Analysis of Mergers & Acquisitions in IT Services & BPO

•

0 gefällt mir•186 views

M&As went slow in 2009 but there are signs of accelerated activity in 2010. IT services accounts for over two-thirds of the deals in value and domestic deals are in favor over crossborder ones.

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Mehr von Niketa Chauhan

Mehr von Niketa Chauhan (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (13)

Analysis of Mergers & Acquisitions in IT Services & BPO

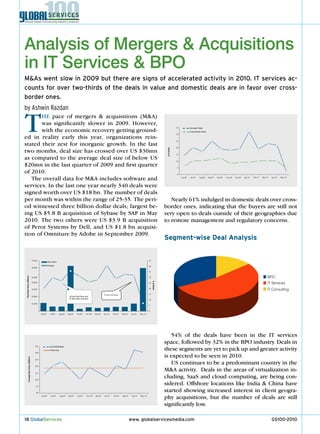

- 1. Analysis of Mergers & Acquisitions in IT Services & BPO M&As went slow in 2009 but there are signs of accelerated activity in 2010. IT services ac- counts for over two-thirds of the deals in value and domestic deals are in favor over cross- border ones. by Ashwin Razdan T He pace of mergers & acquisitions (M&A) was significantly slower in 2009. However, with the economic recovery getting ground- ed in reality early this year, organizations rein- stated their zest for inorganic growth. In the last 35 30 25 Domestic Deals Cross-Border Deals 20 # of Deals two months, deal size has crossed over US $30mn 15 as compared to the average deal size of below US 10 $20mn in the last quarter of 2009 and first quarter 5 of 2010. 0 The overall data for M&A includes software and Jun-09 Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 services. In the last one year nearly 340 deals were signed worth over US $18 bn. The number of deals per month was within the range of 25-35. The peri- nearly 61% indulged in domestic deals over cross- od witnessed three billion dollar deals; largest be- border ones, indicating that the buyers are still not ing US $5.8 B acquisition of Sybase by SAP in May very open to deals outside of their geographies due 2010. The two others were US $3.9 B acquisition to remote management and regulatory concerns. of Perot Systems by Dell, and US $1.8 bn acquisi- tion of Omniture by Adobe in September 2009. Segment-wise Deal Analysis $7,000 45 Deal Value # Deals 40 $6,000 35 BPO Total Deal Value (US$mn) $5,000 30 IT Services # of Deals $4,000 25 $3,000 20 IT Consulting $5.8bn SAPSvbase 15 $2,000 $3.9bn Dell-Perot and $1.8bn Adob-Omniture 10 $1,000 5 0 Jun-09 Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 54% of the deals have been in the IT services space, followed by 32% in the BPO industry. Deals in $35 these segments are yet to pick up and greater activity Avg ExBn$Deals Period Avg $30 is expected to be seen in 2010. Average Deal Value (US$mn) $25 $20 US continues to be a predominant country in the $15 M&A activity. Deals in the areas of virtualization in- $10 cluding, SaaS and cloud computing, are being con- $5 sidered. Offshore locations like India & China have $0 started showing increased interest in client geogra- Jun-09 Jul-09 Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 phy acquisitions, but the number of deals are still significantly low. 18 GlobalServices www. globalservicesmedia.com GS100-2010