The Inspirational Story of Julio Herrera Velutini - Global Finance Leader

HDFC Bank Q3 net up 30%

1.

powered by bluebytes

Saturday , January 19, 2013

HDFC Bank Q3 net up 30%

Publication: Business Standard , Journalist:BS Reporter

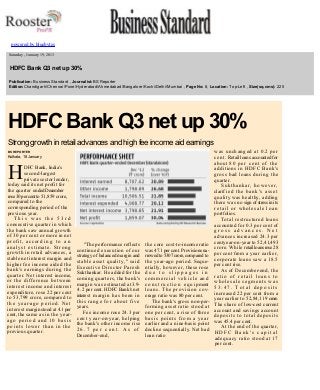

Edition:Chandigarh/Chennai/Pune/Hyderabad/Ahmedabad/Bangalore/Kochi/Delhi/Mumbai , Page No: 8, Location: TopLeft , Size(sq.cms): 225

HDFC Bank Q3 net up 30%

Strong growth in retail advances and high fee income aid earnings

BS REPORTER

Kolkata, 18 January

H

DFC Bank, India's

secondlargest

private sector lender,

today said its net profit for

the quarter ended December

rose 30 per cent to 51,859 crore,

compared to the

corresponding period of the

previous year.

This was the 53rd

consecutive quarter in which

the bank saw annual growth

of 30 per cent or more in net

p r o f i t , a c c or d i n g t o a n

analyst estimate. Strong

growth in retail advances, a

stable net interest margin and

higher fee income aided the

bank's earnings during the

quarter. Net interest income,

or the difference between

interest income and interest

expenditure, rose 22 per cent

to 53,799 crore, compared to

t h e y e a ra g o p e r i o d . N e t

interest margin stood at 4.1 per

cent, the same as in the year

ago period and 10 basis

points lower than in the

previous quarter.

"The performance reflects

continued execution of our

strategy of balanced margin and

stable asset quality," said

Executive Director Paresh

Sukthankar. He added for the

coming quarters, the bank's

margin was estimated at3.9

4.2 per cent. HDFC Bank's net

interest margin has been in

this range for about five

years.

Fee income rose 24.3 per

c e n t y e a ronyear, helping

the bank's other income rise

26.7 per cent. As of

Decemberend,

the core costtoincome ratio

was 47.1 per cent. Provisions na

rrowed to 5307 crore, compared to

the yearago period. Seque

ntially, however, these rose

due to slippages in

commercial vehicle and

c o n s t r u c t i o n e q u i pment

loans. The provision cov

erage ratio was 80 per cent.

The bank's gross nonper

forming asset ratio stood at

one per cent, a rise of three

basis points from a year

earlier and a ninebasis point

decline sequentially. Net bad

loan ratio

was unchanged at 0.2 per

cent. Retail loans accounted for

about 8 0 p e r c e n t o f t h e

additions in HDFC Bank's

gross bad loans during the

quarter.

Sukthankar, however,

clarif i e d t h e b a n k ' s a s s e t

quality was healthy, adding

there was no sign of stress in its

r e t a i l o r w h ol e s a l e l o a n

portfolios.

Total restructured loans

accounted for 0.3 per cent of

gross advances. Net

advances increased 24.3 per

centyearonyear to 52,41,493

crore. While retail loans rose 28

per cent from a year earlier,

corporate loans saw a 18.5

per cent rise.

As of Decemberend, the

ratio of retail loans to

wholesale segments was

53:47. Total deposits

increased 22 per cent from a

year earlier to 52,84,119 crore.

The share of lowcost current

account and savings account

deposits to total deposits

was 45.4 per cent.

At the end of the quarter,

HDFC Bank's capital

adequacy ratio stood at 17

per cent.