%.

Al Ahli Bank

Qatar

57.40

(3.2)

32.4

4.4

Saudi Hollandi Bank

Saudi Arabia

41.70

(2.8)

287.6

(0.2)

Arab National Bank

Saudi Arabia

31.00

(2.5)

651.6

0.6

Bahrain: The BHB index gained 0.1% to close at 1,263.4. The Services index

rose 0.2%, while the Commercial Banking index was up 0.1%. Al Salam Bank

gained 6.5%, while Seef Properties was up 2.5%.

Qatar Exchange Top Gainers

Close*

1D%

Vol. ‘000

YTD%

Al Meera Consumer Goods Co.

142.20

4.7

616.7

6.7

Qatar General Ins. & Rein. Co.

44.50

4.7

11.7

(7.1)

Doha Insurance Co.

27.95

3.5

35.7

Qatar International Islamic Bank

68.00

3.2

655.7

Qatar & Oman Investment Co.

13.01

2.9

266.9

3.9

##

#

Close

1D% Vol. ‘000

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers

Vol. ‘000

Close*

1D%

YTD%

Al Ahli Bank

57.40

(3.2)

32.4

4.4

Islamic Holding Group

51.00

(1.9)

163.7

10.9

11.8

Dlala Brok. & Inv. Holding Co.

23.70

(1.8)

116.9

7.2

10.2

Doha Bank

63.00

(1.3)

337.5

8.2

Qatar German Co. for Med. Devi.

13.70

(1.1)

5.5

(1.1)

Qatar Exchange Top Val. Trades

Close*

1D%

Val. ‘000

YTD%

Al Meera Consumer Goods Co.

142.20

4.7

86,369.8

6.7

174.50

0.6

80,790.6

1.5

3.2

44,036.3

10.2

Close*

1D%

Vol. ‘000

YTD%

Masraf Al Rayan

33.40

(0.9)

1,049.4

6.7

Qatari Investors Group

50.50

0.6

846.5

15.6

QNB Group

Qatar International Islamic Bank

68.00

3.2

655.7

10.2

Qatar International Islamic Bank

68.00

Al Meera Consumer Goods Co.

142.20

4.7

616.7

6.7

Qatari Investors Group

50.50

0.6

43,981.0

15.6

20.75

0.0

518.3

2.5

Masraf Al Rayan

33.40

(0.9)

35,236.5

6.7

Qatar Exchange Top Vol. Trades

Qatar Gas Transport Co.

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Source: Bloomberg (* in QR)

Close

1D%

WTD%

MTD%

YTD%

10,873.08

3,504.66

4,417.79

8,677.87

7,668.82

7,156.17

1,263.41

0.4

1.8

0.5

0.3

0.1

1.0

0.1

3.1

0.9

1.3

0.7

1.6

3.9

1.2

4.8

4.0

3.0

1.7

1.6

4.7

1.2

4.8

4.0

3.0

1.7

1.6

4.7

1.2

Exch. Val. Traded

($ mn)

163.78

456.51

301.96

1,804.13

109.73

46.17

6.20

Exchange Mkt.

Cap. ($ mn)

157,722.0

73,002.2

125,582.6

476,962.3

109,877.3

25,502.1

50,536.5

P/E**

P/B**

13.9

20.7

12.3

17.6

17.0

11.3

8.2

1.9

1.4

1.5

2.2

1.2

1.7

0.9

Dividend

Yield

4.2

2.5

4.1

3.4

3.7

3.6

3.8

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 6

2. Qatar Market Commentary

The QE index rose 0.4% to close at 10,873.1. The Telecoms and

Transportation indices led the gains. The index rose on the back

of buying support from non-Qatari shareholders despite selling

pressure from Qatari shareholders.

Overall Activity

Sell %*

Net (QR)

Qatari

53.53%

76.92%

(121,742,559.87)

Non-Qatari

Al Meera Consumer Goods Co. and Qatar General Ins. & Rein.

Co. were the top gainers, rising 4.2% each. Among the top

losers, Al Ahli Bank fell 3.2%, while Islamic Holding Group

declined 1.9%.

Buy %*

46.47%

23.08%

121,742,559.87

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Thursday rose by 3.5% to 8.5mn

from 8.2mn on Wednesday. However, as compared to the 30day moving average of 11.4mn, volume for the day was 24.4%

lower. Masraf Al Rayan and Qatari Investors Group were the

most active stocks, contributing 12.3% and 9.9% to the total

volume respectively.

Earnings and Global Economic Data

Earnings Releases

Company

Market

United Wire Factories Co.

(ASLAK)

Currency

Saudi Arabia

Revenue

(mn) 4Q2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

% Change

YoY

–

–

24.6

-20.4%

25.0

-19.6%

SR

Source: Company data, DFM, ADX, MSM

Global Economic Data

Date

Market

Source

Indicator

Period

01/09

US

IPSOS Public Affairs

RBC Consumer Outlook Index

January

01/09

US

Department of Labor

Initial Jobless Claims

4-January

01/09

US

Department of Labor

Continuing Claims

28-December

01/09

US

Bloomberg

Bloomberg Consumer Comfort

5-January

01/10

US

Bureau of Labor Stat.

Unemployment Rate

01/10

US

Bureau of Labor Stat.

01/10

US

Bureau of Labor Stat.

01/10

US

01/10

01/10

Actual

Consensus

Previous

51.5

–

49.7

330K

335K

345K

2,865K

2,850K

2,815K

-28.4

–

-28.7

December

6.70%

7.00%

7.00%

Average Hourly Earnings MoM

December

0.10%

0.20%

0.20%

Average Hourly Earnings YoY

December

1.80%

1.90%

2.00%

Bureau of Labor Stat.

Underemployment Rate

December

13.10%

–

13.10%

US

US Census Bureau

Wholesale Inventories MoM

November

0.50%

0.40%

1.30%

US

US Census Bureau

Wholesale Trade Sales MoM

November

1.00%

0.70%

1.10%

01/10

US

Bloomberg

IBD/TIPP Economic Optimism

January

45.2

46

43.1

01/09

EU

European Commission

Services Confidence

December

0.2

-0.5

-0.9

01/09

EU

European Commission

Business Climate Indicator

December

0.27

0.22

0.31

01/09

EU

European Commission

Economic Confidence

December

100

99.1

98.4

01/09

EU

European Commission

Industrial Confidence

December

-3.4

-3

-3.9

01/09

EU

European Commission

Consumer Confidence

December

-13.6

-13.6

-15.4

01/09

EU

ECB

ECB Announces Interest Rates

9-January

0.25%

0.25%

0.25%

01/09

France

Ministry of the Economy

Trade Balance

November

-5680M

-4600M

-4826M

01/10

France

INSEE

Industrial Production MoM

November

1.30%

0.40%

-0.50%

01/10

France

INSEE

Industrial Production YoY

November

1.50%

0.90%

-0.30%

01/10

France

INSEE

Manufacturing Production MoM

November

0.20%

0.20%

0.30%

01/10

France

INSEE

Manufacturing Production YoY

November

1.60%

1.50%

0.50%

01/09

Germany

Bundesbank

Industrial Production SA MoM

November

1.90%

1.50%

-1.20%

01/09

Germany

BAFA

Industrial Production WDA YoY

November

3.50%

3.00%

1.10%

01/09

UK

ONS

Trade Balance

November

-£3238

-£2300

-£3496

01/09

UK

Bank of England

Bank of England Bank Rate

9-January

0.50%

0.50%

0.50%

01/10

UK

ONS

Industrial Production MoM

November

0.00%

0.40%

0.30%

01/10

UK

ONS

Industrial Production YoY

November

2.50%

3.00%

3.20%

01/10

UK

ONS

Manufacturing Production MoM

November

0.00%

0.40%

0.20%

01/10

UK

ONS

Manufacturing Production YoY

November

2.80%

3.30%

2.60%

01/10

UK

ONS

Construction Output SA MoM

November

-4.00%

0.80%

2.00%

01/10

UK

ONS

Construction Output SA YoY

November

2.20%

7.50%

5.10%

01/10

UK

NIESR

NIESR GDP Estimate

December

0.7%

–

0.8%

01/10

Spain

INE

Industrial Output WDA YoY

November

2.70%

2.20%

-1.40%

01/09

China

Nati. Bureau of Statistics

CPI YoY

December

2.50%

2.70%

3.00%

Page 2 of 6

3. 01/09

China

Nati. Bureau of Statistics

PPI YoY

December

-1.40%

-1.30%

-1.40%

01/10

China

Nati. Bureau of Statistics

Trade Balance

December

$25.64B

$32.15B

$33.80B

01/10

China

Nati. Bureau of Statistics

Exports YoY

December

4.30%

5.00%

12.70%

01/10

China

Nati. Bureau of Statistics

Imports YoY

December

8.30%

5.00%

5.30%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QNB Group: $30bn Qatar spend, mega GCC region projects

to drive Gulf growth in 2014 – According to a report by QNB

Group, Qatar’s project spending estimated at $30bn this year

and large-scale projects across the GCC will drive the region’s

growth in 2014. In the short term, the GCC region will drive the

MENA region’s growth, mainly through heavy spending on

infrastructure. In the GCC region, many countries including

Saudi Arabia and Kuwait have huge project spending outlay this

year. Dubai’s successful bid for the World Expo 2020 and a

number of new real estate developments will boost project

spending in the UAE. The Saudi government alone is spending

in excess of $50bn on infrastructure projects through its budget,

which excludes significant project spending by the private sector

and state-owned companies. The report also said greater

integration into the global economy of the MENA region (exGCC region) through increased trade openness and enhanced

competitiveness could raise long-term growth prospects. QNB

Group estimates that real GDP growth in the GCC region stood

at 3.7% in 2013, compared with 1.2% in the rest of MENA. This

is relatively sluggish compared with the historical average

MENA growth of around 5% or higher. (Gulf-Times.com)

Kahramaa studying N-power plant feasibility – Qatar’s

Minister of Energy & Industry HE Dr. Mohammed bin Saleh al

Sada said Qatar General Electricity & Water Corporation

(Kahramaa) is finalizing the preliminary studies to study the

feasibility of establishing a nuclear power plant. He said Qatar is

considering using nuclear energy in electricity production in

collaboration with other GCC countries. Al Sada also hoped that

Qatar’s goal of reducing the rate of electricity consumption per

capita by 20% and water by 35% over the next five years will be

met. (Qatar Tribune)

RasGas plans to convert more vessels to LNG – With the

International Maritime Organization (IMO) deciding to regulate

maritime transport’s emissions from January 2015, RasGas is

planning to convert over a dozen of its diesel-powered energy

carriers into LNG-powered vessels. The IMO’s regulations to cut

the emission rate of ships will force thousands of ship owners to

convert their vessels into cleaner LNG-powered engines.

RasGas has a fleet of 27 LNG carriers, which include 14

conventional carriers, 12 Q-Flex and one Q-Max carrier. The

conventional carriers are already powered by steam plants.

However, using new technology, RasGas is planning to convert

its Q-Flex and Q-Max vessels. Currently, these 13 vessels are

being powered by slow-speed diesel engines, which can use

only heavy fuel or marine gas oil. The idea is to convert them to

be able to use gas, directly vaporized from LNG, as fuel.

(Peninsula Qatar)

Ashghal to align 7 expressways under QR45bn road

projects – The Public Works Authority (Ashghal) is set to sign

various contracts to launch seven major expressways, carry out

road development and repair work and undertake sewage

projects worth QR45bn expected to be completed over the next

five to seven years. The expressway projects involve 900

kilometers of roads, subways, flyovers and interchanges, which

is part of the road infrastructure scheme connecting places in

Doha and other parts of the country. These projects involve

development and repair of some major roads, along with

building 240 major interchanges, which would convert

conventional traffic lights into multi-level interchanges with

tunnels and flyovers. As for the sewage plan, 221 projects are to

be executed over the next 5-7 years at a cost of QR50bn.

(Peninsula Qatar)

QIGD postpones its EGM to January 12 – Qatari Investors

Group (QIGD) announced that the necessary quorum for the

EGM on January 8, 2014, was not met and therefore, it will hold

another EGM on January 12, 2014. (QE)

International

Fischer nominated for Federal Reserve’s vice chairman –

The Obama administration said that the former head of the Bank

of Israel, Stanley Fischer, will be nominated to serve as the Vice

Chairman of the US Federal Reserve. According to a statement

by the White House, Fischer would replace Janet Yellen, who

was promoted to the chairmanship of the US central bank. Lael

Brainard – formerly the US Treasury Department’s international

official – will be on the board, while Jerome Powell is nominated

for a second term. (Bloomberg)

Fed soothes US debt burden to $77.7bn in 2013 – According

to the data published by the Federal Reserve, Fed pumped

$77.7bn into the US Treasury last year, in part by returning

interest payments made by the government on bonds held by

the central bank. The Fed's balance sheet has ballooned over

the last four years to nearly $4tn as it bought debt securities to

lower interest rates and spark a faster economic recovery.

(Bloomberg)

Regulators to ease bank rule to help economic recovery –

According to sources, global regulators will make it easier for

lenders to feed credit to the economy by relaxing a new rule

designed to limit risk on banks balance sheets. The rule is

among the final elements of a global accord on bank capital,

known as Basel III, which forms the world's core regulatory

response to the 2007-09 financial crisis that saw

undercapitalized lenders being rescued by taxpayers. The

Central bankers from the Group of 20 leading economies and

other countries will meet in Basel, Switzerland to endorse the

final version of the so-called leverage ratio that banks will have

to comply with from January 2018. (Bloomberg)

ECB toughens talk on inflation, money market rates – The

European Central Bank (ECB) forcefully underlined its

determination to take further action should the Eurozone’s

inflation risk turns into deflation or rising money market rates

threaten the bloc's fragile recovery. After leaving its interest

rates at a record low on January 9th, the ECB toughened its

pledge to keep its policy loose, while firmly reiterating its

expectation for rates to remain at current levels for an extended

period. ECB’s President Mario Draghi said that the Governing

Council strongly emphasized that it will maintain an

accommodative stance of the monetary policy for as long as

necessary. (Reuters)

China’s 2013 trade crosses $4tn – China’s annual trade

passed the $4tn mark for the first time in 2013. The General

Administration of Customs (GAC) announced that exports from

the country rose 7.9% to $2.21tn, while imports increased 7.3%

Page 3 of 6

4. to $1.95tn. The trade surplus stood at $259.75bn, up 12.8%

from 2012. Total trade came to $4.16tn, showing an increase of

7.6%. GAC’s spokesman Zheng Yuesheng said that it is likely

that China has already overtaken the US to become the world’s

largest trading country in 2013 for the first time. The traditional

leading markets of the EU, US and Japan accounted for 33.5%

of China’s trade, down 1.7 percentage points, suggesting that

emerging markets’ share of business was rising. (Peninsula

Qatar)

Regional

Oil Movements: OPEC to cut exports to lowest in four

months – According to Oil Movements, the Organization of

Petroleum Exporting Countries (OPEC) will reduce its crude

shipments to the lowest level since September 2013 as

refineries trim imports before conducting maintenance during

spring. OPEC will reduce shipments by 390,000 barrels a day,

or 1.6%, to 23.71mn barrels in the four weeks to January 25.

That compares poorly with 24.1mn barrels in the period up to

December 28. These figures exclude two of OPEC’s 12

members: Angola and Ecuador.

IATA: Middle East carriers post record air freight growth –

According to the International Air Transport Association (IATA),

better demand in Europe and solid trade growth with the Gulf

region helped the Middle Eastern carriers to report the strongest

annual freight demand growth of 16.5% in November 2013. In

comparison to the Middle Eastern carriers, the European

carriers witnessed 8% growth in freight demand, followed by

Asia-Pacific (4.9%) and North America (2.5%), as against the

global average of 6.1%. Meanwhile, African and Latin American

airlines saw a contraction of 1.2% and 0.1% respectively. IATA

said that carriers in the Middle East have benefited from

improvements in advanced economies, including better demand

in Europe, as well as solid economic and trade growth in the

Gulf area. (Gulf-Times.com)

ANB reports SR536.6mn net profit in 4Q2013 – The Arab

National Bank (ANB) has reported a net profit of SR536.6mn in

4Q2013, reflecting a decline of 8.9% QoQ (+26.3% YoY). EPS

stood at SR2.97 for the period ended on December 31, 2013 as

compared to SR2.79 in December 31, 2012. Total assets at the

end of December 2013 stood at SR137.9bn as compared to

SR136.6bn in December 2012. Loans & advances rose by 2.5%

YTD to SR 88.5bn, while customer deposits were down by 1.1%

YTD to SR106.4bn. (Tadawul)

Bank Albilad reports SR213.7mn net profit in 4Q2013 – Bank

Albilad has reported a net profit of SR213.7mn in 4Q2013,

reflecting a growth of 8.4% QoQ (+36.4% YoY). EPS stood at

SR1.82 for the period ended on December 2013 as compared to

SR2.35 in December 31, 2012. Total assets at the end of

December 2013 stood at SR36.3bn as compared to SR29.8bn

in December 2012. Loans & advances rose by 28.3% YTD to

SR23.4bn, while customer deposits were up by 22.6% YTD to

SR29.1bn. (Tadawul)

Saudi Aramco to buy $2bn stake in S-Oil – According to

sources, Saudi Aramco will buy a $2bn stake in South Korea’s

S-Oil Corporation. Saudi Aramco will buy almost all of Hanjin

Energy Co’s stake in S-Oil. According to data compiled by

Bloomberg Saudi Aramco currently owns 35% of S-Oil, followed

by Hanjin’s 28.4%. Meanwhile, Saudi Aramco will provide 100%

of its crude cargoes sold under long-term contracts. (GulfTimes.com)

Kingdom plans to sell shares of Satorp, Sadara in IPO –

Saudi Petroleum & Mineral Resources Minister Ali Al Naimi said

that the government plans to sell shares of Saudi Aramco Total

Refining & Petrochemical Company (Satorp) and Sadara

Chemical Company to citizens at cost rate in an IPO. Satrop – a

JV between Saudi Aramco and France’s Total – involves a total

capital investment of SR52.87bn. (GulfBase.com)

Saudi oil output up in December – According to industry

sources, Saudi Arabia produced 9.819mn bpd of crude oil in

December 2013, up from 9.745mn bpd in November 2013. The

Kingdom also raised its supply to the market to 9.897mn bpd in

December from 9.448mn bpd in November. (GulfBase.com)

DSFH plans hospital, university project in Dubai – Dr.

Soliman Fakeeh Hospital (DSFH) is planning to build a hospital

and medical university project worth AED1bn in Dubai Silicon

Oasis. Based in Jeddah, DSFH is a leading private hospital in

the Middle East with a total capacity of 600 beds. The new

hospital is to be completed by 2017, while the medical university

will be ready by 2019, which are expected to offer 4,000 new

jobs. An agreement regarding this was signed by DSFH’s

President & Chairman Mazen Fakeeh and Dubai Silicon Oasis

Authority’s Vice Chairman & CEO Mohammed Al Zarooni.

(GulfBase.com)

Sahara Petchem’s unit to restart operations – Al Waha

Petrochemicals Company, an affiliate of Sahara Petrochemical

Company has announced that the scheduled maintenance of Al

Waha’s plant has been completed and it has started the

necessary steps to restart the operation and plant units.

(Tadawul)

SAFCO announces correction to cash dividend distribution

for 2H2013 – The Saudi Arabia Fertilizers Company (SAFCO)

has announced a correction related to the distribution of cash

dividends to its shareholders for 2H2013. The eligibility of

dividends shall be for the shareholders registered in the

registers of the Securities Depository Center (Tadawul) as on

March 24, 2014. (Tadawul)

Almarai acquires IPNC – Almarai Company has acquired the

entire share capital of the International Pediatric Nutrition

Company (IPNC) from its JV partner Mead Johnson Nutrition.

(Tadawul)

Arabian Pipes signs revised contract with Hanwha E&C –

Arabian Pipes Company has signed a revision of a contract it

had earlier made with Hanwha Engineering & Construction

Company (Hanwha E&C). This revised contract increases the

total amount from SR49mn to SR61mn due to a rise in contract

quantity supplied from Jubail factory. It also extends the contract

delivery period to be during 3Q2014 and 4Q2014 and the

financial impact is expected to be visible after that. (Tadawul)

Bahri receives new 26,000 DWT general cargo vessel – The

National Shipping Company of Saudi Arabia (Bahri) has

received the delivery of a new 26,000 DWT general cargo

vessel. The ship, named Bahri Jeddah was built by Hyundai

MIPO in South Korea. This is the fifth vessel delivered from a

batch of six vessels that were contracted with this shipyard in

2011 for a total value of SR1,543mn. The last general cargo

vessel remaining under construction at Hyundai MIPO is

expected to be delivered during 1H2014. The financial impact of

the delivered vessel will materialize during 1Q2014. (Tadawul)

Saudi CMA approves SAIB’s capital increase through

bonus shares issue – The Saudi Capital Market Authority

(Saudi CMA) has approved the Saudi Investment Bank’s (SAIB)

request to increase its capital from SR5.5bn to SR6bn through

issuance of one bonus share for every 11 existing shares. This

capital increase will be paid by transferring an amount of

SR500mn from its retained earnings account to the bank’s

capital. Consequently, SAIB is increasing its outstanding shares

Page 4 of 6

5. from 550mn shares to 600mn shares. The bonus shares

eligibility is limited to those shareholders who are registered in

the shareholders registry at the close of trading on the day of the

extraordinary general assembly, which will be determined later

by the bank's board, and should be held within six months from

the approval date. (Tadawul)

Aggregate money supply in UAE up 3.8% to AED62.8bn in

October 2013 – The UAE Central Bank announced that the

money supply aggregate M0 increased by 3.8% from

AED60.5bn at the end of September 2013 to AED62.8bn at the

end of October 2013. The money supply aggregate M1

increased by 2% from AED354.4bn in September to

AED361.5bn in October. Similarly, the money supply aggregate

M2, increased by 5.1% from AED955.0bn in September to

AED1,003.5bn in October. Meanwhile, the money supply

aggregate M3 increased by 2% from AED1,199.6bn in

September to AED1,223.1bn in October. Total bank deposits

increased by 1.2% during October 2013 to reach AED1,285.1bn,

as a result of an increase in resident deposits by 2%.

Meanwhile, total bank loans and advances decreased by 1.7%

to reach AED1,157.8bn, while total bank assets increased by

4.1% to reach AED1,986.6bn, at the end of October 2013.

(GulfBase.com)

GCAA signs ASA deal with India – The UAE’s General Civil

Aviation Authority (GCAA), signed the Air Services Agreement

(ASA) with the Government of India, which allows scheduled

flights of any type of service (passenger or cargo) between the

two countries. The agreement was signed by the GCAA’s

Director-General Saif Mohammed Al Suwaidi and the Ministry of

Civil Aviation of India’s Joint Secretary Dr. Prabhat Kumar. Al

Suwaidi said that GCAA continues to explore new horizons for

mutual air transport agreements to promote the UAE’s local

carriers and boost the local economy. Such ASA deals are in

line with the directions of the UAE Government to enhance

international cooperation through air transport. (GulfBase.com)

DFM to be closed on January 12 – The Dubai Financial

Market (DFM) will be closed on January 12, 2014 on the

occasion of the Prophet’s birthday. The trading will resume on

January 13, 2014. (DFM)

Dubai rentals surge, downtown rent up over 100% – Rentals

in Dubai increased significantly during 2013 as downtown rent

jumped by more than 100%, while other locations also

witnessed 30% rise. With the iconic Burj Khalifa and the world’s

largest shopping mall as its centerpiece, the residences in the

downtown area ranked among Dubai’s most sought after

locations during 2013. Evidently, the Dubai Land Department

(DLD) is planning to limit rent hikes when tenants change and

also update its rental price index. According to DLD’s General

Director Sultan Bin Mejren, while there are caps on increases for

existing occupiers, Dubai currently has no controls on increases

for new tenants. (GulfBase.com)

Dubai plans new rules to control properties speculation –

The Dubai Land Department (DLD) General Director Sultan Bin

Mejren said that Dubai is planning new rules to control

speculation on properties sold before they are built after home

prices climbed by more than 30% last year. He said that the real

estate authority plans to complete a review of off-plan

transactions in 1Q2014 and may introduce new regulations in

2Q2014. Mejren said that the home prices this year may rise 3540%. (GulfBase.com)

travelers wishing to visit destinations such as Mauritius,

Bangkok, Shanghai and Sydney, the chance to experience a

seamless Emirates A380 experience connecting through

Emirates’ Dubai hub. (GulfBase.com)

Dubai Group appoints new CEO – Dubai Group has appointed

Ahmed Al-Qassim as its chief executive, who previously worked

at its biggest creditor. Qassim was a director of investment

banking at Emirates NBD since February 2013, and has also

held various roles at General Electric and Mubadala

Development Company. (GulfBase.com)

Kuwait’s inflation drops to 2.6% in November – According to

the report released by the National Bank of Kuwait, the

consumer price index (CPI) edged down to 2.6% YoY in

November, from 2.7% in October. This small move masked

some notable changes within the sub-components: another

sharp fall in food price inflation was almost offset by a rise in

core price pressures. It is expected that core pressures to

continue to edge higher. However, the overall inflation rate is still

forecast to average at a modest 3.0% throughout 2014, up from

2.6% in 2013. The report noted that food price inflation fell to

2.4% YoY from 3.5% in October, its sixth consecutive monthly

decline. Given the component's large weight in the CPI (18%),

this move subtracted some 0.2% points from the overall inflation

rate in November. (Bloomberg)

Bank Dhofar appoints HR Head – Bank Dhofar has appointed

Nasser bin Said Al Bahantah as Deputy General Manager –

Head of Human Resources. Nasser has a bachelor’s degree in

business administration and a Global Executive Graduate

Certificate in human resources leadership. Nasser has 22 years

of experience as a HR professional. (MSM)

Bahrain’s LT/LCR IDR credit rated BBB/BBB+ by Fitch;

outlook stable – Fitch has affirmed Bahrain’s long-term (LT)

foreign currency Issuer Default Rating (IDR) at “BBB” and local

currency IDR at “BBB+” with a Stable outlook. The ratings on

Bahrain's senior unsecured foreign and local currency bonds

have also been affirmed at “BBB” and “BBB+”, respectively.

Fitch has simultaneously affirmed Bahrain's Country Ceiling at

“BBB+” and short-term foreign currency IDR at “F3”. Fitch’s

affirmation and the stable outlook indicate that Bahrain's

external position is stronger than its “BBB” rated peers. A

current account surplus of around 10% of GDP is estimated for

2013, which will be the 10th consecutive year of surplus.

(Reuters)

FEB inks $34mn facility with Dutch firm – Bahrain-based First

Energy Bank (FEB) has signed a $34mn Murabaha facility with

Kore Coal Finance, a Dutch-based subsidiary of Sapinda

Holding. The financing will assist Sapinda in enhancing its

investments in an internationally operating resource company,

which owns coal mining assets in South Africa. This Islamic

facility supplements the recently concluded conventional profit

participation note of EUR55mn raised by Kore Coal Finance with

a similar objective. The Murabaha facility has been structured on

the basis of an attractive return and will be repaid by October

2016. FEB’s Head of Investment Management Tarun Puri said

that the bank seeks to further diversify into asset classes that

can generate similar sustained income streams. The bank has

an authorized share capital of $2bn and a paid-up capital of

$1bn. (GulfBase.com)

Emirates launches daily A380 service to Switzerland –

Emirates Airline has launched A380 service to Zurich in

Switzerland, bringing the number of destinations it serves with

its popular A380 to 25. The new A380 service to Zurich provides

Page 5 of 6

6. Rebased Performance

Daily Index Performance

170.0

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

1.6%

1.2%

0.8%

0.4%

1.0%

0.3%

QE Index

Close

1D%

WTD%

YTD%

16,437.05

(0.0)

(0.2)

(0.8)

S&P 500

1,842.37

0.2

0.6

(0.3)

(3.2)

NASDAQ 100

4,174.67

0.4

1.0

(0.0)

(8.9)

(9.0)

STOXX 600

329.95

0.5

0.7

0.5

(0.2)

3.9

1.2

DAX

9,473.24

0.5

0.4

(0.8)

1.4

0.5

1.7

FTSE 100

6,739.94

0.7

0.1

(0.1)

4,250.60

0.6

0.1

(1.1)

15,912.06

0.2

(2.3)

(2.3)

Oct-12

S&P Pan Arab

May-13

Dec-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

1,248.45

1.7

0.9

3.5

DJ Industrial

20.16

2.9

0.0

3.5

107.25

0.8

0.3

3.95

(4.5)

127.75

138.88

1.37

0.5

0.6

(0.5)

CAC 40

104.18

(0.6)

(0.6)

(1.1)

Nikkei

GBP

1.65

0.0

0.4

(0.4)

MSCI EM

CHF

1.11

0.5

0.3

(1.1)

SHANGHAI SE Composite

AUD

0.90

1.1

0.6

0.9

USD Index

80.66

(0.4)

(0.2)

RUB

33.06

(0.5)

(0.4)

BRL

0.42

1.0

0.6

(0.2)

Yen

Dubai

Mar-12

0.1%

Abu Dhabi

Aug-11

Qatar

Jan-11

0.1%

Oman

0.0%

0.5%

0.4%

Bahrain

124.9

Kuwait

137.6

1.8%

Saudi Arabia

Jun-10

2.0%

156.2

970.15

0.7

(1.0)

(3.2)

2,013.30

(0.7)

(3.4)

(4.9)

HANG SENG

22,846.25

0.3

0.1

(2.0)

0.8

BSE SENSEX

20,758.49

0.2

(0.4)

(1.9)

0.6

Bovespa

49,696.45

0.8

(2.5)

(3.5)

1,395.91

0.5

(3.2)

(3.2)

Source: Bloomberg

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6