(DIYA) Bhumkar Chowk Call Girls Just Call 7001035870 [ Cash on Delivery ] Pun...

2 July Daily market report

1. Page 1 of 7

QE Intra-Day Movement

Qatar Commentary

The QE index rose 2.1% to close at 12,384.2. Gains were led by the Telecoms

and Transportation indices, gaining 3.9% and 3.3%, respectively. Top gainers

were Qatar Cinema & Film Distri. Co. and Qatar Islamic Bank, rising 9.4% and

7.1%, respectively. Among the top losers, Industries Qatar fell 2.2%, while Al

Ahli Bank declined 1.8%.

GCC Commentary

Saudi Arabia: The TASI index rose 1.0% to close at 9,678.5. Gains were led

by the Real Estate Dev. and Hotel & Tou. indices, rising 2.3% and 1.9%,

respectively. Alhokair Group and Umm Al-Qura Cement Co. rose 9.9% each.

Dubai: The DFM index gained 7.9% to close at 4,389.9. The Investment &

Financial Services index gained 13.4%, while the Services index rose 10.0%.

Gulf General Invest. Co. surged 15.0%, while Arabtec Holding was up 14.9%.

Abu Dhabi: The ADX benchmark index rose 5.0% to close at 4,806.8. The

Inv. & Financial Services index gained 14.5%, while the Real Estate index was

up 11.4%. Eshraq properties surged 14.9%, while Waha Capital gained 14.5%.

Kuwait: The KSE index gained 1.1% to close at 7,026.3. The Consumer

Goods and Banking indices rose 3.1% and 1.8%, respectively. Noor Financial

Investment gained 9.3%, while Palms Agro Production Co. was up 9.1%.

Oman: The MSM index rose 0.1% to close at 7,024.8. Gains were led by the

Financial and Industrial indices, rising 0.5% and 0.1%, respectively. Al Madina

Takaful gained 6.8%, while Oman Fisheries was up 3.4%.

Bahrain: The BHB index gained 0.3% to close at 1,430.6. The Industrial index

rose 0.9%, while the Commercial Banking index was up 0.6%. National Bank

of Bahrain and Ahli United Bank gained 1.3% each.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Qatar Cinema & Film Distri. Co. 49.45 9.4 0.2 23.3

Qatar Islamic Bank 93.50 7.1 357.5 35.5

Medicare Group 85.40 6.8 178.5 62.7

Qatar International Islamic Bank 83.00 5.7 142.0 34.5

Ezdan Holding Group 22.51 5.2 4,687.1 32.4

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Vodafone Qatar 18.15 5.1 6,228.2 69.5

Ezdan Holding Group 22.51 5.2 4,687.1 32.4

Masraf Al Rayan 51.50 3.0 3,337.8 64.5

Mazaya Qatar Real Estate Dev. 17.58 3.8 1,882.1 57.2

Qatar Gas Transport Co. 22.11 5.1 1,179.5 9.2

Market Indicators 02 Jul 14 01 Jul 14 %Chg.

Value Traded (QR mn) 949.8 848.9 11.9

Exch. Market Cap. (QR mn) 678,137.4 666,761.2 1.7

Volume (mn) 25.4 20.9 21.8

Number of Transactions 10,172 9,953 2.2

Companies Traded 42 41 2.4

Market Breadth 31:10 40:1 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,470.98 2.1 4.8 24.6 N/A

All Share Index 3,145.78 1.7 4.4 21.6 15.1

Banks 3,034.66 2.5 7.2 24.2 15.1

Industrials 4,147.09 (0.6) 1.7 18.5 16.2

Transportation 2,167.11 3.3 2.2 16.6 13.9

Real Estate 2,603.00 2.9 5.8 33.3 13.0

Insurance 3,419.39 0.5 0.3 46.4 8.9

Telecoms 1,572.16 3.9 2.8 8.1 21.7

Consumer 6,746.68 1.5 2.2 13.4 26.5

Al Rayan Islamic Index 4,120.14 2.4 4.6 35.7 17.8

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Arabtec Holding Co. Dubai 3.31 14.9 271,196.3 61.5

Dubai Financial Market Dubai 2.87 14.8 75,546.5 16.2

Drake & Scull Int. Dubai 1.48 14.7 102,655.5 2.8

Deyaar Development Dubai 1.10 14.6 137,312.6 8.9

Ajman Bank Dubai 2.60 13.0 10,702.2 4.8

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

National Mobile Tele. Kuwait 1.68 (3.5) 5.3 (4.6)

Saudi Cement Saudi Arabia 111.42 (3.4) 145.0 9.8

Industries Qatar Qatar 172.00 (2.2) 190.9 1.8

Abu Dhabi Nat. Energy Abu Dhabi 1.08 (1.8) 11.4 (26.5)

Al Ahli Bank Qatar 50.10 (1.8) 4.3 18.4

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Industries Qatar 172.00 (2.2) 190.9 1.8

Al Ahli Bank 50.10 (1.8) 4.3 18.4

Widam Food Co. 53.10 (1.7) 68.7 2.7

Salam International Investment Co 16.35 (1.4) 1,030.4 25.7

Qatar National Cement Co. 133.00 (1.3) 6.0 11.8

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Masraf Al Rayan 51.50 3.0 171,856.4 64.5

Vodafone Qatar 18.15 5.1 111,729.5 69.5

Ezdan Holding Group 22.51 5.2 106,486.7 32.4

QNB Group 177.00 1.6 89,376.1 2.9

Doha Bank 57.00 0.4 45,058.6 (2.1)

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,384.24 2.1 4.8 7.8 19.3 260.90 186,284.3 15.4 2.1 4.1

Dubai 4,389.94 7.9 4.0 11.3 30.3 817.33 86,213.9 17.6 1.7 2.4

Abu Dhabi 4,806.75 5.0 1.7 4.2 10.5 150.72 133,857.5 14.0 1.8 3.5

Saudi Arabia 9,678.51 1.0 1.1 1.7 13.4 1,734.42 527,768.8 19.3 2.4 2.9

Kuwait 7,026.29 1.1 0.6 0.8 (6.9) 62.29 111,258.3 16.7 1.1 4.0

Oman 7,024.77 0.1 1.2 0.2 2.8 14.90 25,997.8 12.1 1.7 3.9

Bahrain 1,430.56 0.3 (0.1) 0.2 14.5 0.25 53,475.8 11.2 1.0 4.8

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,100

12,200

12,300

12,400

12,500

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 7

Qatar Market Commentary

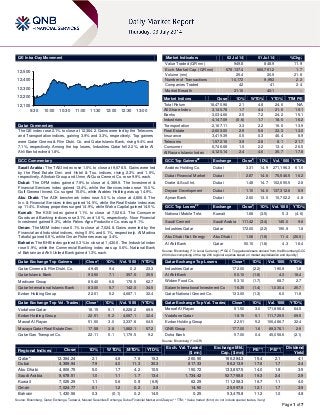

The QE index rose 2.1% to close at 12,384.2. The Telecoms and

Transportation indices led the gains. The index rose on the back

of buying support from non-Qatari shareholders despite selling

pressure from Qatari shareholders.

Qatar Cinema & Film Distri. Co. and Qatar Islamic Bank were the

top gainers, rising 9.4% and 7.1% respectively. Among the top

losers, Industries Qatar fell 2.2%, while Al Ahli Bank declined

1.8%.

Volume of shares traded on Wednesday rose by 21.8% to

25.4mn from 20.9mn on Tuesday. Further, as compared to the

30-day moving average of 21.9mn, volume for the day was

16.3% higher. Vodafone Qatar and Ezdan Holding Group were

the most active stocks, contributing 24.5% and 18.4% to the total

volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Global Economic Data

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

07/02 US MBA MBA Mortgage Applications 27 June -0.20% – -1.00%

07/02 US IPSOS Public Affairs RBC Consumer Outlook Index July 50.5 – 51.0

07/02 US ADP ADP Employment Change June 281K 205K 179K

07/02 EU Eurostat PPI MoM May -0.10% 0.00% -0.10%

07/02 EU Eurostat PPI YoY May -1.00% -1.00% -1.20%

07/02 UK Markit Markit/CIPS UK Construction PMI June 62.6 59.8 60.0

07/02 Spain Spanish Labour Ministry Unemployment MoM Net ('000s) June -122.7 -150.1 -111.9

07/02 Japan Bank of Japan Monetary Base YoY June 42.60% – 45.60%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QNB Capital appoints new CEO – The Board of Directors of

QNB Capital, the investment banking subsidiary of QNB Group

(QNBK), has appointed Mira Hamad Abdullah Al Attiyah as its

Chief Executive Officer. Ms. Al Attiyah had recently held the

position of assistant undersecretary for trade at the Ministry of

Economy and Commerce. She has been occupying several

senior positions within the ministry and at the Supreme Council

for Information and Communication Technology. She was also a

key member of several national committees in the business and

investment sector. QNB Capital provides a wide range of

services to corporations, government and institutional clients

locally and globally. (Gulf-Times.com)

CBQK initiates squeeze-out process at its Turkish

subsidiary Alternatifbank – The Commercial Bank of Qatar

(CBQK), Anadolu Endustri Holding and Anadolu Motor Uretim

ve Pazarlama holding 74.25%, 17.21% and 7.79% shares of

Alternatifbank (ABank), Turkey, respectively, have initiated a

formal squeeze-out process pursuant to which CBQK will

acquire a further 0.75% shares of ABank from the Bourse

Istanbul. The necessary application regarding the squeeze out,

and simultaneous delisting from Bourse Istanbul, has been

submitted to ABank's board of directors on July 1, 2014. In

accordance with the applicable laws of Turkey, the purchase

price of the shares acquired through the squeeze out is

expected to be the average price over the last 30 days. (QE)

QIBK and Bank Asya end exclusive talks over stake sale –

According to sources, Qatar Islamic Bank (QIBK) and Turkey's

Bank Asya have ended exclusive talks over the former acquiring

a stake in Bank Asya due to valuation concerns. Turkish state

bank Ziraat Bank may now be the most likely partner for Bank

Asya, but the two banks have not officially begun talks.

(Reuters)

Turkey-based Anel Elektrik’s unit inks QR169.3mn LOI for

road project in Qatar – Turkey-based Anel Elektrik’s unit,

Anelmep Maintenance & Operation, has signed QR169.3mn

letter of intent (LOI) to carry out electrical and mechanical works

related to the Al Rayyan road construction & development

project in Qatar. Anelmep Maintenance & Operation has inked

the agreement with the project’s main contractor Dogus Onur JV

– a joint venture between Turkish companies Dogus and Onur.

The project envisages the construction of a 10.7 km long road

section and is expected to be completed in 1Q2017.

(Bloomberg)

HPS to supply integrated control and safety system for

QAFAC’s plant – Qatar Fuel Additives Company (QAFAC) has

selected the UK-based Honeywell Process Solutions (HPS) to

supply a new integrated control & safety system for its Mesaieed

Industrial City plant, 50 kilometers south of Doha. The

upgradation work will help the plant reduce operating costs and

improve efficiencies as it scales up production of methanol and

MTBE (methyl tertiary butyl ether), a key gasoline additive that

reduces tailpipe. HPS’s integrated control & safety solution,

including a new fire and gas system, will improve automation at

the plant, increase cyber security, and enhance operator

effectiveness. QAFAC will also benefit from the ongoing long-

term services through Honeywell's lifecycle support. QAFAC is a

joint venture between Industries Qatar (IQCD), OPIC Middle

East, LCY and IOL. (Bloomberg)

Total E&P Qatar sees potential in offshore Al Khalij oilfield,

signs agreement with QP – Total E&P Qatar sees interesting

potential in the offshore Al Khalij oilfield, for which it has signed

Overall Activity Buy %* Sell %* Net (QR)

Qatari 62.08% 63.70% (15,367,480.21)

Non-Qatari 37.92% 36.30% 15,367,480.21

3. Page 3 of 7

an agreement with Qatar Petroleum (QP) to form a JV for 25

years from 2014. Under the terms of this new JV, QP and Total

hold 60% and 40% interest, respectively, in the oilfield. Total

continues to operate the oilfield. Total E&P Qatar’s Managing

Director and Group representative Guillaume Chalmin said that

the JV intends to enhance oil recovery as much as possible from

this mature offshore oilfield. (Gulf-Times.com)

DHBK to disclose results on July 16, 2014 – Doha Bank

(DHBK) will disclose its financial reports for the period ending

June 30, 2014, on July 16, 2014. (QE)

KCBK to announce results on July 17, 2014 – Al Khalij

Commercial Bank (KCBK) will announce its financial reports for

the period ending June 30, 2014, on July 17, 2014. (QE)

VFQS wins Golden CSR award – The Arab Organization for

Social Responsibility has recently recognized Vodafone Qatar

(VFQS) with the Golden Corporate Social Responsibility (CSR)

award. Vodafone Qatar has recently launched the fourth edition

of its annual program, World of Difference, which gives financial

grants to a number of people to carry out their creative ideas

that generate tangible benefits for the community. (Gulf-

Times.com)

QA named official carrier of IASP 2014 – The Qatar Science

& Technology Park (QSTP) has announced that Qatar Airways

(QA) will be the official carrier of the International Association of

Science Parks and Areas of Innovation’s (IASP) 31st Annual

World Conference (IASP 2014 Doha). IASP 2014 Doha is a

global gathering of science parks, entrepreneurs and policy

makers. As the event’s official carrier, QA will help bring roughly

1,000 leading government, business and technology innovation

delegates from 45 countries to Qatar. (Gulf-Times.com)

International

Yellen says rate policy shouldn’t change over instability –

Federal Reserve Chairman Janet Yellen said there is no need to

change the current monetary policy to address the financial

stability concerns although she sees “pockets of increased risk-

taking” in the financial system. In a comprehensive salvo into the

worldwide debate among central bankers over whether interest

rates are a first-order tool to curb financial excess, Yellen came

down against that idea and favored regulatory mechanisms.

Yellen added that the monetary policy faces significant

limitations as a tool to promote financial stability. She said that

the policy’s effects on financial vulnerabilities, such as excessive

leverage & maturity transformation, are not well understood and

are less direct than a regulatory or supervisory approach. Yellen

stated that the “primary role” should fall to a macroprudential

approach, a combination of multiagency oversight, attention to

bank capital & liquidity, and regulatory pressure to create buffers

against failure. (Bloomberg)

Moody's Analytics: US wage growth seen modest into 2016

– Moody's Analytics' chief economist Mark Zandi said US wage

growth will likely remain modest into 2016 even as employers

have ramped up hiring in recent months. Zandi projected the

average domestic wages to likely increase at a 2.5% pace in

2015 and 3.0% in 2016, as compared to the current 2.0% rate.

Zandi said while wage growth is expected to remain "spotty" in

the next couple of years, there are signs of rising salaries in

certain regions of the US and high-paying sectors where there is

a scarce supply of qualified workers. The pace of pay increases

is expected to accelerate when the economy achieves full

employment, which he expects will occur in 2016. Earlier, the

ADP National Employment Report, which Moody's jointly

developed with ADP, showed the US private sector added

281,000 jobs last month, marking the biggest monthly rise since

November 2012. (Reuters)

Markit : UK construction PMI hits four-month high in June –

Industry data showed a surge in home-building helped British

construction activities to grow at its fastest annual pace in four

months in June, bucking expectations for a slowdown. The

monthly Markit/CIPS purchasing managers' index (PMI) for the

construction sector rose to 62.6 in June from 60.0 in May, its

highest level since February and well above the forecast for a

fall to 59.5. Readings above 50 represent a YoY growth in

activities, and those below 50 point to contraction. The

equivalent manufacturing survey on Tuesday also beat

expectations, driving sterling to its highest level in nearly six

years and bolstering expectations that the Bank of England

would raise interest rates this year. The construction survey

showed the fastest pace in hiring in the sector since 1997.

Official data released last week showed that Britain's

construction output rose by 1.5% in the first three months of

2014 and was 6.7% higher than a year earlier - the biggest

annual rise in three years. The PMI figures pointed to ongoing

momentum in the sector, with new orders coming in at the

fastest rate since January. (Reuters)

China's official services PMI eases slightly to 55 in June –

Government data showed growth in China's services sector

edged down from a six-month high in June, with the purchasing

manufacturing index (PMI) for the industry slipping to 55. That

compares with a reading of 55.5 in May, according to the

National Bureau of Statistics. A reading above 50 in PMI

surveys indicates growth on a monthly basis, while an outcome

below the threshold points to a contraction in activity. More

economic indicators are suggesting that the world's second-

largest economy is steadying as a flurry of government stimulus

measures start to kick in. The results in other similar surveys of

Chinese factories earlier in the week have also been upbeat.

(Reuters)

Premier Li says downward pressure still exists for Chinese

economy – China's Premier Li Keqiang said downward

pressure still existed in its economy despite it operating within a

reasonable range and some leading indicators demonstrating a

positive trend. China's factory activities hit multi-month highs in

June, official and private surveys showed on Monday,

reinforcing signs that the world's second-largest economy is

steadying as the government steps up policy support. Li gave no

figures or details and few direct quotes in the comments on the

Chinese government's official website, but also addressed the

disconnect between government finances and the difficulty of

business getting financing. Li said the country is finding it harder

and more expensive to finance firms in the real economy. He

further added that these costs must be decreased, especially for

small and medium enterprises. The government has unveiled a

series of modest stimulus measures in recent months to give a

lift to economic growth, which dipped to an 18-month low of

7.4% in the first quarter, China's slowest annual growth since

the third quarter of 2012. (Reuters)

China frees spreads on retail Yuan rate in reform step –

China will permit banks to set their own exchange rates for the

Yuan against the dollar in deals with clients, in a further step to

relax controls to make the currency more market-driven. The

world's second-largest economy seeks to widen the use of the

Yuan in global trade and freeing up its tightly-controlled currency

is a pre-requisite for wider market liberalization. Beijing has

pledged to free up interest rates and currency controls

eventually to help put its economy on a more sustainable

footing, but such changes have so far been gradual. Effective

Wednesday, banks can set the Dollar/Yuan exchange rate in

4. Page 4 of 7

their over-the-counter deals based on market demand, the

foreign exchange regulator said in a statement. Before the

move, the spread in banks' Dollar/Yuan buying and selling

prices had been subject to regulatory controls. The State

Administration of Foreign Exchange (SAFE) has already

scrapped controls on spreads for banks' retail exchange rates

between Yuan and non-dollar currencies. (Reuters)

Regional

STC joins Telecom Council of Silicon Valley – Saudi

Telecom Company (STC) has joined the Telecom Council of

Silicon Valley for business development, collaboration and

education. The Telecom Council of Silicon Valley connects

companies and individuals involved in the communications

technology industry with one another. STC is the first telecom

company in the Middle East to join the Telecom Council of

Silicon Valley, which includes over 100 member companies,

including more than 25 fixed and wireless operators across the

globe. (GulfBase.com)

Accor, Munshaat sign management deal for ZamZam

Pullman Madinah – Accor Hotel Services Middle East and

Munshaat for Projects & Contracting Company have signed a

management agreement for a new upscale Pullman hotel in

Madinah. The five-star ZamZam Pullman Madinah will consist of

two towers, comprising a total of 834 rooms and suites in the

holy city. The construction of the ZamZam Pullman Madinah is

in an advanced stage and is scheduled to be opened by

September 2014. The ZamZam Pullman Madinah is located 150

meters away from the Holy Mosque. (GulfBase.com)

SAMA: Saudi insurance premiums up 19% to SR25bn –

According to a report based on Saudi Arabian Monetary Agency

(SAMA) data, the value of insurance premiums in the Saudi

market rose by 19.2% to reach SR25.2bn in 2013 as compared

to SR21.2bn in 2012. The health insurance sector, which

represented 51% of the insurance market, grew by 14.3% to SR

12.9bn as compared to SR11.3bn in 2012. Growth in general

insurance, which represented 46% of the insurance market,

reached 27.8% to SR11.5bn as compared to SR9bn in 2012,

whereas growth in protection and saving insurance sector,

which represented 3% of the insurance market, dropped by 5%

to SR845mn in 2013 as compared to SR889mn in 2012. As

regards claims, the report said the value of claims substantially

grew to SR15.9bn in 2013 as compared to SR10.9bn in 2012, or

an increase of 45.8%. The number of settled claims in a three-

year period (2010-2013) rose by 36.5%, whereas insurance

premiums rose by only 21% over the same period, which has

negatively affected the operating income of the companies in

general. (GulfBase.com)

Zain Saudi, Huawei sign new Reload Contract agreement –

Mobile Telecommunications Company Saudi Arabia (Zain

Saudi) and Huawei have signed a new Reload Contract

agreement, aimed at advancing its network infrastructure,

managed services and applications in Saudi Arabia. Under the

terms of the new agreement, Huawei will work closely with Zain

Saudi to improve its technologies and extend its customer

service offering for Saudi users. The contract includes Zain’s

network new FTK, expansion, modernization and managed

services. It also includes the provisions of all related products

and services for Zain’s network in Saudi Arabia. (GulfBase.com)

TVTC signs technology agreement with Mobily, Microsoft

Saudi Arabia – Technical and Vocational Training Corporation

(TVTC) has signed a MoU with Etihad Etisalat Company

(Mobily) and Microsoft Saudi Arabia to raise the level of using

technology in the educational process in the TVTC colleges and

in pursuit of enhancing productivity levels & better qualify

students for the labor market. Under the terms of the agreement,

tablet computers will be provided to the trainees with productivity

applications to upgrade the level of students’ productivity

necessary for the labor market. (GulfBase.com)

Saudi Aramco’s subsidiary to buy 28.4% stake in South

Korea-based S-Oil Corporation – Saudi Arabian Oil

Company’s (Saudi Aramco) Netherlands-based subsidiary –

Aramco Overseas Company (AOC) – has agreed in principle to

buy 28.4% stake in South Korea-based S-Oil Corporation from

Hanjin Group, for a purchase consideration of about $1.95bn.

This acquisition will increase AOC's ownership of S-Oil to 63.4%

from 34.99%. (Reuters)

SCC updates on capital increase – Saudi Cable Company

(SCC) revealed its stance on the proposal of capital increase by

stating that it is the process of finalizing the restructuring of its

obligations with lenders, which it expects to complete before the

end of 2Q2014. The company after completing the financial

restructuring and meeting the Capital Market Authority’s (CMA)

requirements, will initiate the process of applying to the CMA for

the capital increase through a rights issue. (Tadawul)

SEC orders transformers worth $78mn from ABB – ABB, a

Zurich-based power and automation technology group, has won

an order worth $78mn from Saudi Electricity Company (SEC).

ABB will supply transformers for two new combined-cycle power

plants that will boost transmission capacity in Riyadh and

surrounding areas of the Central Region. The order was booked

in the 2Q2014. ABB will deliver generator step-up (GSU)

transformers, power transformers and station service

transformers for SEC’s combined-cycle power plants. Saudi

Arabia plans to boost power-generation capacity by more than

50% by 2020 – from less than 60GW to approximately 91GW.

(GulfBase.com)

Tadawul deposits Al-Ahlia’s tradable rights – The Saudi

Stock Exchange (Tadawul) announced that the tradable rights

for Al-Ahlia Insurance Company have been deposited into

applicable investors’ portfolios on July 1, 2014. (Tadawul)

RFIB appoints General Manager of RFIB Saudi Arabia –

RFIB Group Limited, the international Lloyd's insurance &

reinsurance broker, has appointed Hassan El Kaissi as General

Manager of RFIB Saudi Arabia. Hassan brings over 20 years of

experience in the Middle East reinsurance market to his new

role. He had earlier served Zurich Insurance, as the head of its

mid market segment in the Middle East. (Bloomberg)

Midad, Tech Mahindra to establish new 51:49 JV entity –

Saudi-based Midad Holding, wholly-owned by Al Fozan Group

and India-based information technology (IT) company, Tech

Mahindra have entered into an agreement to establish a new

joint venture (JV) entity, Tech Mahindra Arabia (TMA). TMA will

provide a gamut of IT and IT-enabled services (ITES) to cater to

the established and emerging sectors in KSA. The JV would aim

to provide services in the areas of consulting, application

development & management, network services, integration,

engineering, managed services, remote infrastructure

management, operational & maintenance services and business

process outsourcing. Midad will hold a 51% stake, while the

remaining 49% will be held by Tech Mahindra. (Bloomberg)

SCTA signs contract worth SR12mn – Saudi Commission of

Tourism and Antiquities (SCTA) has signed a project contract

worth about SR12mn with a national company for operating

tourist information centers in Saudi Arabia for three years.

(Bloomberg)

Tarmac signs MoU with Etihad Rail – Tarmac Middle East has

signed a MoU with Etihad Rail, the developer and operator of

5. Page 5 of 7

the UAE’s national railway. The MoU will enable Tarmac Middle

East to utilize Etihad Rail operations for the distribution of its

products from its local arm, Al Futtaim Tarmac Quarry Product

Company to Etihad Rail’s distribution and export terminals

across the UAE. It will also enable the distribution to other GCC

counties once Etihad Rail completes its connection to the

mainline GCC rail network at the end of 2018. This will help

Tarmac to reduce operating costs and enhance transit times.

The agreement will also provide Etihad Rail with additional

volumes of bulk commodities transport capability from its export

terminals to other locations within the UAE. It is expected that

the volume to products Tarmac Middle East will transport by

2020 via Etihad Rail will reach 6mn tons. (GulfBase.com)

MEED: Construction contracts worth $15bn awarded in UAE

in 1H2014 – According to data released by MEED Projects,

contracts worth $15bn were awarded in 1H2014 for projects

valued at more than $30mn in the UAE’s civil construction

sectors. More than 50 contracts, worth a total of over $5.4bn,

were for newly-announced or recovered residential projects, and

$3.8bn was for mixed-use projects. The civil construction

projects represented 75% of all awards in the UAE in 1H2014. In

Dubai, 44 major residential projects sector contracts totaling

$4.8bn were awarded in 1H2014. Abu Dhabi, with six projects

worth a total of $500mn, had the second highest level of

residential sector awards measured by value. The top six

contractors measured by value of contracts awarded in the six-

month period all netted over $500mn worth of contracts. Arabian

Construction Company and Arabtec topped the list with over

$1bn each. Over $15bn worth of buildings’ projects have been

recovered, with nearly 80% of these in the mixed-use and

residential sub-sectors, while around $9bn worth of civil sector

projects have changed from on hold to active status in the six-

month period. (Bloomberg)

DME launches new trading mechanism – The Dubai

Mercantile Exchange (DME) has launched a new trading

mechanism, Trade at Marker (TAM), for customers of the DME

Oman crude oil futures contract. TAM will allow DME customers

to buy and sell oil at a price directly linked to DME’s 12:30pm

Marker Price. The average of the month’s Marker Prices on

DME is the basis of the crude oil export price of the Sultanate of

Oman and the Emirate of Dubai, making the DME Marker Price

one of the world’s key energy benchmarks. The ability to trade

the Marker Price directly will be extremely useful to investors

who want exposure to Oman and Dubai‘s crude oil export price,

but who may not necessarily want to trade during DME’s

settlement window. The TAM trading mechanism can be traded

on a daily basis for the front three months of the DME Oman

crude oil contract. (GulfBase.com)

DP commences handover of mixed-use development Bay

Square – Dubai Properties (DP), the development company of

Dubai Properties Group (DPG), has commenced the handover

process at its popular mixed-use Bay Square development in

Business Bay. Bay Square has become one of Dubai’s most

sought-after developments, recording a sell-out response when

it was launched for sale in 2013 which prompted huge demand

for other similar projects in Business Bay. Bay Square

comprises thirteen low-rise buildings which include residential,

commercial, retail units and a hotel facing a landscaped

courtyard. DP has commenced handovers with new owners of

up to 570 commercial units, covering 1mn square ft, in Bay

Square, and with new tenants of over 120 retail units at the

podium level. (GulfBase.com)

HSBC: Arabtec needs to hire 17,500 staff to clear AED60bn

backlog – According to a research report by HSBC, Arabtec

Holding’s ability to meet its ambitious growth strategy could be

seriously hampered by a lack of executive and middle-

management talent in the wake of the crisis that has swept the

contracting company in recent weeks. The report says that the

company needs to hire an additional 17,500 employees to

execute its backlog until 2017, believed to be standing at more

than AED60bn. The report also says Arabtec would have to

outsource as much as 25 per cent of its order backlog.

(GulfBase.com)

Arabtec says it has Aabar’s backing; no projects scrapped

– Arabtec has retained the support of its major shareholder

Aabar Investments and announced that the company has not

cancelled any projects as a result of recent management

changes and a restructuring of the firm. Earlier Aabar diluted its

stake in Arabtec to 18.94% from 21.57%, raising doubts over its

willingness to support the company. (Reuters)

NBAD launches liquidity management fund – The National

Bank of Abu Dhabi (NBAD) has launched the Cash Plus Fund, a

fund designed to offer liquidity, capital preservation and yield

enhancement. The NBAD Cash Plus Fund allows investors to

benefit from higher rates than conventional deposits and avail

liquidity. The Fund is designed for corporates, institutions and

high net worth individuals (HNWI) and suits clients, who would

like to benefit from higher returns on cash without giving up their

liquidity position. NBAD Cash Plus enhances cash yield through

investments into sophisticated money market instruments that

are otherwise not accessible to investors; and allows them to

retain the flexibility to access their investments on a daily basis.

NBAD Cash Plus Fund is open for subscriptions in the form of

private placements with a minimum subscription of AED250,000

with multiples of AED100,000 thereafter. The Fund is an open-

ended, actively managed product, which aims to provide a yield

in excess of overnight deposits, with income distributed daily in

the form of additional units. The Fund aims to capture the best

opportunities available to investors by investing in a range of

high quality money market instruments in the UAE and wider

MENA region, in addition to Asia and Europe. (GulfBase.com)

Kuwait: CPI inflation at 2.9% in May 2014 – Kuwait’s inflation

in the consumer price index (CPI) rose from 2.7% YoY in April

2014 to 2.9% YoY in May 2014 – the marginal rise in inflation

was mostly driven by core inflation (excluding food), which also

climbed from 2.7% YoY in April 2014 to 2.9% YoY in May 2014,

making it currently on par with the overall inflation rate. The rise

in core inflation primarily stemmed from YoY rises in clothing &

footwear prices and furnishing & household maintenance costs.

Food price inflation remained largely unchanged, slowing

marginally from 2.9% YoY in April 2014 to 2.8% YoY, while

inflation in housing rents was steady at 4.6% YoY, unchanged

from April 2014. Pressures in the three other major components

of the CPI - clothing, furnishings and other goods & services

resumed their upward trajectory in May 2014. Inflation is

expected to average 3.0% in 2014, amid firm pressures from the

housing sector. (GulfBase.com)

CBO: Omani Commercial banks’ profits climb 15.1% –

According to the Central Bank of Oman’s (CBO) annual report,

the net profits of commercial banks operating in the Sultanate

rose 15.1% to OMR351.3mn in 2013 after provisions and taxes

from OMR305.3mn in 2012. Of the total profits, local banks’

share stood at OMR337.8mn at 96.2%, while that of foreign

banks amounted to OMR13.5mn at 3.8%. Interest income

remained the dominant component of bank revenues accounting

for 73.3% of the total income in 2013. At OMR841.1mn, interest

income stood higher by 6.5% over the previous year. On the

other hand, interest expenses accounted for 39.1% of total

expenditure in 2013 as compared to 40.1% in the previous year.

However, interest expenses registered an increase of 6.7% from

6. Page 6 of 7

OMR240.3mn in 2012 to OMR256.5mn in 2013. Net interest

income increased from OMR549.4mn in 2012 to OMR584.6mn

in 2013, reflecting a rise of 6.4% over the year. The ratio of

operating expenses to total expenses stood at around 60% over

2011-2013. Provision for taxes increased by 21.2% to

OMR50.3mn in 2013. Cash dividends paid out by local banks to

shareholders increased by 9.2% in 2013 to OMR120.5mn as

compared to OMR110.3mn in the previous year. Stock

dividends, too, rose by 18.7% over the year to OMR64.2mn.

(GulfBase.com)

KFH: Bahrain introduces new personal financing product –

Kuwait Finance House-Bahrain (KFH-Bahrain) has launched a

new personal financing product, Tamweely. The first-of-its-kind

Shari’ah compliant Tawarruq facility, Tamweely, allows

customers to take financing up to BHD100,000 and enjoy a

generous repayment period of up to 84 months. The facility is

based on the international commodity trading of palm oil and is

offered in partnership with one of its international brokers at the

Malaysia bourse. According to an Islamic finance expert,

Tawarruq is a transaction where one party buys some goods on

credit at a marked-up price and sells the same at a lesser value

for the purpose of getting cash. (GulfBase.com)

CIO: Bahrain's economy registers growth – According to the

Central Informatics Organization’s (CIO) statistics, Bahrain's real

economic growth increased to 3.1% in fixed prices and 1.4% at

current prices in 1Q2014 as compared to 1Q2013. The oil sector

grew by 4.1% at constant prices but dropped 0.7% at current

prices, while the non-oil sector increased by approximately 2.9%

and 2.1% at constant and current prices respectively. The

financial projects also registered a growth rate of 1.9% at

constant prices and 1.5% at current prices. The construction

activities grew by 1.5% at constant and current prices

respectively, while the real estate activities rose by about 3.1%

at constant prices and 4% at current prices. The transportation

and telecommunications sectors grew by 4.5% at fixed prices

and 5.3% at current prices, while manufacturing industries rose

by 0.8% at fixed prices and 2.9% at current prices. The CIO

periodical report also showed government-funded projects

growing by 2.4% at fixed prices and about 2.3% at current

prices. Electricity & water sector registered a 3.5% growth at

fixed prices and 3.8% at current prices. Agricultural & fishing

activities increased by 1.1% and 1.2% at fixed and current

prices respectively. Bahrain's GDP grew by 0.1% at fixed prices,

but dropped by 3.2% at current prices in 1Q2014 as compared

to 4Q2013. The oil sector dropped by 7.6% at constant prices

and 10% at current prices, while the non-oil sector soared by

2.3% at constant prices but recorded a 0.7% drop at current

prices. (GulfBase.com)

CBB’s monthly issue of treasury bills oversubscribed by

402% – The Central Bank of Bahrain (CBB) has announced that

the BHD30mn monthly issue of Government T-Bills has been

oversubscribed by 402%. The bills, carrying a maturity of 182

days, are issued by the CBB, on behalf of the Kingdom of

Bahrain. The issue date of the bills is July 6, 2014 and the

maturity date is January 4, 2015. The weighted average rate of

interest is 0.73% as compared to 0.79% for the previous issue

on June 8, 2014. The approximate average price for the issue

was 99.63%, with the lowest accepted price being 99.622%.

With this, the total outstanding value of Government Treasury

Bills is BHD1.230bn. (Bloomberg)

Bahrain Steel launches $340mn seven-year loan – Bahrain

Steel launched a $340mn seven-year syndicated loan. Arab

Banking Corporation, HSBC and Mashreqbank acted as

bookrunners, lead arrangers and underwriters for the

transaction. The company intends to use the proceeds to repay

debt and for general corporate purposes. (Bloomberg)

7. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

200.0

210.0

Jul-10 Jul-11 Jul-12 Jul-13 Jul-14

QE Index S&P Pan Arab S&P GCC

1.0%

2.1%

1.1%

0.3% 0.1%

5.0%

7.9%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,326.86 0.0 0.8 10.1 DJ Industrial 16,976.24 0.1 0.7 2.4

Silver/Ounce 21.16 0.6 0.9 8.7 S&P 500 1,974.62 0.1 0.7 6.8

Crude Oil (Brent)/Barrel (FM

Future)

111.24 (0.9) (1.8) 0.4 NASDAQ 100 4,457.73 (0.0) 1.4 6.7

Natural Gas (Henry

Hub)/MMBtu

4.39 (0.9) 0.3 1.1 STOXX 600 345.68 0.2 1.1 5.3

LPG Propane (Arab Gulf)/Ton 104.75 (1.2) (2.2) (17.2) DAX 9,911.27 0.1 1.0 3.8

LPG Butane (Arab Gulf)/Ton 125.00 (0.8) (1.4) (7.9) FTSE 100 6,816.37 0.2 0.9 1.0

Euro 1.37 (0.1) 0.1 (0.6) CAC 40 4,444.72 (0.4) 0.2 3.5

Yen 101.77 0.2 0.3 (3.4) Nikkei 15,369.97 0.3 1.8 (5.7)

GBP 1.72 0.1 0.8 3.7 MSCI EM 1,060.57 0.9 1.4 5.8

CHF 1.13 (0.1) 0.2 0.5 SHANGHAI SE Composite 2,059.42 0.4 1.1 (2.7)

AUD 0.94 (0.6) 0.2 5.9 HANG SENG 23,549.62 1.5 1.4 1.0

USD Index 79.96 0.2 (0.1) (0.1) BSE SENSEX 25,841.21 1.3 3.0 22.1

RUB 34.35 0.0 1.8 4.5 Bovespa 53,028.78 (0.3) (0.2) 3.0

BRL 0.45 (0.9) (1.3) 6.4 RTS 1,390.47 2.1 0.8 (3.6)

178.0

150.6

136.4