1. Economics /

.Mean S Capital Market Perspectives

KBank Strategy

Update on bond supply for Q3 FY2011 FX / Rates

30 March 2011

Bt103.5bn bond supply in Q3 is close to initial estimate; the

actual supply is merely Bt4bn bigger than foreseen last year Nalin Chutchotitham

nalin.c@kasikornbank.com

Key difference is the issuance of Bt30-40 of inflation-linked

bonds that remained unofficial

During our seminar for institutional investors last week, the

director of PDMO clarified that government’s financing needs had

reduced substantially from their initial estimate

We continue to expect policy rate to move up to 3.25% by July

and bond yields on the front-end could rise further, making the

Disclaimer: This report

yield curve flatter in the next quarter must be read with the

Stay with bonds along the mid-curve as long-dated bonds sees Disclaimer on page 6

that forms part of it

little value in an inflationary environment

Q3 bond supply in line with initial estimate

KBank Capital Market

The Ministry of Finance would be issuing a total of Bt103.5bn of bonds in the third

Research can now be

quarter of the fiscal year 2011. The size is close to our initial estimate ($99.5bn) which

accessed on Bloomberg:

had been derived from the PDMO’s (Public Debt Management Office) whole year plan.

KBCM <GO>

The major difference is likely to be the issuance of Bt30-40bn worth of inflation-linked

bonds that remained unofficial despite much news and excitement among the

regulators and investors. We expect that the market would continue to have high

demand for government bonds, due to the high level of liquidity among savers. Foreign

investors’ inflows into the bond market had slowed in recent months but continued to

be observable. An added risk factor to the performance of the bond market is the

increases in fixed deposit rates, which had risen rapidly due to banks’ competition and

loan expansion.

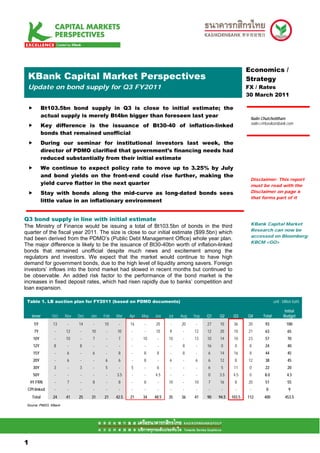

Table 1. LB auction plan for FY2011 (based on PDMO documents) unit : billion baht

Initial

tenor Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Q1 Q2 Q3 Q4 Total Budget

5Y 13 - 14 - 10 - 16 - 20 - 20 - 27 10 36 20 93 100

7Y - 12 - 10 - 10 - - 10 9 - 12 12 20 10 21 63 65

10Y - 10 - 7 - 7 - 10 - 10 - 13 10 14 10 23 57 70

12Y 8 - 8 - - - - - - - 8 - 16 0 0 8 24 40

15Y - 6 - 6 - 8 - 8 8 - 8 - 6 14 16 8 44 45

20Y - 6 - - 6 6 - 8 - 6 - 6 6 12 8 12 38 45

30Y 3 - 3 - 5 - 5 - 6 - - - 6 5 11 0 22 20

50Y - - - - - 3.5 - - 4.5 - - - 0 3.5 4.5 0 8.0 4.5

4Y FRN - 7 - 8 - 8 - 8 - 10 - 10 7 16 8 20 51 55

CPI linked - - - - - - - - - - - - - - - - 0 9

Total 24 41 25 31 21 42.5 21 34 48.5 35 36 41 90 94.5 103.5 112 400 453.5

Source: PMDO, KBank

11

1

3. Reduced financing needs by the government

As shown in Table 3, the government needs less funding compared to the previous two

fiscal years (total financing amounted to Bt537bn, down from Bt661bn in FY2010). In

particular, revenue collection had improved while fiscal spending to stimulate the

economy is spread out between the years as there had been strong economic growth

last year. Furthermore, a significant extent of debt-profile restructuring had been done

during the past two years - PDMO did this by issuing long-dated bonds to refinance Financing needs reduced

short-term debts, effectively lengthening the average time to maturity of the to Bt537bn in FY2011

government’s repayment profile. Hence, the overall supply outlook is positive for the from Bt661bn in FY2010

bond market. In addition, there is still substantial liquidity in the hands of investors. We on economic growth

show in two graphs below the maturing government bonds during the past quarters and

capital inflows from maturing Korean bond funds going forward.

Fig 2. Benchmark bond issuance shows PDMO’s aim for

Fig 1. FY2010 and FY2011 benchmark bond issuance

increasing liquidity in the secondary market

Bt bn Government bond issuance Bt bn Benchmark bond issuance

140 350

120 300

100 93

250

80 63 200

57

60 44 150

38

40 100

22

20 8 50

0 0

5Y 7Y 10Y 15Y 20Y 30Y 50Y FY2008 FY2009 FY2010 FY2011

FY2010 FY2011 5Y 7Y 10Y 15Y 20Y 30Y 50Y

Source: PDMO, KBank’s estimate Source: PDMO, KBank’s estimate

Outlook on bond yields and the policy rate

Backed by the hawkish comments from the Bank of Thailand (please refer to our earlier

piece on MPC minutes or www.bot.or.th), we maintain our call for another three rate Maintain expectation of

hikes during the next three MPC meetings. These hikes would bring the policy rate to 3 more rate hikes by

3.25% by July, 2011. BoT. Target 3.25% by

July

BoT continued to signal a shift of weight to inflationary concerns for its monetary policy

conduct going forward. Vis-à-vis the risks of slower-than-expected growth for Thailand

(Kasikorn Research Center had revised downwards base-case growth for Thailand this

year to 3.6% from 4.5%) in the aftermath of earthquakes and tsunamis in Japan, as

well as higher energy prices due to unrests in the MENA region (Middle-East and North

Africa), it does seem that the central bank prefers an unwavering and preemptive

approach to inflation control.

For asset allocation, we do see higher value in the mid-curve bonds: the front-end is

risky due to continued rate hikes and the long-dated bonds are not attractive in an

inflationary environment. While the supply of 5-year bonds during the next three

months is at Bt36bn, there is sufficient liquidity in the secondary market and a history of We recommend mid-

strong investors’ demand. curve bonds as long-

dated bonds are

In any case, we continue to expect the yield curve to remain in a bear-flattening mode unattractive in an

in the next quarter. The total supply of bonds with maturities of 10-30 years amounts to inflationary environment

a mere Bt45bn, an amount easily absorbed by the market. Furthermore, PDMO’s

director, Mr. Chakkrit Parapuntakul, shared with investors at a KBank seminar for

institutional investors last week that the PDMO would try to manage the supply of

bonds such that borrowing costs do not rise by too much – indicating that the Q4 bond

33

3

4. supply for long-dated bonds could still be reduced from original plan should yields

become unfavorable for the government to borrow.

Fig 7. Maturing government bonds (calendar year) Fig 8. Maturing Korean bond funds (returning liquidity)

Bt bn

Maturing Government loan bonds Bt 90 bn

bn baht 70

61

100 89 60

88

80 70 50 44

40

60

40 30

40

20 14 14 13

9 7 9

20 10 3

3 0

0 0

Q4/2010 Q1/2011 Q2/2011 Q3/2011 Q4/2011 Q1/2012 Apr May Jun Jul Aug Sep Oct Nov Dec

Principal Korean bond funds maturing in 2011

Source: Bloomberg, KBank Source: Bloomberg, KBank

Fig 7. Yield spread 2-5 and 5-10 Fig 8. Forward implied bond curves

bps % Bond yields implied curve shifts

160 4.50

120

4.00

80

3.50

40

3.00

0

Jan-08 Jan-09 Jan-10 Jan-11 Mar-11 Jun-11 Sep-11 Dec-11 tenor (yrs)

2.50

2-5 bond spread 5-10 bond spread 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14

Source: Bloomberg, KBank Source: Bloomberg, KBank

44

4

6. Disclaimer

For private circulation only. The foregoing is for informational purposes only and not to be considered as an offer to buy or

sell, or a solicitation of an offer to buy or sell any security. Although the information herein was obtained from sources we

believe to be reliable, we do not guarantee its accuracy nor do we assume responsibility for any error or mistake contained

herein. Further information on the securities referred to herein may be obtained upon request.

66

6