Workshop 2: Tipping Point Analysis Preview ("From the Fund Management Jungle: Value Investing Exposed and Explored" Workshop Series)

•

3 gefällt mir•3,413 views

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie Workshop 2: Tipping Point Analysis Preview ("From the Fund Management Jungle: Value Investing Exposed and Explored" Workshop Series)

Ähnlich wie Workshop 2: Tipping Point Analysis Preview ("From the Fund Management Jungle: Value Investing Exposed and Explored" Workshop Series) (20)

Mehr von Koon Boon KEE

Mehr von Koon Boon KEE (18)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Workshop 2: Tipping Point Analysis Preview ("From the Fund Management Jungle: Value Investing Exposed and Explored" Workshop Series)

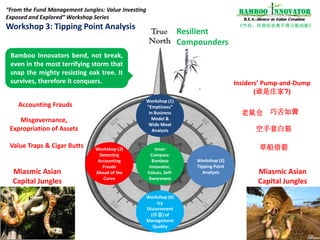

- 1. 1 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation Resilient Compounders Workshop (2) Detecting Accounting Frauds Ahead of the Curve Workshop (3) Tipping Point Analysis Workshop (4) Icy Discernment (冰鉴) of Management Quality Inner Compass: Bamboo Innovator, Values, Self- Awareness “From the Fund Management Jungles: Value Investing Exposed and Explored” Workshop Series Workshop 3: Tipping Point Analysis Accounting Frauds Value Traps & Cigar Butts Misgovernance, Expropriation of Assets Miasmic Asian Capital Jungles Miasmic Asian Capital Jungles 空手套白狼 草船借箭 老鼠仓 巧舌如簧 Insiders’ Pump-and-Dump (谁是庄家?) Bamboo Innovators bend, not break, even in the most terrifying storm that snap the mighty resisting oak tree. It survives, therefore it conquers. Workshop (1) “Emptiness” in Business Model & Wide Moat Analysis

- 2. 2 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation Waiting can be the poison in value investing and tipping point analysis is the antidote. Investors often lose patience and conviction with their stocks when they don’t perform in the short-term to produce a feel-good comfort that we are right in our stock calls. That’s why fund managers under pressure to deliver short-term results always ask their sell-side analysts or the management, “Any upcoming catalysts?” This cannot be more misleading when there is an insufficient understanding in the scalability and resilience of the underlying business model. This is critical because a lot of “catalysts” such as corporate news announcement of “sexy” projects or M&As are, in fact, false signals created and released by “insiders” (庄家) to inject “action” into the stock, luring investors in and then offloading to them in a pump-and-dump cycle. Serious institutional investors spend most of their time not in looking at stock price screens or gaining “insider” knowledge of “catalysts” to generate alpha or excess returns, but in analyzing the interaction of business model dynamics with “tipping point” events so that they literally hear and see the “clicking” sound when they occur to produce a resilient compounder. Value investors need to have a systematic framework to understand and identify “tipping point” events when they occur to stay ahead of the momentum traders and colluding insiders on the investing curve. Catalyst Vs Click/Tipping Point

- 3. 3 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation How Do “Can Make Money or Not” Loud-Mouthed Flashy Fund Managers Use “Catalyst” Signals In Investing From the US Attorney: “On the evening of July 9, 2009, AGGARWAL learned from a friend who was an employee of Microsoft that discussions about the Partnership had recommenced and that a transaction was likely within the next few weeks. The next day, AGGARWAL provided information about the Partnership to at least two different hedge funds, including to Richard Lee, then a portfolio manager at SAC Capital Advisors LP. On July 10, 2009, AGGARWAL told Lee, in substance, that he had heard from a source – whom AGGARWAL described as “a senior guy at Microsoft” – that (a) senior Yahoo executives had been meeting with senior Microsoft executives at Microsoft’s offices; (b) senior Microsoft executives were making requests for information that suggested to the sources that a deal was likely to be completed soon; (c) the success of Microsoft’s Bing search engine had caused Yahoo to move closer to Microsoft’s offer; and (d) it was likely that the deal could be announced within the next two weeks. Thereafter, Lee’s hedge fund purchased several hundred thousand shares of Yahoo stock, and Lee purchased 25,000 shares of Yahoo stock in his personal account.”

- 4. 4 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation How Do Serious Low-Profile Institutional Fund Managers Use “Catalyst” Signals In Investing – Norway’s SWF How did Norwegian sovereign wealth fund (SWF) grow from an initial funding of $300 million in May 1996 to over $700 billion in assets? GIC Policy Portfolio US$700B US$500B Oil Inflow + US$200B Returns = US$700B AUM NBIM’s Simple 60-40 Asset Allocation Changes in value since first capital inflow in 1996

- 5. 5 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation How Do Serious Low-Profile Institutional Fund Managers Use “Catalyst” Signals In Investing – Norway’s SWF Conversation with NBIM Head of Equity Asset Strategies (EAS), one of the four departments in Equity managing the global equity investments: The bulk of NBIM’s assets in equities investments are managed using active indexing strategies with firm-specific event-driven analysis. T = 0 “Announcement date” (AD): Announcement of stock inclusion or deletion in index “Inclusion/deletion date” (ID): Actual date of inclusion/deletion T + 14 to 60 to 720 daysT – 20 days Catalyst: Do stock price go up or down at announcement date? Possible to predict the catalyst? Who enters or exits the index? Random or deliberate decision? Do the returns persist at the actual date? Effect on industry counterparts?

- 6. 6 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation This figure shows the average cumulative returns (top line) for the cumulative raw returns in excess of the value-weighted market index (bottom line) from the 20 days before to 60 days after the stock enters the S&P index. Day zero represents the date on which the stock was added to the index. The sample consist of 36 stocks that entered the S&P 500 from 1977 to 1999. How Do Serious Low-Profile Institutional Fund Managers Use “Catalyst” Signals In Investing – Norway’s SWF “… much of the loss in Hong Kong was due to an 8.7% plunge by property giant Cheung Kong Holdings, which will be deleted from the MSCI Hong Kong Index… On the winning side was Pacific Century Works Ltd. The internet company rose more than 5% after MSCI said it will be included in the MSCI Hong Kong Index.” - Wall Street Journal, May 19, 2000

- 7. 7 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation How Do Serious Low-Profile Institutional Fund Managers Use “Catalyst” Signals In Investing – Norway’s SWF Inclusion in index might convey positive info about the longevity and prospects of that firm because of the certification effect Greater interest in the firms included in index could lead to the expectation of higher future cashflows and these firms may be forced to perform more efficiently and make more value-enhancing decisions if monitoring by investors and analysts become more effective Membership in the index may also increase the ability of firms to attract new capital if financial institutions or investors are more willing to lend to firms in the index. The additional capital may enable the company to grow at a rate higher than the rate prior to the inclusion in the index The original pioneering work in 1986 by Andrei Shleifer Prior to Sep 1976, the announcement of changes did not include the actual dates on which they were made. Empirical research that’s part of your CFA Paper 3 Exam (probably the only practical critical thinking part of the CFA)

- 8. 8 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value CreationIHH Healthcare Bhd (IHH SP): Inclusion Into STI Index Sep 12: S$1.245 Announcement Date (AD): Sep 13 “Asia’s largest health-care operator IHH Healthcare is replacing container carrier Neptune Orient Lines as one of the 30 component stocks in the benchmark Straits Times Index come Sept 24. Following Thursday's review, the next five companies ranked highest on the same basis as the STI companies in order of market value are Hutchison Port Holdings Trust, Keppel Land, Ascendas Real Estate Investment Trust, UOL Group and CapitaCommercial Trust. These five counters will be kept on the STI reserve list and will replace any STI constituents that become ineligible as a result of corporate actions before the next review. In addition, new quarterly reviews of the indices, including the STI, will be introduced in June and December to fast-track the inclusion of eligible IPO stocks. The first quarterly IPO review will occur in December.” - Straits Times, Sep 13, 2012 Note: From Jan 1, 2008, the old STI index of 50 stocks is replaced by a new FTSE STI index of 30 stocks and 18 new indices. The change is announced in Oct 2007. STI IHH

- 9. 9 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value CreationNOL: Deletion from STI Index “Asia’s largest health-care operator IHH Healthcare is replacing container carrier Neptune Orient Lines as one of the 30 component stocks in the benchmark Straits Times Index come Sept 24. Following Thursday's review, the next five companies ranked highest on the same basis as the STI companies in order of market value are Hutchison Port Holdings Trust, Keppel Land, Ascendas Real Estate Investment Trust, UOL Group and CapitaCommercial Trust. These five counters will be kept on the STI reserve list and will replace any STI constituents that become ineligible as a result of corporate actions before the next review. In addition, new quarterly reviews of the indices, including the STI, will be introduced in June and December to fast-track the inclusion of eligible IPO stocks. The first quarterly IPO review will occur in December.” - Straits Times, Sep 13, 2012 NOL STI

- 10. 10 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value CreationGLP: Inclusion Into STI Index “Global Logistic Properties will replace SMRT Corp as a constituent of the Straits Times Index (STI) following the conclusion of its half-yearly review. SMRT Corp will join the FTSE ST Mid-Cap Index. All changes from this review will take effect from the start of trading on 21 March 2011. The next review is scheduled for 8 September 2011.” - Financial Times, Mar 10, 2011 STI GLP

- 11. 11 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value CreationSMRT: Deletion from STI Index “Global Logistic Properties will replace SMRT Corp as a constituent of the Straits Times Index (STI) following the conclusion of its half-yearly review. SMRT Corp will join the FTSE ST Mid-Cap Index. All changes from this review will take effect from the start of trading on 21 March 2011. The next review is scheduled for 8 September 2011.” - Financial Times, Mar 10, 2011 SMRT STI

- 12. 12 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation CapitaMalls Asia (CMA SP): Inclusion Into STI Index Not Foolproof: The Seduction and Limitation of Catalysts “CapitaMalls Asia shares rose to a two-month high in Singaporean trading after the company was chosen to replace Cosco Corp. Singapore in the Straits Times Index following the conclusion of a half-yearly review, reported Bloomberg. The changes will take effect from March 22. Fund managers who benchmark their holdings of Singaporean equities against the Straits Times typically buy additions and sell deletions in order to mirror the stock index. CapitaMalls Asia, a unit of Southeast Asia’s biggest developer CapitaLand, gained 1.3% to $2.37 today, the highest level since Jan 14. Cosco Corp., China’s second- largest publicly traded shipbuilder, lost 2.4% to $1.23. CapitaMalls Asia, which owns and operates shopping malls in the Pacific Rim and India, has a market value of $9.2 billion, according to data compiled by Bloomberg. CapitaMalls Asia on Feb 3 reported full-year profit after tax and minority interest of $388 million, more than triple the previous year’s $116 million. The company is 66% owned by CapitaLand.” - Bloomberg, Mar 12, 2010 CMA STI Catalysts cannot overcome longer-term business fundamentals and prospects

- 13. 13 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation Singapore’s Goodpack: Inclusion of Lanxess (Goodpack’s Key Customer) Into German DAX Index The Seduction and Limitation of Catalysts + Understand Intra-Industry Spillover Analysis “Lanxess Cuts 2014 Profit Forecast Amid No Sign of Recovery: Lanxess AG (LXS), which until today had lost 30 percent since joining Germany’s benchmark DAX index in September, cut its profit forecast for 2014 as it sees no sign of a demand recovery in the second half of this year. Lanxess, based in Cologne, Germany, has been cutting costs as clients continue to reduce inventories, especially in Asia, and it already idled factories in the first half to counter falling demand from the auto industry. - Bloomberg, Aug 6, 2013 Goodpack Lanxess Lanxess Goodpack STI Intra-industry spillover analysis is important

- 14. 14 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value CreationCatalyst or Event-Driven Investing Event Driven (19%): Twenty years ago these funds mainly practiced a form of investing called risk-arbitrage. Example: If a company announced an acquisition, the “arbs” would buy shares of the seller (which would rise), short the buyer’s shares (which would fall, temporarily) and capture the spread. Today this group hunts for all sorts of “events” that could move a company’s stock—catalysts like a change in the corner office, a merger with a competitor, the spin-off of a division, looming litigation, a major debt restructuring or even a bankruptcy filing. Conversation with NBIM Head of Equity Asset Strategies (EAS), one of the four departments in Equity managing the global equity investments: Most of the NBIM guys can understand the empirical research papers and we try to come up with original practical applications. We refine our know- how over the years and we openly share the process and findings with one another. Our culture is about winning together with a shared process and not about slapping a “team” label of star fund managers or dealmakers. Outcome of corporate events is often not linked to economic conditions, thus offering potential de-correlated returns Major risk: Credit- and distressed-driven events can blow up big-time even with clever structuring

- 15. 15 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation How to Make Sense of Catalysts? Fireflies Before the Storm? Financial Non-Financial Bonus, Rights, Share buyback, Share split, Warrants Capital reduction program Equity or debt placement (IPO, SEO – secondary equity offering, CB, MTN etc) Financial structure changes (commitment plan on debt equity ratio) 1) Accruals Initiation of coverage, stopping coverage, changes in recommendation and target prices, forecast revisions, commentary NDR (Non-deal roadshow), Conference 1) Analyst Turnover of management, director, ID, board governance committee, auditor, banker, adviser Management compensation (incentive plan, bonus, share options, share awards) Sudden CEO or founder death 2) KAH (key appointment holder) changes Contract or project updates, Orderbook, Operating results Investments in R&D, capex, capacity, deal New or lost of product/service, market, customer, supplier, partner ASP increase or decrease Patents, Research trial completion RPT (related-party transactions) Credit rating changes 5) Corporate news M&A, Spinoff, Reverse merger, Takeover JV, Partnership, Strategic alliance, Licensing agreements, MoU Asset injection/transfer/disposal Restructuring MBO/LBO Litigation, Contingent liabilities event Regulatory shock 7) Significant corporate events 3) Ownership changes Considerations: What is disclosed: Categorize by “good” and “bad” news? Overreaction to “good” news, underreaction to “bad” news? Buy on “bad” news, Sell on “good” news? How it’s disclosed: Categorize by sentiment/tone/confidence? Voluntary or mandatory? When it’s disclosed: Scheduled or unscheduled? Bunching, sequencing or spread out? Why it’s disclosed: Why will management disclose “bad” news? Is the info content transitory or persistent? Do false news have persistent effects? Are investors desensitized by catalysts? In what situation are positive catalysts misleading noise e.g. insider purchase can be negative 4) Industry, intra-industry or contagion effect Customers, suppliers, stakeholders, partners Subsidiaries, associates, affiliates Revenue and Cost driver shock: “If it’s raining in Brazil, Buy Starbucks” Insider buy/sell Strategic shareholder4) Others Restatement Change in accounting policy Change in fiscal year Index inclusion or deletion Expiry of moratorium or lock-up period Dual-listing 6) Special events 3) Capital management Initiation, Changes, Omission, Resumption, One-off special PEAD (Post-Earnings Announcement Drift) 2) Dividends

- 16. 16 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation What is the Relationship Between Business Model/Moat & Tipping Point Analysis? MOAT Share Price Has Already

- 17. 17 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation “Wouldn’t it be nice if we can invest BEFORE the economic moat is obvious?” Key challenge: Stocks are categorized into moats AFTER they are obvious… “Our advantage is intimately linked to categorization through analogy, a mental mechanism that lies at the very center of human thought but at the furthest fringes of most attempts to realize artificial cognition. It is only thanks to this mental mechanism that human thoughts, despite their slowness and vagueness, are generally reliable, relevant, and insight-giving, whereas computer “thoughts” are extremely fragile, brittle and limited, despite their enormous rapidity and precision.” – Hofstadter and Sander in “Surface and Essences: Analogy as the Fuel and Fire of Thought”

- 18. 18 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation Lollapalooza! How Do Buffett-Like Value Investors Use Tipping Point? Different Tipping Points in Business Models Extreme success is likely to be caused by some combination of the following factors Extreme maxi/ mini of one or two variables Extreme of good performance over many factors Catching and riding some sort of big wave Lollapalooza “Adding success factors, so that a bigger combination drives success, often in non- linear fashion, as one is reminded by the concept of breakpoint and the concept of critical mass in physics. Often, the results are not linear. You get a little bit more mass, and you get a lollapalooza result.”

- 19. 19 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation Apple: Catalyst (Oct 2011, iPod) Vs Tipping Point (Apr 2003) Up 68-fold since April 2003 to $410B Dec 1996 – Sep 2001 Steve Jobs returns Apple +49% Nasdaq +32% Oct 2001 – Mar 2003 Launch of iPod Apple -26% Nasdaq -16% Apr 2003 – Now Launch of iTunes Apple +68X Nasdaq +153% Apple +126X Nasdaq +17.8X Tipping Point! Tipping Points? 1998: S$100b

- 20. 20 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation Program Outline and Key Learning Points: UNDERSTAND the stock market reactions to a wide-range of “catalysts”: “Post-earnings announcement drift (PEAD)”, “Capital management programs” (e.g. dividends, capital reduction, share buybacks, bonus issue, rights, splits, share/debt placement) and “Financial structure changes”, “Analyst coverage and recommendations”, and many more. GAIN the surprising insight to why certain positive catalyst signals can be misleading noise, for instance, insider purchase can be negative. And also why overreaction to certain negative catalyst signals can be an opportunity. DEVELOP the ability to distinguish between “catalysts” with unsustainable short-term effects and “tipping point” with long-term value relevance. LEARN where M&A pays and where it strays and the pitfalls. DISSECT a wide range of real-world cases of Asian and global Bamboo Innovators in various industries and understand the tipping point in their business models. UNIFY at the end of the day all the previously disparate loose-hanging concepts, descriptive facts and “checklists” you have learnt from various sources into the practical Bamboo Innovator mental model when it comes to real investment decision-making.

- 21. 21 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation “In business, I look for economic castles protected by unbreachable ‘moats’.” - Warren Buffett With unresolved crises on the horizon, investors are often immobilized in making investment decision. “Wait for the clouds to clear” is the mantra. Value investing appears to provide a way out to see opportunities in cloudy weather by using the “cheap” price signal to identify “out-of-favor” neglected stocks and invest in them for “reversion back to mean”. Hence, pick stocks with “cheap” valuations based on conventional metrics and ratios – how much lower can they go anyway? – and they will bounce back up to their historical average levels. Or simply wait for a market dip, or a crash, before declaring some magical list of top ten stock tips to invest in. This is NOT value investing. When Li Ning, the “Nike of China”, announced that its founder is going into industrial park and property development in September 2010, the stock has been a darling, having a competitive “moat” with brand recognition and it has recovered strongly since its bottom in March 2009 by climbing 140% to HK$24 per share. Oh, it is already expected that the market will react negatively to the property news, now it is down 20% to HK$19, value stock, be contrarian, BUY! Down another 20% to HK$15, getting cheaper and it’s out-of-favor, it will bounce back up, BUY! And the value investor catches the falling knife until below HK$5 now; while Nike hits an all-time high. How do value investors distinguish whether “cheap” stocks are value traps or opportunity? Without an understanding of the underlying business model dynamics and analyzing the durability of the economic moat, an investment decision based on price and macro signals and historical valuation metrics can be misleading and costly. Without an understanding of business model, one would also have sold Wal-mart after it was listed in 1972 as the stock crashed over 60% in the next three years. Wal-mart went on to compound 1,200-fold since 1972 to over US$250 billion in market cap – a $100,000 investment in Wal-Mart becomes a $120 million treasure trove. So why is Wal-mart able to bounce back to scale new heights but the same cannot be said for the “Nike of China”? Can resilient business models – Bamboo Innovators - outperform even in stormy periods? When Shanghai Composite Index crashed 70% from its peak of 6,000 in October 2007 to below 2,000 at the bottom in March 2009, Yunnan Baiyao was UP around 8%. As the index bounce to 2,200, still down 60% from its peak, Baiyao is up over 220% during the same period. Increasingly, such resilient business models are outperforming in Asia and globally; while the “cheap” stocks get cheaper and they become the fertile ground for “insiders” (庄家) who manipulate prices and volumes and inject “action” via exciting corporate news announcement of “sexy” projects or M&As, luring investors in and then offloading to them in a pump-and-dump cycle. Sophisticated value investors can overcome poor and uncertain macro conditions by investing in resilient compounders because they have their own internal rhythm to create value, like the bamboo, which bend, not break even in the wildest of storm that would have snapped the once-mighty oak tree. Workshop 1 of 4: In Search of Compounding Stocks in Uncertain Times

- 22. 22 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation Program Outline and Key Learning Points: LEARN the R.E.S.-ilience factors in the business model and economic moat analysis of how Bamboo Innovators create extraordinary value, particularly the “E” factor which stands for “emptiness” in the business model. GAIN the surprising insight of sophisticated institutional investors who understand why growth in sales, profit and tangible asset may not translate to market capitalization growth and sustainable share price gains. ATTAIN the critical knowledge of 12 types of sophisticated institutional investors that climbing from $50 million to $1 billion in market cap takes an entirely different business model dynamics as compared to scaling up sustainably from $1 billion to $20 billion in market cap. RECOGNIZE the 12 types of business models and their profit patterns and acquire the ability to scan through different businesses in various industries to understand the key levers for growth ahead of the investment curve. UNDERSTAND why and how businesses hit a stall point in growth and without a transformation in business model, bigger can be riskier. Thus “Grow or Perish” become “Grow AND Perish” DISSECT a wide range of real-world cases of Asian and global Bamboo Innovators in various industries and understand the intricacies of their business models, their critical success – and failure – factors. UNIFY at the end of the day all the previously disparate loose-hanging concepts, descriptive facts and “checklists” you have learnt from various sources into the practical Bamboo Innovator mental model when it comes to real investment decision-making.

- 23. 23 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation Frauds. Warren Buffett commented in the recent Berkshire Hathaway AGM 2013 that when he’s reading through financial statements, he’d find companies he was virtually certain are frauds. In response to a shareholder’s question on what did he find that made him so certain, both Buffett and Munger replied that “there isn’t a 40-point checklist” and that value investors need to understand the interaction between the underlying business model dynamics and the people running the enterprise when examining the numbers. In Asia, with outbreaks of accounting frauds and corporate governance lapse erupting on a systematic basis at the firm level, how does a value investor go about generating sustainable outsized returns? To paraphrase Sherlock Holmes, to murder (to engage in earnings management) is easy, but to dispose the murdered body (to expropriate or tunnel out the cash and assets out of the company) is harder as it is detectable by the serious institutional investor with his or her keen observation of the various information signals and clues. It would be premature to speak of “fundamental” analysis using possibly rigged accounting numbers due to propping and tunneling to fashion elaborate but “garbage-in-garbage-out” quant valuation models. Even “technical” analysis can be misleading given prices and volumes are often manipulated by the “insiders” (庄家) who establish the stock inventory (老鼠仓), luring investors in and then offloading in a pump-and-dump cycle. Such exploits by insiders is made easy as most stocks in Asia are still relatively small-cap and illiquid, given that the median market cap of the listed universe of 23,000 stocks in Asia is around $80 million and over 80% are under a billion dollar in market cap. Thus, the use of “fundamental” or “technical” analysis, or its combination – without a Mungerian I-O accounting framework using the Bamboo Innovator way – can lead to a false sense of confidence that clever insiders exploit at your expense. Workshop 2 of 4: Detecting Frauds Ahead of the Curve

- 24. 24 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation Program Outline and Key Learning Points: UNDERSTAND the importance of the Mungerian I-O (Incentive-Opportunity) accounting framework to adapt value investing principles in Asia. LEARN the three accounting steps that “set-up” companies commonly use to expropriate assets and the ORECTA and other information signals that sophisticated institutional investors use in their cutting-edge empirical research tool-bag. DEVELOP the ability to scan through thick annual reports and financial statements for the Seven Accounting Sins. DEMYSTIFY the various techniques in “earnings management”, “revenue recognition management”, “real activity management” and “income smoothing” and differentiate between opportunistic bookkeeping mischief and discretionary signaling of private information of leading indicators of firm performance by management to investors. ATTAIN the application tools used by sophisticated institutional investors in the accounting of words, that is, textual analysis of disclosures which are an important source of information with value relevance about the firm. DISSECT actual cases of capex-related fraud in prominent Asian listed companies that are invested by reputable fund management institutions who are also caught flat-footed when things unravel. RE-EXAMINE accounting fundamentals that universities impart without the relevant context of value investing, including the use and abuse of the accruals anomaly (AA) in investing strategies adopted by sophisticated institutional investors in various forms. UNIFY at the end of the day all the previously disparate loose-hanging concepts, “descriptive” facts and “checklists” you have learnt from various sources into the practical Bamboo Innovator mental model when it comes to real investment decision-making.

- 25. 25 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation Outline and Key Benefits: •LEARN the application tools and techniques used by sophisticated institutional investors in the accounting of words, that is, textual analysis of disclosures which are an important source of information with value relevance about the firm. •UNDERSTAND the framework to sense and detect the quality of management and corporate governance, how leaders are better (or worse) under pressure and bring out the best (or worse) in themselves and others during difficult times. •DEVELOP the insight using the Bamboo Innovator framework of how “Sheath” leadership encourage and protect the emergence of innovative ideas and how they cultivate “Rootedness” in the corporate culture to be trusting and ready to risk in new innovations. •ATTAIN the knowledge of what to look out for when investing in family-controlled businesses to assess the opportunities and pitfalls. •ADAPT the ancient Chinese wisdom of “Icy Discernment” by people-reader Zeng Guofan to view management quality afresh. •UNIFY at the end of the day all the previously disparate loose-hanging concepts, descriptive facts and “checklists” you have learnt from various sources into the practical Bamboo Innovator mental model when it comes to real investment decision-making. Workshop 4 of 4: Bet on the Jockey (Management) or the Horse (Business Model)?

- 26. 26 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation Published Articles & Research (2013): • Snapped By Regulatory Storms? Braving Through Berkshire’s Former Iron Mountain to Asia, July 31, 2013 (BeyondProxy) • From Buffett’s Scott Fetzer to Asia, Are Oddballs Odious or Opportunities? July 24, 2013 (BeyondProxy) • Are Boring Businesses Resilient or Risky? Pitfalls and Opportunities in Europe and Asia, July 17, 2013 (BeyondProxy) • Supply- and Demand-side Moat Economics in Europe and Asia, July 10, 2013 (BeyondProxy) • “Must-Have” vs “Nice-To-Have”: Exploiting the Sector-Company Gap in Asia, July 3, 2013 (BeyondProxy) • Institutional Imperative and Differentiating Between the Tech Innovators, the Imitators and the Swarming Incompetents in Asia, June 27, 2013 (BeyondProxy) • BNSF + JB Hunt = Buffett + Munger = Lollapalooza! How About Asia? June 19, 2013 (BeyondProxy) • Why Berkshire Hathaway’s McLane Has a Moat, and Are There Similar Companies In Asia? June 12, 2013 (BeyondProxy) • Investing in Korea: Staying Rational Despite Samsung’s Halo Effect, June 5, 2013 (BeyondProxy) • Education 2.0 In Indonesia: Inspiring Bamboo Innovators, May 11, 2013 (Jakarta Post) • Any Benjamin Franklins in Asia? May 9, 2013 (BeyondProxy) • Berkshire Hathaway 2013: Takeaways and Impressions from the Annual Meeting, May 7, 2013 (BeyondProxy) • Pilgrimage to Omaha + Entrepreneurship, Asian-style! May 1, 2013 (BeyondProxy) • Who’s the Buffett CEO in Asia? Part 1 on China’s Great Wall Motor, April 23, 2016 (BeyondProxy) • Who’s the Buffett CEO in Asia? Part 2 on Australia’s ARB Corporation, April 26, 2013 (Beyond Proxy) • Kewpie: Japan’s Heinz and R.E.S.-ilient Bamboo Innovator, April 20, 2013 (BeyondProxy) • Value Investors in Asia: Making Sense of the Micro Vs. Macro Dilemma, April 16, 2013 (BeyondProxy) • “Be like the bamboo, not the oak tree”, TODAY, 8 April 2013 • “Creating ‘bamboo innovators’ in S’pore”, Straits Times, 1 April 2013 • Detecting Fraud by Scrutinizing the “How” Rather than the “What” of Management Disclosures, March 22, 2013 (BeyondProxy) Featured (2013): • Mental Models: Bamboo Innovator, April 4, 2013 (BeyondProxy) • The Bamboo Innovator Approach to Investing in Asia, April 4, 2013 (YouTube uploaded by BeyondProxy.com) • Six Common Accounting Pitfalls at Asian Companies, March 20, 2013 (BeyondProxy) • Insights into Accounting Pitfalls at Asian Companies, March 21, 2013 (Greatinvestors.TV and Frequency.com) • Beware of “Other Receivables” Accounting at Asian Companies, March 26, 2013 (Greatinvestors.TV) Internationally Featured Value Investor: TEDxWallStreet, BeyondProxy, GreatInvestors.TV

- 27. 27 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation Some Testimonial From Public Workshop “I enjoyed today's course. Thanks in particular for having extensively prepared the notes with examples and for sharing with us your anecdotes on various CEOs and top executives in Singapore. I found such opinions useful since many of us do not have access to a company's management outside of a shareholders' meeting so it is difficult to get a better sense of the management's true character. I also found your 3-point Bamboo Innovators Search Methodology a useful litmus test in filtering companies for further value analysis. Thanks again for the course and I hope to see you in a future course soon.” Charles Guo “It has been mind-blowing learning from you. The amount of knowledge you shared is so intensive that I went home and slept till the next day. The case studies you shared were great.” Johnny Lee “You have gave a great lecture yesterday, it was certainly worth spending an entire Saturday for the course. The things that you have taught is truly unique and thought- provoking just like your articles on BeyondProxy. The Bamboo Innovator framework has allowed me to use a more holistic approach towards investing.” Yeo Shan Rui

- 28. 28 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation “It has been an interesting and encouraging program. The program has encouraged me to continue to pursue what I want to do for the company.” Jismyl Teo Chor Khin, CEO of DMX Technologies Limited “The content and substance of the Program is original, useful and important. This program challenged me intellectually and helped me to think critically and learn more effectively. Overall, I find the Program beneficial to me and my company (rated 5 out of 5).” Sherlie Young, Senior Manager (Group Finance) of Gallant Ventures Limited “The program gives a new and refreshing perspective of how companies can be successful and it is backed by a lot of research with a practical, real-world approach.” “The Program Director is approachable, authentic and helpful when sharing his insights. Overall, I would highly recommend this Program to my colleagues and peers (rated 5 out of 5).” Danny Tan, Manager (Group Finance) of Gallant Ventures Limited “It is an eye opener for me. With this seminar, I can learn about how companies scale up successfully.” Ratnawati, Corporate Accounts Manager of Gallant Ventures Limited “I have increased my knowledge as a result of taking this Program.” “Overall, I find the Program beneficial to me and my company and I would highly recommend this Program to my colleagues and peers (rated 5 out of 5).” Sun Yi, Managing Director of Sunnic Pte Ltd Some Testimonial From Corporate Workshop

- 29. 29 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value Creation Bamboo: The hardiest and effective natural structure to evolve in millions of years of restless experiment in cellular life on earth Even through the strongest hurricanes, the bamboo will bend but never break; when covered with snow, it will patiently wait for it to melt down, and then rise up. And in the end, the bamboo stands tall, green and beautiful. For the Chinese, the bamboo represents the value of “uprightness”. Bamboo is an ancient resident of earth, here before people by some 100 to 200 million years. Its “root-like” rhizome and “hollow” culm is perhaps the hardiest and effective natural structure to evolve in millions of years of restless experiment in cellular life on earth, and the most efficient laboratory that has yet appeared for braiding sunlight, water, and soil into forms which have for centuries proved immensely useful for human needs. The bamboo culm combines a certain gentle capacity to yield with a strength that rivals steel. 52,000 pounds per square inch were required to break a good bamboo. Walnut required 22,000 pounds per square inch, while the steel commonly used for reinforcing concrete required about 60,000 pounds. Bamboos bend, not break, and remain evergreen even with the onslaught of the atomic bomb. The world’s first atomic bomb over the city of Hiroshima on August 6, 1945, has destroyed streets and houses, charred trees and grasses to bits. Yet, one living thing stood out. In the very epicenter, a thicket of bamboo stood through the blast, suffering only one side to be scorched. The sight was an immeasurable encouragement to the war- shattered citizens. A portion of the bamboo plant is now housed in the Memorial Museum for Peace.

- 30. 30 《竹经:经商经世离不得立根创新》 nnovatorBamboo R.E.S.-ilience in Value CreationContact KB Kee “Give me a lever long enough and a place to stand and I’ll move the world,” says Archimedes. The long lever we choose to innovate in the world is hopefully the Bamboo; the place where we stand is Emptiness - when we empty our heart of prejudices, pride and fear, we become open to the possibilities to innovate – and Emptiness is rooted in Kindness and Trust. Bamboo Innovator Institute is set up to establish the thought leadership of resilient value creators around the world. Koon Boon has been rooted in the principles of value investing for over a decade as a fund manager and analyst in the Asian capital markets. He was a fund manager and head of research/analyst at a Singapore-based investment management organization dedicated to the craft of value investing in Asia. He had been with the firm since 2002 and was also part of the core investment committee in significantly outperforming the index in the 10-year-plus flagship Asian fund. He was previously the portfolio manager for Asia-Pacific equities at Korea’s largest mutual fund company. He received his Masters in Finance (magna cum laude) and double degree in Accountancy and Business Management (both summa cum laude) from the Singapore Management University (SMU). He had taught accounting at his alma mater in SMU and lectures at SIM University for working professionals. He had published cutting-edge empirical research in the Special Issue of Istanbul Stock Exchange 25th Year Anniversary of the Boğaziçi Journal, Review of Social and Economic Studies, as well as wrote articles about value investing and corporate governance in the media. He had also presented in top banking and finance conferences in Sydney, Cape Town, HK, Beijing and in the recent Emerging Value Summit 2013. He is also an internationally-featured value investor in TEDxWallStreet, Greatinvestors.TV and BeyondProxy.com. He has trained CEOs, entrepreneurs, CFOs, management executives in business strategy, macroeconomic and industry trends in Singapore, HK and China. www.twitter.com/bambooinnovator bambooinnovator@gmail.com www.bambooinnovator.com