Everything you ever Wanted to Know about Florida Property Tax Exemptions.pdf

August 2009 Edition: Toronto Real Estate Market Views

1. Market Views

Magda Mo’s

PREFERRED CLIENT NEWSLETTER AUGUST 2009

Record setting July resale market Magda Mo

Sales Representative

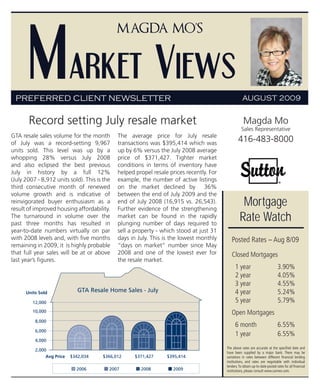

GTA resale sales volume for the month The average price for July resale

of July was a record-setting 9,967 transactions was $395,414 which was

416-483-8000

units sold. This level was up by a up by 6% versus the July 2008 average

whopping 28% versus July 2008 price of $371,427. Tighter market

and also eclipsed the best previous conditions in terms of inventory have

July in history by a full 12% helped propel resale prices recently. For

(July 2007 - 8,912 units sold). This is the example, the number of active listings

third consecutive month of renewed on the market declined by 36%

volume growth and is indicative of between the end of July 2009 and the

reinvigorated buyer enthusiasm as a

result of improved housing affordability.

end of July 2008 (16,915 vs. 26,543).

Further evidence of the strengthening

Mortgage

The turnaround in volume over the

past three months has resulted in

market can be found in the rapidly

plunging number of days required to

Rate Watch

year-to-date numbers virtually on par sell a property - which stood at just 31

with 2008 levels and, with five months days in July. This is the lowest monthly Posted Rates – Aug 8/09

remaining in 2009, it is highly probable “days on market” number since May

that full year sales will be at or above 2008 and one of the lowest ever for Closed Mortgages

last year’s figures. the resale market.

1 year 3.90%

2 year 4.05%

3 year 4.55%

Units Sold GTA Resale Home Sales - July 4 year 5.24%

12,000 5 year 5.79%

10,000 Open Mortgages

8,000

6 month 6.55%

6,000

1 year 6.55%

4,000

The above rates are accurate at the specified date and

2,000

have been supplied by a major bank. There may be

Avg Price $342,034 $366,012 $371,427 $395,414 variations in rates between different financial lending

institutions, and rates are negotiable with individual

lenders. To obtain up-to-date posted rates for all financial

2006 2007 2008 2009 institutions, please consult www.cannex.com.

2. Understanding your credit history

Personal

Finance

Regardless of what stage you are in life, you are almost

certain to be a user of credit in one fashion or another. Along

with the use of credit comes a credit history that individual Many applicants are surprised to learn that lenders establish

consumers need to really understand. very specific guidelines on what mortgage rates they will

offer and it is usually based on an applicant’s credit score.

If you own a credit card, have a line of credit or a car loan,

you have a credit history and it is being recorded in a credit Take the time to understand how you can achieve and

report by credit reporting agencies, Equifax, Trans Union or maintain the best credit score. When it is time for you to

Northern Credit Bureaus. These credit reporting agencies renew your mortgage financing in the future, you will be

collect information on your ongoing use of credit and your able to qualify for the best mortgage rates.

repayment of that debt. As you continue to utilize your

Here are some quick tips to help you:

credit cards, pay your car loan or your line of credit, you

will be assigned something called a “credit score”. A credit 1. Be sure to pay your bills on time.

score is a numerical scoring measurement of an individual’s 2. Avoid exceeding your credit limits.

use of credit, specifically repayment of debt. A higher score 3. Avoid having too much available credit.

would indicate a borrower has better management of their

consumer debt while a lower score would indicate poor 4. You should always know, validate and protect your credit

management of consumer debt. There are several factors rating as much as your SIN number and credit cards.

that can affect your credit score, for example, whether you 5. You can check your credit rating for accuracy once a

pay your debts on time, the total amounts that you owe, year free of charge. Just call Equifax at 1-800-465-7166

delinquent payments, collections that may have been filed or go on-line at www.equifax.ca and fill out the form at

against you or limits that have been exceeded or “maxed www.equifax.com/EFX_Canada/consumer_information_

out”. centre/docs/request_report_form_e.pdf or you can purchase

a copy of your credit report online.

If you currently have a mortgage or will be applying

for mortgage financing, you may know that mortgage 6. If you find any information on your credit report that

lenders will want to see your credit report. You will need is not accurate, you should contact the Credit Reporting

to provide permission to the bank or mortgage broker to Agency to have it corrected.

retrieve your consumer credit report for review, at the time 7. Be sure to download a copy of the document entitled

of your application for a mortgage. Once the credit report “Understanding Your Credit Report and Credit Score”

is retrieved, it will be carefully reviewed by the lender to published by the Financial Consumer Agency of Canada by

determine what mortgage rates you are eligible to receive. going to www.fcac-acfc.gc.ca

3. Condo Act provisions to be aware of

Condo

Provision One: Under the new Condominium Act, buyers

of brand new units have 10 days to cancel their contract

Corner

when the builder wants to apply those funds towards

construction costs. For years it was unclear at whose

after receiving the accepted offer from the builder. That expense. According to the new act’s regulations, condo

10-day “cooling-off” period allows purchasers to carefully builders must pay the fee for excess deposit insurance,

examine the offer and disclosure statement, and discuss “and shall not directly or indirectly transfer the cost of the

their content with a real estate lawyer. Though disclosure premiums” to consumers.

statements are foreign to new home transactions, contracts

for both new homes and condos are lengthy and complex, Provision Five: Reservation agreements are quite common

liberally sprinkled with hefty charges and unusual clauses. in both new condo and new home projects. Builders may

test the market before making any final decision to proceed.

Provision Two: Developers under the new Condominium

Or builders can “hold” a unit or lot once sales are underway,

Act must pay interest on deposits “calculated from the

until the purchaser is ready to submit a formal offer. Either

day the person pays the money received until the day the

way, no rules previously governed reservation fees.

proposed unit is available for possession.”

According to the regulations, the interest rate is a set Traditionally they were paid directly to builders. Sometimes

formula (the Bank of Canada bank rate less 2%, reset March they were non-refundable, even when a buyer proceeded

31st and September 30th for the next six months). That with the purchase. The new Condominium Act equates

obligation exists “despite any agreement to the contrary.” reservation fees with deposits. Besides being payable to the

Until the new act became law, few condo developers paid builder’s lawyer or an escrow agent in trust, buyers who

interest on deposits before interim closing. purchase the unit must be credited with the amount paid.

Provision Three: Unlike the old legislation, condo builders Provision Six: Under the new Condominium Act, if there

can’t receive and hold deposits anymore. Instead, deposits is a “material change” to the information in a disclosure

must be paid to the builder’s lawyer or an escrow agent in statement, buyers get a fresh 10-day cooling-off period

trust. Few resale home sellers receive and retain deposits

to opt out of the deal. “Material change” is defined as a

either. Generally they are paid to the listing broker or the

change or series of changes that a reasonable purchaser,

seller’s lawyer in trust.

acting objectively, would regard as sufficiently important

Provision Four: Excess deposit insurance has long been “that it is likely that the purchaser would not have entered

available to protect condo deposits that exceed $20,000, into an agreement of purchase and sale for the unit.”