1. C O M P A N Y U P D A T E

India

14 Sep 2012

Venus Remedies Rs 287

Sector: Pharma Positive research results

BSE Code 526953 NSE Code VENUSREM Venus Remedies has shown good progress from its

CMP (Sep 13) 287.5 52W H/L 308/141 research development pipeline in recent months,

Nifty 4,842 Sensex 18021

Equity Cap (m) 2,369 Face Value 10

with two of its innovative products getting patent

Shares (m) 9.74 Free Float 65.29% approvals by the US patent office. This marks a big

Market Cap (m) 2,816 3M Avg Vol 83524

stride in Venus’ ability show results from its R&D

investments, and the market has reacted positively,

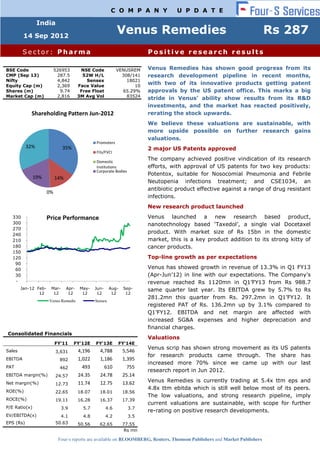

Shareholding Pattern Jun-2012 rerating the stock upwards.

We believe these valuations are sustainable, with

more upside possible on further research gains

valuations.

Promoters

32% 35% 2 major US Patents approved

FIIs/FVCI

Domestic

The company achieved positive vindication of its research

Institutions efforts, with approval of US patents for two key products:

Corporate Bodies

Potentox, suitable for Nosocomial Pneumonia and Febrile

19% 14%

Neutopenia infections treatment; and CSE1034, an

antibiotic product effective against a range of drug resistant

0%

infections.

New research product launched

330 Price Performance Venus launched a new research based product,

300 nanotechnology based „Taxedol‟, a single vial Docetaxel

270

240

product. With market size of Rs 15bn in the domestic

210 market, this is a key product addition to its strong kitty of

180 cancer products.

150

120 Top-line growth as per expectations

90

60 Venus has showed growth in revenue of 13.3% in Q1 FY13

30 (Apr-Jun‟12) in line with our expectations. The Company‟s

- revenue reached Rs 1120mn in Q1‟FY13 from Rs 988.7

Jan-12 Feb- Mar- Apr- May- Jun- Aug- Sep- same quarter last year. Its EBITDA grew by 5.7% to Rs

12 12 12 12 12 12 12

281.2mn this quarter from Rs. 297.2mn in Q1‟FY12. It

Venus Remedis Sensex

registered PAT of Rs. 136.2mn up by 3.1% compared to

Q1‟FY12. EBITDA and net margin are affected with

increased SG&A expenses and higher depreciation and

financial charges.

Consolidated Financials

Valuations

FY'11 FY'12E FY'13E FY'14E

Venus scrip has shown strong movement as its US patents

Sales 3,631 4,196 4,788 5,546

for research products came through. The share has

EBITDA 892 1,022 1,186 1,395

increased more 70% since we came up with our last

PAT 462 493 610 755

research report in Jun 2012.

EBITDA margin(%) 24.57 24.35 24.78 25.14

Net margin(%) 11.74 12.75 13.62 Venus Remedies is currently trading at 5.4x ttm eps and

12.73

4.8x ttm ebitda which is still well below most of its peers.

ROE(%) 22.65 18.07 18.01 18.56

The low valuations, and strong research pipeline, imply

ROCE(%) 19.11 16.28 16.37 17.39

current valuations are sustainable, with scope for further

P/E Ratio(x) 3.9 5.7 4.6 3.7

re-rating on positive research developments.

EV/EBITDA(x) 4.1 4.8 4.2 3.5

EPS (Rs) 50.63 50.56 62.65 77.55

Rs mn

Four-s reports are available on BLOOMBERG, Reuters, Thomson Publishers and Market Publishers

2. Company Report: Venus Remedies 10 Sep 2012

Steady growth in Q1 FY13, to continue through FY13

Particulars (Rs mn) Q1 FY'13 Q1 FY'12 Q4 FY'12 % Chg YoY % Chg QoQ

Net sales 1120 989 1135 13.3 (1.3)

Total Operating Income 1126 990 1147 13.7 (1.8)

Total Expenditure 829 709 864 16.9 (4.1)

Consumption of Raw 652 622 647 4.8 0.9

Materials

(Inc)/Dec in Stock In -30 -78 0 (62.0) -

Trade & WIP

Employees Cost 57 55 56 4.6 2.3

Other Expenditure 149 110 162 34.9 (8.0)

EBITDA 297 281 283 5.7 5.1

Depreciation 78 61 61 27.9 26.7

EBIT 220 221 221 (0.5) (0.8)

Interest & Finance charges 76 61 73 24.9 4.9

Other Income 1 0 2 207.3 (37.3)

PBT 145 160 151 (9.6) (4.1)

Tax Expense 4 24 -5 (82.4) (186.2)

PAT 141 136 156 3.1 (9.7)

*Standalone (Source: Ace Equity, company reports)

Stable growth in Q1 FY13

FY13 growth Venus Remedies reported revenue of Rs 1120mn in Q1 FY13, up

likely to remain from Rs 989mn in same quarter last year, a good 13.3% growth over

in line with Q1 the last year. Strong domestic market performance has contributed

FY13 growth to this growth. Domestic market grew from Rs 376mn in Q1 last year

to Rs 442mn in this quarter, a growth of 17.5% Y-o-Y. This gives

assurance that efforts taken by the company to boosts revenue in

the domestic market are on track.

The company believes that it will continue to drive the growth on

similar lines of 13-15% through-out the rest of the year with similar

performance expected from domestic & international market in the

near future.

Margins on the expected levels

The company has maintained margins in this quarter, EBITDA margin

at 26.4%, and 12.5% PAT margin. These margins are at par with its

historical figures and are on the expected lines. It clocked EBITDA of

Rs 297mn this quarter up from Rs 281mn in the same quarter last

year and PAT of Rs 140mn, up from Rs 136mn in Q1 FY12.

Company‟s efforts to improve reach in domestic and international

Four-S Research 2

3. Company Report: Venus Remedies 10 Sep 2012

market has pushed the sales and distribution cost which has

marginally affected the EBITDA margins for this quarter. The

continued expenditure on R&D and other expenses has in effect

pushed up the financing cost and depreciation. This has resulted in

marginal dip in PAT margins.

Key Ratios Q1 FY'13 Q1 FY'12 Q4 FY'12

EBITDA Margin 26.40% 28.40% 24.65%

Net Margin 12.48% 13.75% 13.57%

Total Expenditure/Operating 73.60% 71.60% 75.35%

Income

Raw Material Cost/Operating 55.31% 54.94% 56.38%

Income

Staff Cost/Operating Income 5.07% 5.51% 4.86%

Other Expenditure/Operating 13.22% 11.14% 14.11%

Income

*Standalone (Source: Ace Equity, company reports)

Margins compare favourably with peers

Maintains Venus Remedies‟ operating margins continue to be at the higher end

strong margins of its peer set. Most midcap pharma companies, including injectable

companies, have operating margins in the range of 15-25%. Venus‟s

reported EBITDA margin of 27% is better than most of this lot. It

must be noted that Venus books more R&D expense through its

balance sheet compared to its peers.

With recent patents and upcoming research product launches, Venus

could see further improvement in the EBITDA margins. We expect

this change to manifest from middle of FY14.

Better profitability supporting the growth

Q1’FY13 Net

Total EBITDA Net Income

Company Income EBITDA Margin Income Margin

Mid-Cap Peers

Ajanta Pharma 1718 371 22% 196 11%

Indoco Remed 1512 256 17% 104 7%

Natco Pharma 1345 290 22% 168 12%

Nectar Life 3936 604 15% 160 4%

Parabolic Drugs 3052 433 14% 98 3%

Injectable Peers

Strides Arcolab 5083 1313 26% 905 18%

Ahlcon Parenterals 248 49 20% 23 9%

Parenteral Drug 716 -130 -18% -302 -42%

Claris Life 1949 777 40% 323 17%

Four-S Research 3

4. Company Report: Venus Remedies 10 Sep 2012

Kilitch drugs 154 -1 -1% 29 19%

Average 1932 390 16% 169 6%

Venus 1120 297 27% 140 13%

(Source: Ace Equity, company reports)

R&D investments show greater results

Receives 2 US patents for its research products

2 significant US The innovation cell of Venus Remedies has given some significant

patent awards results this quarter. The Company received two patents from US

patent office for antibiotic products: Elores and Potentox. Both

products are from its anti microbial resistance (AMR) product line.

The US patents are significant achievement for Venus Remedies as

earlier the Company had patents mainly in EU and other regions like

Australia, South Africa and the developing world while missing out on

the major US market. These patents may further strengthen the

market‟s belief in Company‟s R&D capability and its ability to achieve

growth through its R&D products.

‘Super Bug’ resistant drug patented in US

CSE1034, to be Venus Remedies has received patent from the US Patent Office for a

launched as breakthrough antibiotic product CSE1034. The new drug product

Elores in the CSE1034, is an antibiotic adjuvant entity (AAE), has been found to be

Indian market, effective against a wide range of drug resistant infections including

is the most the `superbugs‟ like Carbapenemase resistant Metallo Beta

effective anti- Lactamses (MBL) strains. Venus is planning to launch this drug in

biotic India under the brand name ELORES and is planning to have a pre

formulation IND meeting with US FDA for fast track approval of this product.

today The drug has been found safe while effectively dealing with

hospital acquired (nosocomial) infections involving Metallo Beta

Lactamase and other resistant strains such as E. coli, K. pneumoniae,

P. aeruginosa & A. baumanni, with reduced drug induced toxicity

resulting in lesser adverse effects.

US patent for Potentox

Venus Remedies has received patent from the US Patent Office for

Potentox, the patent protects the composition of Potentox and

the method of treatment.

The Patent provides an exclusivity period for Potentox until May,

2027. In addition to this new patent grant, Potentox is protected by a

number of other patents from across the Globe including India,

Australia, New Zealand, South Korea, South Africa and Ukraine.

The Company has already been marketing Potentox successfully in

India and few of the emerging markets around the globe. The

Four-S Research 4

5. Company Report: Venus Remedies 10 Sep 2012

product is growing with a CAGR of 50% since past 3 years and now

Venus is planning to have a pre IND meeting with US FDA for fast

track approval of this product.

Designed novel, patented technology for anti cancer products

DPPC is a The Company has established pre-clinical proof of concept for its

patented drug Drug–Protein-Polymer-Conjugate (DPPC). The DPPC concept by

delivery Venus is a novel, patent protected technology, which will help in

platform alleviating cancer by specific and selective targeting of tumor cells.

This is a platform technology with a novel concept of triple conjugate

i.e., Drug -Protein-Polymer- Conjugate (DPPC).

New Product launched: Taxedol

Taxedol is a Venus Remedies Limited has introduced for the first time a nano

ready to use technology based “Ready-to-Use” single vial Docetaxel in the

single vial domestic market under the brand name “TAXEDOL”. This one-vial

cancer product formulation has the advantage of requiring a single dilution step in

suitable infusion solutions prior to administration. The product caters

to the Rs 15bn Indian Cancer Drug Industry, which is expected to

grow at close to 20% over the coming few years.

Valuation: Available at decent bargain even after the upsurge

EV/ EV/

Company Sales Price Mcap EV EBITDA Sales P/E

Mid-Cap Peers

Ajanta Pharma* 6435 411 9629 11228 8.4 1.7 13.2

Indoco Rem* 5851 69 6322 7191 8.6 1.2 14.1

Natco Pharma 5369 348 10849 11918 9.8 2.2 17.6

Nectar Life 14874 20 4496 4496 1.7 0.3 5.3

Parabolic Drugs* 10377 24 1507 6285 3.8 0.6 3.3

Injectable Peers

Strides Arco 24916 886 52026 57982 68.0 2.3 6.1

Ahlcon

Parenterals* 825 340 2448 2616 18.3 3.2 45.8

Parenteral Drugs 3333 70 1806 5502 -79.5 1.7 -2.3

Claris LIfe 7657 219 13986 14817 6.9 1.9 11.4

Kilitch Drugs* 914 80 1057 947 14.5 1.0 35.7

Venus Remedies 4181 286 2785 4579 4.8 1.1 5.4

*Standalone (Source: Ace Equity, company reports)

Stock has seen Venus has seen a partial re-rating since we made our initiatial

rerating, but research report. The share price has moved from 161 on 4 th June to

still cheap around 280-290 now. The driver behind the rerating has been the

award of new patents for the US markets, which has bolstered

investor confidence in the Company‟s research capabilities.

Four-S Research 5

6. Company Report: Venus Remedies 10 Sep 2012

Venus is currently trading at PE ratio of 5.4x which is still at 68%

discount of its peers average. With current US patents approvals,

regular product launch schedule and stable financial performance, we

believe current valuations are sustainable, with upside based on

further positive show from its R&D efforts.

We raise our target price expectations to Rs 350 by Sep‟13, implying

an upside potential upside of 22%. At this price the company quotes

at 4.5x FY14 expected eps and 4x FY14 expected EV/EBITDA.

Share Price and tt

400

350

7x

300

250

5x

200

150 3x

100

50

0

May-…

Aug-…

May-…

Aug-…

May-…

Aug-…

Nov-…

Dec-…

Mar-…

Nov-…

Dec-…

Mar-…

Nov-…

Dec-…

Mar-…

Apr-09

Sep-09

Feb-10

Sep-10

Feb-11

Sep-11

Apr-12

Sep-12

Jun-09

Jun-10

Jun-11

Jun-12

Jul-12

Jan-12

Four-S Research 6

11. Company Report: Venus Remedies 10 Sep 2012

About Four-S Services

Founded in 2002, Four-S Services is a financial boutique providing Research, Financial Consulting and Investment

Banking services. We have executed more than 100+ mandates across diverse range of industries for Indian as

well as global companies, investment firms and private equity and venture capital firms.

Our clients value our focused, actionable advice which is based on deep domain expertise in Education, Financial

Services, Media & Entertainment, Healthcare, Consumer Goods, Automotive, Energy, Logistics and

Manufacturing. For further information on the company please visit www.four-s.com

Disclaimer

The information contained herein has been obtained from sources believed to be reliable but is not necessarily

complete and its accuracy cannot be guaranteed. No representation, warranty, guarantee or undertaking, express

or implied, is made as to the fairness, accuracy or completeness of any information, projections or opinions

contained in this document. Four-S Services Pvt. Ltd. will not accept any liability whatsoever, with respect to the

use of this document or its contents. This Company commissioned document has been distributed for information

purposes only and does not constitute or form part of any offer or solicitation of any offer to buy or sell any

securities. This document shall not form the basis of and should not be relied upon in connection with any contract

or commitment whatsoever. This document is not to be reported or copied or made available to others.

Four-S may from time to time solicit from, or perform consulting or other services for any company mentioned in

this document.

For further details/clarifications please contact:

Alok Somwanshi Ajay Jindal

Alok.somwanshi@four-s.com Ajay.jindal@four-s.com

Tel: +91-22-42153659 Tel: +91-22-42153659

Four-S Research 11