Beginners Guide to TikTok for Search - Rachel Pearson - We are Tilt __ Bright...

2015 Mid-Market M&A - Transaction Trends f

1. *All report data is based on Factset transaction info

**Mid- Market are companies with revenues <500MM

2015 Mid-Market M&A - Transaction Trends

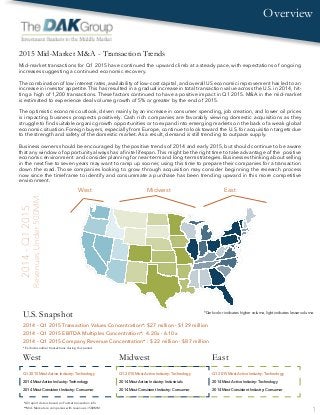

West East

1

Midwest

Overview

Mid-market transactions for Q1 2015 have continued the upward climb at a steady pace, with expectations of ongoing

increases suggesting a continued economic recovery.

The combination of low interest rates, availability of low-cost capital, and overall US economic improvement has led to an

increase in investor appetite. This has resulted in a gradual increase in total transaction value across the U.S. in 2014, hit-

ting a high of 1,200 transactions. These factors continued to have a positive impact in Q1 2015. M&A in the mid-market

is estimated to experience deal volume growth of 5% or greater by the end of 2015.

The optimistic economic outlook, driven mainly by an increase in consumer spending, job creation, and lower oil prices

is impacting business prospects positively. Cash rich companies are favorably viewing domestic acquisitions as they

struggle to find suitable organic growth opportunities or to expand into emerging markets on the back of a weak global

economic situation. Foreign buyers, especially from Europe, continue to look toward the U.S. for acquisition targets due

to the strength and safety of the domestic market. As a result, demand is still trending to outpace supply.

Business owners should be encouraged by the positive trends of 2014 and early 2015, but should continue to be aware

that any window of opportunity always has a finite lifespan. This might be the right time to take advantage of the positive

economic environment and consider planning for near-term and long-term strategies. Businesses thinking about selling

in the next five to seven years may want to ramp up sooner, using this time to prepare their companies for a transaction

down the road. Those companies looking to grow through acquisition may consider beginning the research process

now since the timeframe to identify and consummate a purchase has been trending upward in this more competitive

environment.

*Dark color indicates higher volume, light indicates lesser volume.

2014 Most Active Industry: Technology

2014 Most Consistent Industry: Consumer

2014 Most Active Industry: Industrials

2014 Most Consistent Industry: Consumer

2014 Most Active Industry: Technology

2014 Most Consistent Industry: Consumer

West Midwest East

2014-Q12015

RevenuesUnder500MM

Q1 2015 Most Active Industry: Technology Q1 2015 Most Active Industry: Technology Q1 2015 Most Active Industry: Technology

2014 - Q1 2015 Transaction Values Concentration*: $27 million - $129 million

2014 - Q1 2015 EBITDA Multiples Concentration*: 4.20x - 6.10x

2014 - Q1 2015 Company Revenue Concentration* : $ 22 million - $87 million

U.S. Snapshot

* Excludes outlier transactions during this period.

2. *All report data is based on Factset transaction info

Eastern U.S. Industry Deal Volume

Focus on

Eastern U.S.

Q1 2014 Q1 2015

Q1 2014

Eastern U.S. Industry Average Transaction Value($MM)

Q1 2015

C

onsum

er

Industrials

Technology

The Eastern U.S. is once again leading the country in deal volume for the first quarter of 2015 accounting for 43%

of deals closed across the entire U.S. The Midwest and West regions trailed the East with deal volume of 25%

and 32% respectively.

Broad reaching industry classifications such as manufacturing, distribution and logistics are classified based on

the subsector of focus on a per transaction basis, i.e. transactions involving the manufacturing of food products

are reported in the Consumer subsector.

While aggregate data from the Eastern U.S. supports claims of growth and recovery, not all industries tracked

produced positive trending data in the first quarter of 2015. M&A value growth can be clearly observed in Con-

sumer, Healthcare,Technology, and Utilities industries as shown above. M&A value shrank in the Financial, Indus-

trials, Materials, and Telecom industries. The largest swing in deal volume was in the Utilities sector (doubled).

Increases in deal volume from upward trending sectors was significant enough to offset sectors experiencing

deal volume declines, solidifying the Eastern U.S. as 2014’s M&A value and transactional leader.

M

aterials

H

ealthcare

Energy

Consumer

Financial

Industrials

Materials

Telecom

Utilities

Energy

Healthcare

Technology

190

Eastern Region Leads U.S. M&A Recovery

0

50

100

150

200

250

300

Telecom

93

30

9

9

5 3

18

12

80

26

20

18

17

11

7

1 1

2

Note: Industry classifications: manufacturing, distribution, logistics etc. are included in the

industry subsectors above.

Financial

3. *All report data is based on Factset transaction info

Top Subsectors

Eastern U.S. Subsector Analysis

Eastern U.S. Leading Subsectors Deal Volume

In Q1 2015, the Eastern region was led by the Technology, Consumer and Financial subsectors. These three

subsectors accounted for nearly 60% of all Eastern region transactions.

Technology is the clear Q1 2015 front runner, contributing 80 transactions which account for more than 45%

of the region’s total closed deals. This is on the heels of a vibrant 2014 which experienced an 8% increase in

number of deals completed (287) compared to (266) in 2013 and represented 24% of 2014 transactions. The

two prime subcategories, Application Software and Internet Software and Services make up close to 90% of the

deals closed, as companies continue to embrace new technologies and the services that support them.

The Consumer sector ranked second with 15% of total contributing transactions or 26 closed deals in Q1 2015,

consistent with ranking #2 in 2014, with a total deal volume of 158. This sector received a boost from economic

recovery driven by rising income levels and broad incremental job creation. The correlating subsector contrib-

uting to the lion’s share of Consumer transactions is Hospitality, accounting for 65% of 2014 transactions, and

55% of Q1 2015 transactions.

The Financials subsector contributed 11% of all deal volume with 20 transactions closed in the region, ranking

this sector as #3 in Q1 2015. This is a nice increase from its lower position in 2014, and an indicator of the con-

tinued positive effects of low interest rates and some loosening of regulatory scrutiny.

Technology (287)

Internet Software

& Services

IT Consulting

Application

SoftwareSemiconductors

Electronic Equipment

& Instruments

51%

23%

9%

8%

7%

Consumer (158)

10%

65%11%

5%

5%

Hotels,Resorts,

and Cruise Lines

Advertising

Packaged Foods

and Meats Foods

Broadcasting

Movies and Entertainment

Healthcare (133)

35%

20%

12%

Facilities

Equipment

ServicesPharmaeuticals

Biotechnology

Technology (80)

Internet Software

& Services

IT Consulting

Application

Software

Semiconductors

Electronic Equipment

& Instruments

45%

43%

6%

3% 3%

Consumer (26)

Hotels,Resorts,

and Cruise Lines

Advertising

Packaged Foods

and Meats Foods

Broadcasting

Movies and Entertainment

8%

55%

30%

4% 3%

Financials (20)

Regional

Insurance

Brokers

Property & Casualty

Insurance

Thrifts & Mortgage

Finance

Investment Banking

& Brokerage

25%

45%

15%

10%

5%

Q1 2015

FY 2014

3

20%

14%

4. How does this affect you?

Conclusion

The DAK Group focuses exclusively on the M&A needs of middle market companies. We help mid-market CEO’s, entrepreneurs, and stake-

holder’s navigate their financial options for growth and expansion as well as pursue successful exit strategies.

Since its founding in 1984, The DAK Group has completed over 600 transactions across a broad range of industries. We are committed to

maximizing enterprise value for our clients in mergers, acquisitions, divestitures, capital raises and financial restructuring. In addition, we

provide business assessments and improvement plans, valuations and fairness opinions. Optimizing shareholder value, maintaining confi-

dentiality, providing senior level attention and being a trusted partner are at the core of DAK’s client-centric philosophy.

The DAK Group 195 Route 17 South Rochelle Park, NJ 201-712-9555 www.dakgroup.com

EBITDA Multiples

Consumer

Healthcare

Financials

Industrials

Technology

Materials

Telecom

Utilities

100 20

An important measure of a company’s cash flow is

EBITDA — earnings before interest, taxes, depreciation

and amortization. The EBITDA multiple serves as a ba-

rometer of how an individual company or industry is

doing compared to others. Multiples of EBITDA vary

greatly depending on the specific market, size of the

company, key technology, and other factors.

During 2014 the highest concentration of reported

EBITDA multiples for lower mid-market companies

ranged from 4.20x to 6.10x. Excluding a few outliers

in the Financials, Technology and Utilities industries,

the average across all other industries was 6.53x in

2014, with a small increase to 6.81x in the first quarter

of 2015.

While EBITDA is an important factor in determining the

value of a business for sale or acquisition, it should not

be the only factor taken into consideration. Instead,

EBITDA should be considered alongside other key

value drivers.*

In 2015’s vibrant market, many business owners in the mid-market are considering their next steps. M&A volume

and value trends are cyclical. While today’s market is better than last year’s, for how much longer can we make this

claim?

Based on the data and trends in this report, we believe the cycle will continue for another 24-36 months. For busi-

ness owners thinking about a future exit strategy, the next two or three years may be the best time to take advan-

tage of current market conditions. Those with a longer time horizon or no plans to sell may want to use add-on

acquisitions as part of their growth strategy.

Energy

Q1 20152014

5

4

Request Our White Paper:

Do I Sell or Do I Grow? A CEO’s Dilemma

Or, to learn more about current trends in

mid-market M & A please contact:

Joan McGeough at 201-478-5261

jmcgeough@dakgroup.com

*For more information on other critical factors that will impact val-

uation please contact Joan McGeough, jmcgeough@dakgroup.

15