CEIC WorldTrend Data Talk: The "New Mediocre" for the Global Economy

•

0 gefällt mir•251 views

Christine Lagarde, the managing director of the International Monetary Fund (IMF), warned in the latest World Economic Outlook (WEO) that the risk of a “new mediocre” prolonged slow growth is a challenge to the global economy. The trend is particularly evident in the advanced economies, where recovery is concentrated among a few countries, while the others are still struggling to return to their precrisis growth rates. The emerging markets, despite their robust growth outlook, are no exception. Read more: http://bit.ly/1xnjD7F

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Empfohlen

Empfohlen (20)

CEIC WorldTrend Data Talk: The "New Mediocre" for the Global Economy

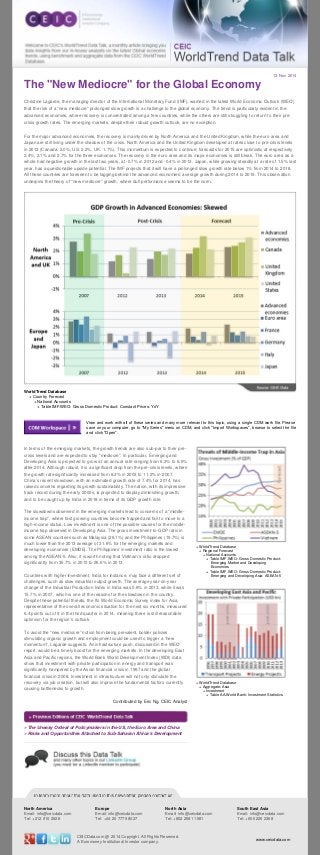

- 1. 13 Nov 2014 The "New Mediocre" for the Global Economy Christine Lagarde, the managing director of the International Monetary Fund (IMF), warned in the latest World Economic Outlook (WEO) that the risk of a “new mediocre” prolonged slow growth is a challenge to the global economy. The trend is particularly evident in the advanced economies, where recovery is concentrated among a few countries, while the others are still struggling to return to their pre-crisis growth rates. The emerging markets, despite their robust growth outlook, are no exception. For the major advanced economies, the recovery is mainly driven by North America and the United Kingdom, while the euro area and Japan are still living under the shadow of the crisis. North America and the United Kingdom developed at rates close to pre-crisis levels in 2013 (Canada: 2.0%, US: 2.2%, UK: 1.7%). This momentum is expected to continue; forecasts for 2015 are optimistic at respectively 2.4%, 3.1% and 2.7% for the three economies. The recovery in the euro area and its major economies is still bleak. The euro area as a whole had negative growth in the last two years, at -0.7% in 2012 and -0.4% in 2013. Japan, while growing steadily at a rate of 1.5% last year, has a questionable upside potential. The IMF projects that it will have a prolonged slow growth rate below 1% from 2014 to 2018. All these countries are foreseen to be lagging behind the advanced economies’ average growth during 2014 to 2019. This observation underpins the theory of “new mediocre” growth, where dull performance seems to be the norm. WorldTrend Database + Country Forecast + National Accounts + Table IMF.WEO: Gross Domestic Product: Constant Prices: YoY View and work with all of these series and many more relevant to this topic, using a single CDM work file. Please save on your computer, go to "My Series" menu on CDM, and click "Import Workspaces", browse to select the file and click "Open". In terms of the emerging markets, the growth trends are also sub-par to their pre-crisis levels and are expected to stay “mediocre”. In particular, Emerging and Developing Asia is projected to grow at an annual rate ranging from 6.3% to 6.6% after 2014. Although robust, it is a significant drop from the pre-crisis levels, where the growth rate significantly increased from 8.3% in 2003 to 11.2% in 2007. China’s recent slowdown, with an estimated growth rate of 7.4% for 2014, has raised concerns regarding its growth sustainability. The nation, with its impressive track record during the early 2000s, is projected to display diminishing growth, and to be caught up by India in 2018 in terms of its GDP growth rate. The slowdowns observed in the emerging markets lead to concerns of a “middle-income trap”, where fast growing countries become trapped and fail to move to a high-income status. Low investment is one of the possible causes for the middle-income trap observed in Developing Asia. The gross investment-to-GDP ratio in some ASEAN countries such as Malaysia (26.1%) and the Philippines (19.7%) is much lower than the 2013 average of 31.6% for the emerging markets and developing economies (EMDE). The Philippines’ investment ratio is the lowest among the ASEAN-5. Also, it is worth noting that Vietnam’s ratio dropped significantly from 35.7% in 2010 to 26.6% in 2013. Countries with higher investment, India for instance, may face a different set of challenges, such as slow industrial output growth. The average year-on-year change of the Industrial Production Index in India was 0.6% in 2013, while it was 15.7% in 2007, which is one of the reasons for the slowdown in the country. Despite these potential threats, the Ifo World Economic Survey index for Asia, representative of the overall economic situation for the next six months, measured 6.4 points out of 9 in the third quarter in 2014, meaning there is still reasonable optimism for the region’s outlook. To avoid the “new mediocre” notion from being prevalent, bolder policies stimulating organic growth and employment could be used to trigger a “new momentum”, Lagarde suggests. An infrastructure push, discussed in the WEO report, would be a timely boost for the emerging markets. In the developing East Asia and Pacific regions, the World Bank World Development Index (WDI) data show that investment with private participation in energy and transport was significantly hampered by the Asian financial crisis in 1997 and the global financial crisis in 2008. Investment in infrastructure will not only stimulate the recovery via job creation, but will also improve the fundamental factors currently causing bottlenecks to growth. Contributed by Eric Ng, CEIC Analyst » The Uneasy Ordeal of Policymakers in the US, the Euro Area and China » Risks and Opportunities Attached to Sub-Saharan Africa’s Development + WorldTrend Database + Regional Forecast + National Accounts + Table IMF.WEO: Gross Domestic Product: Emerging Market and Developing Economies + Table IMF.WEO: Gross Domestic Product: Emerging and Developing Asia: ASEAN-5 + WorldTrend Database + Aggregate: Asia + Investment + Table AA.World Bank: Investment Statistics North America Email: info@ceicdata.com Tel: +212 610 2928 Europe Email: info@ceicdata.com Tel: +44 20 7779 8027 North Asia Email: info@ceicdata.com Tel: +852 2581 1981 South East Asia Email: info@ceicdata.com Tel: +65 6225 2368 CEICData.com @ 2014 Copyright. All Rights Reserved. A Euromoney Institutional Investor company. www.ceicdata.com