NO1 Certified Amil Baba In Lahore Kala Jadu In Lahore Best Amil In Lahore Ami...

24 September Daily market report

1. Page 1 of 6

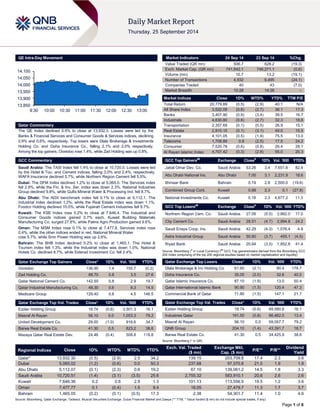

QE Intra-Day Movement

Qatar Commentary

The QE Index declined 0.5% to close at 13,932.3. Losses were led by the Banks & Financial Services and Consumer Goods & Services indices, declining 0.9% and 0.6%, respectively. Top losers were Dlala Brokerage & Investments Holding Co. and Doha Insurance Co., falling 2.1% and 2.0% respectively. Among the top gainers, Ooredoo rose 1.4%, while Zad Holding was up 0.8%.

GCC Commentary

Saudi Arabia: The TASI Index fell 1.4% to close at 10,720.5. Losses were led by the Hotel & Tou. and Cement indices, falling 3.0% and 2.4%, respectively. WAFA Insurance declined 5.7%, while Northern Region Cement fell 5.5%.

Dubai: The DFM Index declined 1.2% to close at 5,065.0. The Services index fell 2.9%, while the Fin. & Inv. Ser. index was down 2.3%. National Industries Group declined 9.8%, while Gulfa Mineral Water & Processing Ind. fell 8.7%.

Abu Dhabi: The ADX benchmark index fell 0.1% to close at 5,112.1. The Industrial index declined 1.2%, while the Real Estate index was down 1.1%. Foodco Holding declined 10.0%, while Fujairah Cement Industries fell 9.7%.

Kuwait: The KSE Index rose 0.2% to close at 7,646.4. The Industrial and Consumer Goods indices gained 0.7% each. Kuwait Building Materials Manufacturing Co. surged 27.8%, while Palms Agro Production gained 9.6%.

Oman: The MSM Index rose 0.1% to close at 7,477.8. Services index rose 0.4%, while the other indices ended in red. National Mineral Water rose 5.7%, while Smn Power Holding was up 2.6%.

Bahrain: The BHB Index declined 0.2% to close at 1,465.1. The Hotel & Tourism index fell 1.3%, while the Industrial index was down 1.0%. National Hotels Co. declined 8.7%, while Esterad Investment Co. fell 2.4%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Ooredoo

136.90

1.4

155.7

(0.2) Zad Holding Co. 88.70 0.8 3.5 27.6 Qatar National Cement Co. 142.50 0.8 2.9 19.7 Qatar Industrial Manufacturing Co. 48.30 0.6 8.3 14.5 Medicare Group 129.40 0.6 4.5 146.5

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group

19.74

(0.6)

3,501.3

16.1 Masraf Al Rayan 56.10 0.0 1,053.3 79.2

United Development Co.

29.00

(1.0)

916.6

34.7 Barwa Real Estate Co. 41.30 0.5 823.2 38.6

Mazaya Qatar Real Estate Dev.

24.46

(0.4)

508.8

118.8

Market Indicators 24 Sep 14 23 Sep 14 %Chg.

Value Traded (QR mn)

506.7

628.2

(19.3) Exch. Market Cap. (QR mn) 741,842.1 746,271.1 (0.6)

Volume (mn)

10.7

13.2

(19.1) Number of Transactions 4,932 6,495 (24.1)

Companies Traded

40

43

(7.0) Market Breadth 10:28 14:26 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return

20,779.89

(0.5)

(2.9)

40.1

N/A All Share Index 3,522.09 (0.6) (2.7) 36.1 17.3

Banks

3,407.90

(0.9)

(3.4)

39.5

16.7 Industrials 4,630.80 (0.6) (2.7) 32.3 18.8

Transportation

2,357.69

(0.1)

(0.5)

26.9

15.1 Real Estate 2,910.15 (0.1) (3.1) 49.0 15.5

Insurance

4,101.05

(0.5)

(1.9)

75.5

13.0 Telecoms 1,708.89 0.8 (2.5) 17.5 24.2

Consumer

7,520.78

(0.6)

(0.8)

26.4

28.1 Al Rayan Islamic Index 4,707.42 (0.3) (2.8) 55.0 20.3

GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD%

Jabal Omar Dev. Co.

Saudi Arabia

53.26

3.4

7,551.6

82.4 Abu Dhabi National Ins. Abu Dhabi 7.00 3.1 2,231.9 18.6

Ithmaar Bank

Bahrain

0.19

2.8

2,500.0

(19.6) Combined Group Cont. Kuwait 0.88 2.3 0.1 (27.8)

National Investments Co.

Kuwait

0.18

2.3

4,677.2

11.3

GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD%

Northern Region Cem. Co.

Saudi Arabia

27.09

(5.5)

3,862.0

17.0 City Cement Co. Saudi Arabia 28.51 (4.7) 2,994.8 24.2

Saudi Enaya Coop. Ins.

Saudi Arabia

42.29

(4.3)

1,076.4

4.9 Astra Industrial Group Saudi Arabia 50.60 (3.7) 455.1 (4.5)

Riyad Bank

Saudi Arabia

20.64

(3.5)

1,852.8

41.4

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Dlala Brokerage & Inv Holding Co.

61.60

(2.1)

90.4

178.7 Doha Insurance Co. 35.00 (2.0) 32.6 40.0

Qatar Islamic Insurance Co.

87.10

(1.9)

13.0

50.4 Qatar International Islamic Bank 90.90 (1.5) 120.4 47.3

Commercial Bank of Qatar

71.80

(1.5)

147.1

21.7

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Ezdan Holding Group

19.74

(0.6)

69,580.8

16.1 Industries Qatar 191.50 (0.8) 66,462.5 13.4

Masraf Al Rayan

56.10

0.0

59,057.7

79.2 QNB Group 204.10 (1.4) 43,391.7 18.7

Barwa Real Estate Co.

41.30

0.5

34,425.9

38.6

Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield

Qatar*

13,932.30

(0.5)

(2.9)

2.5

34.2

139.15

203,709.8

17.4

2.3

3.6 Dubai 5,065.02 (1.2) (0.6) 0.0 50.3 237.68 97,570.8 21.0 1.9 1.9

Abu Dhabi

5,112.07

(0.1)

(2.3)

0.6

19.2

67.10

139,061.2

14.5

1.8

3.3 Saudi Arabia 10,720.51 (1.4) (3.1) (3.5) 25.6 2,755.32 583,910.1 20.6 2.6 2.6

Kuwait

7,646.36

0.2

0.6

2.9

1.3

101.13

113,556.9

19.5

1.2

3.6 Oman 7,477.77 0.1 (0.4) 1.5 9.4 18.05 27,479.7 11.3 1.7 3.7

Bahrain

1,465.05

(0.2)

(0.1)

(0.5)

17.3

2.38

54,301.7

11.4

1.0

4.6

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

13,85013,90013,95014,00014,05014,1009:3010:0010:3011:0011:3012:0012:3013:00

2. Page 2 of 6

Qatar Market Commentary

The QE Index declined 0.5% to close at 13,932.3. The Banks & Fin. Serv. and Consumer Goods & Serv. indices led the losses. The index fell on the back of selling pressure from non-Qatari shareholders despite buying support from Qatari shareholders.

Dlala Brokerage & Investments Holding Co. and Doha Insurance Co. were the top losers, falling 2.1% and 2.0%, respectively. Among the top gainers, Ooredoo rose 1.4%, while Zad Holding Co. was up 0.8%.

Volume of shares traded on Wednesday fell by 19.1% to 10.7mn from 13.2mn on Tuesday. Further, as compared to the 30-day moving average of 17.2mn, volume for the day was 37.6% lower. Ezdan Holding Group and Masraf Al Rayan were the most active stocks, contributing 32.7% and 9.8% to the total volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Global Economic Data

Global Economic Data Date Market Source Indicator Period Actual Consensus Previous

09/24

US

MBA

MBA Mortgage Applications

19-September

-4.10%

–

7.90% 09/24 US US Census Bureau New Home Sales August 504K 430K 427K

09/24

US

US Census Bureau

New Home Sales MoM

August

18.00%

4.40%

1.90% 09/24 France French Labor Office Total Jobseekers August 3,413.3K 3,441.0K 3,424.4K

09/24

France

French Labor Office

Jobseekers Net Change

August

-11.1

16.5

26.1 09/24 Germany IFO IFO Business Climate September 104.7 105.8 106.3

09/24

Germany

IFO

IFO Current Assessment

September

110.5

110.2

111.1 09/24 Germany IFO IFO Expectations September 99.3 101.2 101.7

09/24

UK

LBMA Silver Price

London Silver Market Fixing

24-September

17.8

–

– 09/24 UK London Gold Market Fix. London Gold Market PM Fix 24-September 1,217.3 – 1,222.0

09/24

Italy

ISTAT

Consumer Confidence Index

September

102.0

101.0

101.9

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted

News

Qatar

MDPS: Monthly Industrial PPI stands at 167.2 in July 2014, drops 6.3% YoY – Qatar’s Ministry of Development Planning & Statistics (MDPS) has released the monthly Producer Price Index (PPI) of the Industrial sector which covers Mining, Electricity & Water and Manufacturing activities for July 2014. The PPI for July 2014 stands at 167.2, which showed a decrease of 2.4% over the PPI of June 2014, and a YoY decrease of 6.3%. The mining group PPI (with a weight of 77%) showed a MoM decline of 3.2% as crude petroleum and natural gas also fell by 3.2%. The manufacturing group PPI (with a weight of 21%) showed a MoM rise of 1.3%. The MoM increase is explained by the combined effect of increasing prices seen in dairy products (by 3.0%), refined petroleum products (2.1%), cement & other non-metallic products (0.6%), beverages (0.4%) and basic chemicals (0.1%). On the other hand, decreasing prices were seen in grain mill and other products (0.9%). The electricity & water group PPI (representing about 2.0% weight) fell in July 2014 (-0.4% MoM). On a YoY basis, the mining group PPI showed a drop of 6.4%, primarily due to the price decrease seen in crude petroleum and natural gas group by the same percentage. The manufacturing group PPI showed a YoY decline of 6.0% in July 2014. The major groups which explain this price fall include: refined petroleum products (-9.2% YoY), basic metals (-2.9% YoY), beverages (-2.2% YoY) and basic chemicals (-0.1% YoY). However, price rises are noticed in dairy products (+3.8% YoY), cement & other non-metallic products (+2.4% YoY) and grain mill and other products (+0.2% YoY). The electricity & water PPI showed a decrease of 4.6% YoY,

resulting from the effect of price fall seen in water (-4.9% YoY) and electricity energy (-4.4% YoY). (MDPS)

QNBK to announce 3Q2014 results on October 12, 2014 – QNB Group (QNBK) will disclose its 3Q2014 financial statements on October 12, 2014. (QE)

QEWS to disclose results on October 12 – Qatar Electricity & Water (QEWS) announces its intent to disclose 3Q2014 financial statements on October 12, 2014. (QE)

DHBK to announce 3Q2014 results on October 21, 2014 – Doha Bank (DHBK) will disclose its 3Q2014 financial statements on October 21, 2014. (QE)

QATI to announce results on October 21 – Qatar Insurance Company (QATI) announces its intent to disclose 3Q2014 financial statements on October 21, 2014. (QE)

Cabinet ratifies draft law on marine vessels – The cabinet chaired by HE the Prime Minister and the Minister of Interior Sheikh Abdullah bin Nasser bin Khalifa Al-Thani ratified a draft law on marine vessels featuring terms related to the prohibition of sailing unregistered vessels, registration conditions, registration application procedures, validity of registration certificates, setting entry & exit points of marine vessels, and setting regulations & conditions of granting steering licenses, lease procedures and ownership transfer for the vessels. The cabinet also endorsed the cabinet’s decision to amend some provisions of decision No. 30 of 2013 on the formation of a tender commission at the Ministry of Interior. In addition, the cabinet ratified the minister of transport’s draft decision to oblige Overall Activity Buy %* Sell %* Net (QR)

Qatari

66.94%

58.20%

44,307,741.95 Non-Qatari 33.06% 41.80% (44,307,741.95)

3. Page 3 of 6

ships and floating facilities to install Automatic Identification System (AIS) and VHF set. According to the draft decision, the VHF system is a high frequency radio that operates within the system of marine rescue, safety and emergency. (Peninsula Qatar)

Qatar Development Bank to get Al Forjan income – According to a proposal approved by the State Cabinet, the income from Al Forjan Markets project will go to the state-owned Qatar Development Bank (QDB). Al Forjan Markets are being set up by the government in different remote parts of the country to enable the residents to access basic commodities of daily needs locally and not rush to Doha and other towns looking for them. (Peninsula Qatar)

CME to create new firm with Salam Technology – Canon Middle East (CME) announced its intent to establish a new company in Qatar in cooperation with Salam Technology, its existing imaging solutions distribution partner. The new company will strengthen CME's presence in the region while demonstrating its commitment to operating closer to customers and meet customers’ demands through diversifying its business offering. Once established, the new company will provide Qatari customers an opportunity to receive direct advice on products and services from Canon professionals. CME is keen to strengthen its presence in this strategically important region in order to become market leader in imaging solutions in the Middle East. (Bloomberg)

International

US new home sales at six-year high, but outlook challenging – Sales of new single-family homes in the US surged in August 2014 to their highest level in more than six years, a sign the housing recovery remains on course. The recovery, however, is likely to remain gradual against a backdrop of relatively high unemployment and sluggish wage growth, which are sidelining first-time buyers and keeping many young adults from seeking their own accommodation. The US Commerce Department said new home sales jumped 18% to a seasonally adjusted annual rate of 504,000 units, a second straight monthly gain that took them to the highest level since May 2008. Although new home sales account for only about 9% of the market, the increase helped allay fears of renewed weakness after a surprise decline in home re-sales last month. (Reuters)

Draghi: ECB to keep loose policy for long time – The European Central Bank (ECB) President Mario Draghi said the bank will maintain its monetary policy loose for as long as it takes to push up the ultra-low inflation in the Eurozone closer to the 2% level. Draghi said the ECB would do all in its power to stimulate growth, but reaffirmed that Eurozone countries needed to make their economies fitter. Referring to signs of growth elsewhere in the global economy, Draghi said the ECB policy would remain accommodative even as other countries' monetary policy may acknowledge recovery is taking place. The EU's statistics office Eurostat said consumer inflation among the 18 Eurozone countries rose 0.1% MoM in August for a 0.4% YoY increase. Inflation has fallen steadily since the end of 2011, reflecting a weak Eurozone economy and near-record unemployment, after a debt crisis ripped the bloc apart. (Reuters)

Slide in German business morale points to weak 3Q2014 – Business sentiment in Germany fell for the fifth consecutive month in September to its lowest level in nearly 18 months, dampening expectations for a third-quarter rebound in Europe's largest economy. The Munich-based Ifo think tank's Business Climate Index, which is based on a monthly survey of 7,000

firms, fell to 104.7 from 106.3. The Reuters consensus had forecast for a milder decline to 105.7. Ifo survey showed the German economy is no longer running smoothly and the sentiment is worsening across all sectors of the economy. The German economy surged at the start of the year thanks to an unusually mild winter that boosted construction activity; but it contracted by 0.2% in 2Q2014, leading some economists to warn of the risk of recession. (Reuters)

WB: Russian economy to stagnate over next two years – The World Bank (WB) said Russia's economy is set to stagnate over the next two years as the country pays the price for the Ukraine crisis, lack of structural reforms and an uncertain economic policy. In a much more pessimistic outlook than the Russian government’s, the Washington-based lender forecast the economy would grow by just 0.3% next year and could contract if the Ukraine crisis escalates. WB said Russian GDP will increase by 0.4% in 2016, while the Russian government estimates a growth of 1.2% in 2015 and 2% in 2016. Sanctions imposed by the US and Europe over Russia's involvement in Ukraine will dampen investment, while consumption growth in coming years – a major driver behind Russia's economy – will be subdued. (Reuters)

Japan flash PMI shows manufacturing picked up in 3Q2014 – A recent PMI survey showed Japan's manufacturing activity picked up in 3Q2014, but economists say they need more information on wages and consumer spending to determine whether the government should raise the sales tax again next year. An improving corporate sector is certainly welcome news for Japanese Prime Minister Shinzo Abe after the economy contracted sharply in 2Q2014, following the sales tax hike in April. However, the government, which is monitoring data to decide whether to raise the sales tax again, is likely to remain cautious for fear that consumer spending may not fully recover. Abe is set to make a final decision by the end of the year. The Markit/JMMA flash Japan Manufacturing Purchasing Managers Index (PMI) fell to a seasonally adjusted 51.7 in September from a final reading of 52.2 in August, but remained above the 50 threshold for a fourth straight month. (Reuters)

IMF: China has many tools to keep growth above 7% next year – The International Monetary Fund said China has many tools to keep its growth well above 7% next year, downplaying the risks of the cooling property market in the world's second- largest economy. Changyong Rhee, Director of the Asia Pacific Department at the IMF said economic growth in China is likely to be well above 7% next year. Rhee’s remarks suggested the global lender is likely to upgrade its growth forecast for the country due next month from the current 7.1% estimate. The IMF has a 7.4% growth forecast for China for 2014, slightly below the government's official target of around 7.5%. Many economists see the rapidly slowing property market as the biggest risk facing China's economy. Home prices, sales and new construction are all falling, which are burdening other related sectors. Analysts believe Beijing will roll out more stimulus measures in coming months to avert a deeper economic slowdown, including help for would-be home buyers. However, Rhee said the IMF does not expect China's cooling property market to become a serious problem, saying it sees a gradual adjustment rather than a hard landing. (Reuters)

Regional

CBRE: Mideast investors to spend $180bn in commercial realty markets – According to ‘Middle East: In and Out' report by CBRE, Middle Eastern (Mideast) investors are expected to spend $180bn in the commercial real estate markets outside their own region over the next decade. The major increase in

4. Page 4 of 6

Mideast capital flows into global markets is emerging from the extraordinary mismatch between the lack of institutional real estate in domestic markets and the huge spending power concentrated in the region. The CBRE report indicated that with $20bn invested outside their home region in commercial property in the last two years alone – there is strong evidence that Middle Eastern players are increasing their interest and investment allocations to direct real estate. (GulfBase.com)

HSBC Bank Middle East raises $400mn through bonds issue – HSBC Bank Middle East raised $400mn through a five- year bond issue at a spread of 85 basis points over mid-swaps. The issue, arranged solely by HSBC, is priced at a coupon of 2.75%, with a reoffer price of 99.824. (Reuters)

BNP, StanChart said to join Algosaibi Group in debt negotiations – According to sources, BNP Paribas and Standard Chartered (StanChart) are among lenders that are negotiating a $5.9bn debt restructuring deal with Ahmad Hamad Algosaibi & Brothers Company. The two banks are part of a five- member creditors’ steering committee that will hold talks with the Saudi Arabian business group on behalf of about 87 lenders. Reportedly, Dubai-based Emirates NBD, Bahrain’s Arab Banking Corporation and New York-based asset manager Fortress Investment Group make up the rest of the committee. (Bloomberg)

Boeing, KACST launch Decision Support Center – Boeing Company has partnered with King Abdulaziz City for Science & Technology (KACST) to launch the Decision Support Center (DSC) at KACST. The center will serve as a key tool for collaboration and experimentation between customers and partners in Saudi Arabia providing users with the ability to make more informed modernization and interoperability decisions regarding aerospace and defense platforms. The agreement is a part of Boeing’s commitment to support Saudi Arabia’s efforts to develop applied research and technology capabilities and infrastructure. (GulfBase.com)

ZPE wins SR29mn steam drum supply contract – Zamil Process Equipment Company (ZPE), a subsidiary of Zamil Industrial Investment Company (ZIIC) has been awarded a contract worth approximately SR29.4mn by STF. Under the terms of the contract, ZPE will supply 36 steam drums (high pressure, intermediate pressure and low pressure) that weigh approximately 1,800 metric tons in total for the PP 13 & 14 combined cycle power plants project owned by the Saudi Electricity Company (SEC) and located near Riyadh. The shell thickness of each high-pressure drum is 120mm and the material used for construction is SA 299 Grade B. (GulfBase.com)

Emaar EC secures SR2bn Murabaha financing – Emaar, The Economic City (Emaar EC) has signed a SR2bn Murabaha financing agreement with the Saudi British Bank (SABB). The loan period extends from September 25, 2014 until September 25, 2021. The purpose of the loan is to complete residential and infrastructure projects in King Abdullah Economic City. The company pledges all of its shares in the Port Development Company, totaling 260.5mn shares. (Tadawul)

IGC signs supply agreement with SABIC; Sipchem starts trials operations of new plant in Riyadh – Saudi International Petrochemical Company (Sipchem) announced that its affiliate International Gases Company (IGC) has signed a long-term carbon monoxide (CO) supply agreement with Saudi Basic Industries Corporation’s (SABIC) affiliate the Saudi Methacrylates Company (SAMAC), which will be used as feedstock in the production of 250 KTA methyl methacrylate (MMA). CO is one of the raw materials required by SAMAC and

IGC will process natural gas, allocated by ARAMCO to SABIC, for this purpose at its existing plant in Jubail Industrial City. Once the SAMAC plant is operational, IGC will be able to increase its production and sales of CO by 23%. IGC operates a CO plant, which is considered to be one of the largest of its kind in the world; producing 345,000tpa of CO. Sipchem owns 72% of IGC and 28% is owned by local investors. Meanwhile, Sipchem had started trial operations of a new plant in Riyadh along with South Korea's Hanwha Chemical. The plant, which has an annual production capacity of 1,000 tons of plastic moulds, is estimated to cost SR110mn. (Tadawul, Reuters)

CSO: Saudi Arabia GDP growth drops to 3.8% in 2Q2014 as oil sector slows – According to data released by the Central Statistics Office (CSO), Saudi Arabia's economic growth eased to an annual 3.8% in 2Q2014, the lowest rate in a year, because of a slowdown in the oil sector. The growth rate for inflation- adjusted GDP was revised up to 5.1% in 1Q2014 – the fastest pace since the 3Q2012 from an initial reading of 4.7%. The GDP dropped 3.1% on a QoQ basis in 2Q2014, the biggest fall since the quarterly data series began in 2010, after a 4.1% jump in the previous quarter. The growth in the hydrocarbons sector, which accounts for almost half of the $748bn Saudi economy, slumped to 2.5% YoY in 2Q2014 from 6.1% in the previous three months. (Reuters)

Ashmore-led group sells GEMS to Gulf group – Ashmore-led group has sold Global Environmental Management Services (GEMS), a Saudi Arabia-based waste management company to a group of Gulf private equity firms. Jadwa Investment confirmed in a statement it had bought the company through its Jadwa Waste Management Opportunities Fund. Reportedly, Dubai- based Fajr Capital was also involved as a buyer and that the price was around $300mn. (Reuters)

UAE plans more Fujairah crude oil storage – The UAE is planning to expand its crude storage at the Arabian Sea port of Fujairah and new berthing facilities are being built to allow large crude carriers (VLCC). Fujairah, the UAE's only major port on the Arabian Sea, has grown rapidly to become the world's second-largest bunkering fuel hub after Singapore. The UAE plans to expand Fujairah's crude storage to 12mn barrels, from 8mn barrels. Fujairah Government’s technical advisor, Salem Abdo Khalil said that the emirate has eight storage tanks, each with 1mn barrels capacity, and foundations have been laid for four new tanks. No date has been set for completion of the new storage. (GulfBase.com)

Abraaj plans to raise $500mn fund for Turkey deals – According to sources, Abraaj Group Limited is raising a $500mn fund to invest in Turkey. Abraaj, which has about $7.5bn in global assets under management, according to its website, plans to reach its fundraising target by 2014-end. (Bloomberg)

DP announces hotel project at Cityscape Global – Dubai Properties (DP) has launched a luxury hotel, a waterfront district (Dubai Wharf) and an upscale twin-tower (Maram Residence) at the Cityscape Global expo in Dubai. The luxury hotel, which is due to open in early 2018, will be operated by Anantara Hotel Resorts & Spa. The hotel will be located in the heart of the Culture Village directly facing the Dubai Creek and close to the new mixed-use project Dubai Wharf. The hotel will comprise 270 rooms and will have waterfront views of the creek. (GulfBase.com)

Savills: Dubai drops to ninth rank as world’s most expensive city – According to a report by Savills, Dubai is becoming more affordable to live and work in, and is ranked ninth most expensive city in the world for companies to locate employees. The drop in the ranking from eighth to ninth was

5. Page 5 of 6

achieved despite Dubai having witnessed a 12% growth in rents in 1H2014, and high price growth in its residential markets, with values up 22.8%. The ranking has dropped a notch since 2008 when Dubai was placed 8th in the index, but is still ahead of Shanghai and Rio De Janeiro. The cost of living and working in Dubai were deemed 16% lower than in 2008. (GulfBase.com)

EMG’s listing likely to price at AED2.9 per share – According to sources, Emaar Properties is expected to price the flotation of its malls unit, Emaar Malls Group (EMG) at AED2.9 a share. Reportedly, the price would give the unit a value of AED37.7bn. Strong demand has seen the institutional tranche oversubscribed at 7.5 times at the top end of the AED2.5-2.9 range, while the retail tranche is oversubscribed 20 times. (Reuters)

DSI Saudi unit wins AED189mn MEP contract – Drake & Scull Saudi Arabia, a subsidiary of Drake & Scull International (DSI) has won an AED189mn MEP contract for Al-Dara Hospital and Medical Center in Riyadh. The contract commences immediately and has to be completed by January 2016. Under the agreement terms, DSI will undertake complete installation, testing and commissioning of critical MEP systems, like HVAC, plumbing and firefighting systems as well as electrical systems for the 107-bed hospital, located close to the King Faisal Specialist Hospital in Riyadh. (DFM)

DFM eIPO successfully implements EMG’s IPO – The Dubai Financial Market (DFM) stated that its eIPO platform has witnessed enormous turnout from investors in the UAE and other countries in the region during the IPO of Emaar Malls Group (EMG). This success has been enabled by the platform’s multiple smart channels including a direct connection with the receiving banks, and through the iVESTOR card. The proportion of electronic applications jumped 10 times to 20% of the total number of applications, from 2% during the previous IPO. (Zawya)

Al Mazaya purchases 2 land plots for KD3.95mn – Al Mazaya Holding announced that its subsidiary Mazaya Real Estate Development Company has purchased two investment land plots for a total amount of KD3.95mn. (DFM)

Masdar agrees to buy Statoil stake in UK wind project – Masdar Abu Dhabi Future Energy Company (Masdar) has agreed to buy half of Statoil’s stake in the 402-megawatt Dudgeon wind project off the coast of eastern England, UK. The transaction will give Masdar a 35% stake in the project valued at $860mn. Statoil is a multinational energy company, which will operate the plant and retains a 35% stake, while fellow Norwegian company Statkraft owns the remainder. (GulfBase.com)

Etihad to take first A380 delivery – Etihad Airways is scheduled to take the delivery of its first Airbus A380 aircraft on September 25, 2014 in Hamburg. The aircraft is one among the 10 A380s the airline has ordered. (Bloomberg)

Trowers & Hamlins to act as legal counsel for $2.8bn Orpic loan deal – Trowers & Hamlins has been appointed as the local counsel to advise a consortium of 21 international and local financial institutions on all legal aspects of the financing of a $2.8bn loan arranged for Oman Oil Refineries & Petroleum Industries Company (Orpic). The loan will be utilized for certain large-scale projects of Orpic over the coming years, including the $2.1bn Sohar Refinery Improvement Project. The project will involve engineering, procurement, construction, start-up and commissioning services, which will be 65% debt financed. (Bloomberg)

Alba receives approval for line 6 gas allocation – Aluminium Bahrain (Alba) has received approval from Bahrain’s government for the gas allocation needed to support its planned sixth production line. Alba’s CFO, Isa al-Ansari said that once secured, the scheme will take 36 months to complete and production should begin in 1Q2018. (GulfBase.com)

6. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg, *$ adjusted returns.

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

Aug-10 Aug-11 Aug-12 Aug-13 Aug-14

QE Index S&P Pan Arab S&P GCC

(1.4%)

(0.5%)

0.2%

(0.2%)

0.1%

(0.1%)

(1.2%)

(1.8%)

(1.2%)

(0.6%)

0.0%

0.6%

Saudi Arabia

Qatar

Kuwait

Bahrain

Oman

Abu Dhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD%

Global Indices Performance Close 1D%* WTD%* YTD%*

Gold/Ounce 1,217.06 (0.5) 0.1 0.9 DJ Industrial 17,210.06 0.9 (0.4) 3.8

Silver/Ounce 17.70 (0.6) (0.7) (9.1) S&P 500 1,998.30 0.8 (0.6) 8.1

Crude Oil (Brent)/Barrel (FM

Future)

96.95 0.1 (1.5) (12.5) NASDAQ 100 4,555.22 1.0 (0.5) 9.1

Natural Gas (Henry

Hub)/MMBtu

3.84 (1.4) (0.4) (11.6) STOXX 600 344.35 0.2 (1.6) (2.7)

LPG Propane (Arab Gulf)/Ton 105.88 (0.8) (1.9) (16.3) DAX 9,661.97 0.2 (1.8) (6.3)

LPG Butane (Arab Gulf)/Ton 124.50 (0.3) (1.5) (8.3) FTSE 100 6,706.27 0.3 (1.7) (2.0)

Euro 1.28 (0.5) (0.4) (7.0) CAC 40 4,413.72 0.77 (1.4) (4.7)

Yen 109.04 0.1 0.0 3.5 Nikkei 16,167.45 (0.2) (0.9) (4.2)

GBP 1.63 (0.3) 0.3 (1.3) MSCI EM 1,035.31 0.2 (1.8) 3.3

CHF 1.06 (0.6) (0.5) (5.6) SHANGHAI SE Composite 2,343.58 1.5 0.7 9.2

AUD 0.89 0.5 (0.4) (0.4) HANG SENG 23,921.61 0.3 (1.6) 2.7

USD Index 85.04 0.4 0.4 6.2 BSE SENSEX 26,744.69 0.1 (1.4) 28.2

RUB 38.19 (1.0) (0.6) 16.2 Bovespa 56,824.42 0.7 (2.7) 8.4

BRL 0.42 1.0 (0.9) (1.0) RTS 1,189.23 1.9 1.6 (17.6)

200.2

165.5

148.8