NO1 Certified Black Magic Removal in Uk kala jadu Specialist kala jadu for Lo...

Blue Star

1. 1QFY2011 Result Update | Cons Durables

July 30, 2010

Blue Star NEUTRAL

CMP Rs441

Performance Highlights Target Price -

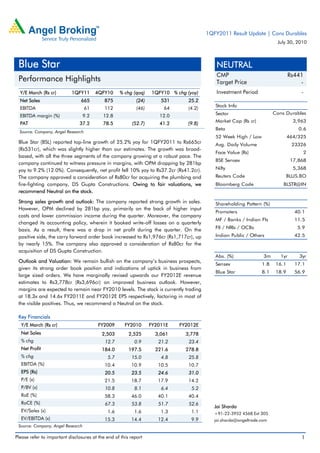

Y/E March (Rs cr) 1QFY11 4QFY10 % chg (qoq) 1QFY10 % chg (yoy) Investment Period -

Net Sales 665 875 (24) 531 25.2

Stock Info

EBITDA 61 112 (46) 64 (4.2)

Sector Cons Durables

EBITDA margin (%) 9.2 12.8 12.0

Market Cap (Rs cr) 3,963

PAT 37.2 78.5 (52.7) 41.2 (9.8)

Beta 0.6

Source: Company, Angel Research

52 Week High / Low 464/325

Blue Star (BSL) reported top-line growth of 25.2% yoy for 1QFY2011 to Rs665cr Avg. Daily Volume 23326

(Rs531cr), which was slightly higher than our estimates. The growth was broad-

Face Value (Rs) 2

based, with all the three segments of the company growing at a robust pace. The

BSE Sensex 17,868

company continued to witness pressure in margins, with OPM dropping by 281bp

yoy to 9.2% (12.0%). Consequently, net profit fell 10% yoy to Rs37.2cr (Rs41.2cr). Nifty 5,368

The company approved a consideration of Rs80cr for acquiring the plumbing and Reuters Code BLUS.BO

fire-fighting company, DS Gupta Constructions. Owing to fair valuations, we Bloomberg Code BLSTR@IN

recommend Neutral on the stock.

Strong sales growth and outlook: The company reported strong growth in sales. Shareholding Pattern (%)

However, OPM declined by 281bp yoy, primarily on the back of higher input

Promoters 40.1

costs and lower commission income during the quarter. Moreover, the company

MF / Banks / Indian Fls 11.5

changed its accounting policy, wherein it booked write-off losses on a quarterly

basis. As a result, there was a drop in net profit during the quarter. On the FII / NRIs / OCBs 5.9

positive side, the carry forward order book increased to Rs1,976cr (Rs1,717cr), up Indian Public / Others 42.5

by nearly 15%. The company also approved a consideration of Rs80cr for the

acquisition of DS Gupta Construction.

Abs. (%) 3m 1yr 3yr

Outlook and Valuation: We remain bullish on the company’s business prospects,

Sensex 1.8 16.1 17.1

given its strong order book position and indications of uptick in business from

Blue Star 8.1 18.9 56.9

large sized orders. We have marginally revised upwards our FY2012E revenue

estimates to Rs3,778cr (Rs3,696cr) on improved business outlook. However,

margins are expected to remain near FY2010 levels. The stock is currently trading

at 18.3x and 14.6x FY2011E and FY2012E EPS respectively, factoring in most of

the visible positives. Thus, we recommend a Neutral on the stock.

Key Financials

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

Net Sales 2,503 2,525 3,061 3,778

% chg 12.7 0.9 21.2 23.4

Net Profit 184.0 197.5 221.6 278.8

% chg 5.7 15.0 4.8 25.8

EBITDA (%) 10.4 10.9 10.5 10.7

EPS (Rs) 20.5 23.5 24.6 31.0

P/E (x) 21.5 18.7 17.9 14.2

P/BV (x) 10.8 8.1 6.4 5.2

RoE (%) 58.3 46.0 40.1 40.4

RoCE (%) 67.3 53.8 51.7 52.6

Jai Sharda

EV/Sales (x) 1.6 1.6 1.3 1.1 +91-22-3952 4568 Ext 305

EV/EBITDA (x) 15.3 14.4 12.4 9.9 jai.sharda@angeltrade.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

2. Blue Star | 1QFY2011 Result Update

Exhibit 1: 1QFY2011 Performance

Y/E March (Rs cr) 1QFY11 4QFY10 % chg (qoq) 1QFY10 % chg (yoy) FY2010 FY2009 % chg

Net Sales 664.8 874.7 (24.0) 531.0 25.2 2,549.4 2,519.4 1.2

Consumption of RM 504.3 644.2 (21.7) 380.0 32.7 1,882.1 1,874.3 0.4

(% of Sales) 75.9 73.6 71.6 73.8 74.4

Staff Costs 47.3 48.1 (1.6) 46.4 1.9 184.9 182.3 1.4

(% of Sales) 7.1 5.5 8.7 7.3 7.2

Other Expenses 52.3 70.5 (25.8) 41.1 27.4 183.3 186.5 (1.7)

(% of Sales) 7.9 8.1 7.7 7.2 7.4

Total Expenditure 604.0 762.8 (20.8) 467.5 29.2 2,250.3 2,243.0 0.3

Operating Profit 60.9 112.0 (45.6) 63.5 (4.2) 299.2 276.4 8.2

OPM (%) 9.2 12.8 12.0 11.7 11.0

Interest 2.0 2.5 (20.0) 1.5 37.9 8.5 17.3 (51.0)

Depreciation 7.6 9.1 (17.2) 8.2 (7.8) 34.7 25.9 34.2

Other Income 0.4 2.7 (85.7) 0.4 (7.3) 6.7 4.9 35.2

PBT (excl. Extr. Items) 51.7 103.0 (49.8) 54.3 (4.8) 262.7 238.2 10.3

Extr. Income/(Expense) 0.4 - - 14.0 -

PBT (incl. Extr. Items) 52.1 103.0 (49.4) 54.3 (4.0) 276.6 238.2 16.1

(% of Sales) 7.8 11.8 10.2 10.9 9.5

Provision for Taxation 15.0 24.5 (38.7) 13.1 14.2 65.1 57.9 12.4

(% of PBT) 28.7 23.8 24.2 23.5 24.3

Reported PAT 37.2 78.5 (52.7) 41.2 (9.7) 211.5 180.3 17.3

PATM (%) 5.6 9.0 7.8 8.3 7.2

Equity shares (cr) 9.0 9.0 9.0 9.0 9.0

EPS (Rs) 4.1 8.7 (52.7) 4.6 (9.7) 23.5 20.0 17.3

Adjusted PAT 36.7 78.5 (53.2) 41.2 (10.8) 197.5 180.3 9.6

Source: Company, Angel Research

Segment-wise performance: The electro mechanical projects and packaged air-

conditioning systems (EMPPACS) division registered a strong 18.9% yoy increase in

sales for the quarter to Rs374cr (Rs314cr). EBIT of the division stood at Rs34cr,

implying an EBIT margin of 9.1%.

Sales of the cooling products (CP) division stood at Rs253cr (Rs190cr) for

1QFY2011, an increase of 33.1% yoy. EBIT of the division came in at Rs35cr,

while EBIT margin stood at 13.9% for 1QFY2011.

The professional electronics and industrial systems (PEIS) division posted a growth

of 30.9% yoy to Rs32cr (Rs25cr). EBIT of the division came in at Rs5.5cr, while EBIT

margin stood at 16.9% for 1QFY2011.

July 30, 2010 2

3. Blue Star | 1QFY2011 Result Update

Exhibit 2: Segment-wise performance

% chg % chg

Y/E March (Rs cr) 1QFY2010 4QFY2010 1QFY2011

(qoq) (yoy)

Total Revenue

A) EMPPACS 314.7 613.0 374.2 (39.0) 18.9

B) Cooling Products 190.3 186.9 253.4 35.5 33.1

C) PEIS 24.7 54.7 32.3 (40.9) 30.9

Total 529.7 854.6 659.8 (22.8) 24.6

Less: Inter-Seg. Revenue - - -

Net Sales 529.7 854.6 659.8 (22.8) 24.6

EBIT

A) EMPPACS 34.6 79.0 34.0 (56.9) (1.5)

B) Cooling Products 33.2 28.7 35.2 22.7 6.1

C) PEIS 7.1 19.8 5.5 (72.5) (22.8)

EBIT Margin (%)

A) EMPPACS 11.0 12.9 9.1 (379bp) (188bp)

B) Cooling Products 17.5 15.4 13.9 (146bp) (3545bp)

C) PEIS 28.6 36.2 16.9 (1937bp) (1172bp)

Source: Company, Angel Research

Healthy order book indicates bright revenue prospects: In 1QFY2011, the

company’s sales growth was robust across all the three segments. Growth visibility

high on the back of the healthy order book of Rs1,976cr (Rs1,717cr). Besides, the

company’s acquisition of DS Gupta Construction will give additional fillip to sales.

Exhibit 3: Sales Trend

1000 30.0

875

900 25.0

800 714 20.0

647 665

700 596 15.0

567 540 564

600 10.0

(Rs cr)

(%)

500 5.0

400 0.0

300 -5.0

200 -10.0

100 -15.0

0 -20.0

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

Sales (LHS) yoy Growth (RHS)

Source: Company, Angel Research

Weak profit margins during 1QFY2011 to improve: The company witnessed a

decline of 281bp yoy in OPM during 1QFY2011. However, we expect full year

margins to remain at FY2010 levels, as input prices stabilise. In FY2012E, we

expect the company to clock OPM of 10.7%.

July 30, 2010 3

4. Blue Star | 1QFY2011 Result Update

Exhibit 4: OPM Trend

120.0 16

14

100.0

12

80.0

10

(Rs cr)

(%)

60.0 8

6

40.0

4

20.0

2

- 0

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

EBITDA (LHS) OPM (RHS)

Source: Company, Angel Research

As a result of the decline in OPM and change in accounting policies, PAT during

the quarter fell by 10% to Rs37cr.

Exhibit 5: Profit Trend

90

80

70

60

50

(Rs cr)

40

30

20

10

0

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

Source: Company, Angel Research 1QFY11

July 30, 2010 4

5. Blue Star | 1QFY2011 Result Update

Management Call - Key Takeaways

The company has approved a consideration of Rs80cr to acquire, the

plumbing and fire-fighting major, DS Gupta Construction. The company will

leverage this acquisition to cross sell its services to DS Gupta’s customers.

Funding for the acquisition will to be done through internal accruals and debt.

EMPPACS division is expected to record higher billing in the coming quarters,

as transformation of the order book is now complete and incremental orders

are expected to translate into sales.

The company is witnessing an uptick in demand in the ducted systems space

after 18 months of de-growth. This is generally a pre-cursor to the

improvement in business in the large order space. This augurs well for the

company.

There is a lot of activity in the small commercial sector. The real estate and

retail segments are also showing signs of revival. However, there is still not

much activity seen in the office space and IT segment.

Pricing pressure is expected to ease after new order inflows start coming

through, which the company expects to start happening in 4-6 months.

Cooling products division growth was driven by the healthy 34% growth in the

refrigeration and air-conditioning segment.

July 30, 2010 5

6. Blue Star | 1QFY2011 Result Update

Investment Arguments

Substantial demand for centralised air-conditioning, cold storage to drive future

growth: The surge in demand for commercial space and increasing corporate and

government thrust for setting up an efficient cold chain infrastructure in the country

is set to trigger demand for centralised air-conditioning and cold storage system in

India. BSL's cold storage division too has high growth potential with the aggregate

cost of providing a nation-wide cold chain infrastructure estimated to cost more

than Rs15,000cr.

To maintain leadership position owing to superior execution skills: BSL's strength

lies in its superior execution skills compared to competition. The company, with

30% market share in the central air-conditioning system segment, is a preferred

vendor with the institutional clients. The company's list of national account

customers provides repetitive business.

Present in high-margin segments: BSL is a diversified player in the air-conditioning

industry and is focused on high-margin segments including commercial

refrigeration, cold storage and central air-conditioning. The company has

improved its margins following an increase in the average ticket size of orders. The

easing of pricing pressures is also expected to improve the company's margins

going ahead.

Outlook and Valuation

We maintain our positive view on the company, given the strong growth indicators

across all the three segments and a healthy order book of Rs1,976cr. The

acquisition of DS Gupta Construction will complement the company’s service

bouquet, which would now have a strong presence in the plumbing and fire

fighting space. The company will also be able to cross sell its existing services to

DS Gupta’s customers. The transformation of the order book implies that the order

book growth will start translating into higher sales for the company. The uptick in

the ducted systems segment augurs well for the business outlook, as it generally

precedes the inflow of large sized orders. Overall, we expect the company to post

CAGR of 22.3% in sales over FY2010-12E. Once complete recovery happens,

OPM of the company would also improve and remain at FY2010 levels. Thus, we

expect OPM to come in at 10.5% in FY2011E and at 10.7% in FY2012E.

Exhibit 6: Revised Estimates

Rs cr Old New % chg

FY2011E FY2012E FY2011E FY2012E FY2011E FY2012E

Sales 2,994 3,696 3,061 3,778 2.2 2.2

EBITDA 314 395 321 404 2.2 2.2

EBITDA % 10.5 10.7 10.5 10.7

PAT 217 273 222 279 2.4 2.1

EPS 24.1 30.3 24.6 31.0 2.4 2.1

Source: Company, Angel Research

July 30, 2010 6

7. Blue Star | 1QFY2011 Result Update

Currently, the stock is trading at 17.9x and 14.2x FY2011E and FY2012E EPS

respectively, factoring in most of the growth prospects. We have valued DS Gupta

Construction’s business at 1x the consideration approved by BSL and added it to

the Target Price. However, the stock is trading at levels very close to our Target

Price. Hence, we recommend a Neutral on the stock.

Exhibit 7: Key Assumptions

FY2011E FY2012E Remarks

EMPPACS Contribution to Sales 70.6 71.5 High growth expected on account of demand revival

Cooling Prod Contribution to Sales 23.3 22.7 Strong growth momentum to continue

PEIS Contribution to Sales 5.4 5.3

OPM (%) 10.5 10.7 OPM to improve following decline in raw material prices

Tax Rate (%) 27.2 27.2 Higher compared to FY2010 as tax benefits on one plant end

Source: Angel Research

Exhibit 8: Peer Valuations

Company Mcap CMP P/E (x) P/BV (x) EV/EBITDA (x) RoE (%)

(Rs cr) (Rs) FY11E FY12E FY11E FY12E FY11E FY12E FY11E FY12E

Blue Star 3,970 441 17.9 14.2 6.4 5.2 12.4 9.9 40.1 40.4

Voltas 7,033 213 19.4 15.9 5.5 4.3 13.1 10.8 31.1 29.1

Source: Company, Bloomberg, Angel Research

Exhibit 9: One-year forward P/E band

600

500

Share Price (Rs)

400

300

200

100

0

Apr-04 Apr-05 Apr-06 Apr-07 Apr-08 Apr-09 Apr-10

Price 8x 11x 14x 17x 20x

Source: Company, Bloomberg, Angel Research

July 30, 2010 7

8. Blue Star | 1QFY2011 Result Update

Profit and Loss

Y/E March (Rs cr) FY07 FY08 FY09 FY10 FY11E FY12E

Gross sales 1,595 2,222 2,552 2,558 3,061 3,778

Less: Excise duty - - 49.7 32.6 - -

Net Sales 1,595 2,222 2,503 2,525 3,061 3,778

Other operating income - - - - - -

Total operating income 1,595 2,222 2,503 2,525 3,061 3,778

% chg - 39.3 12.7 0.9 21.2 23.4

Total Expenditure 1,484 1,999 2,243 2,250 2,740 3,374

Net Raw Materials 1,243 1,691 1,874 1,882 2,308 2,852

Other Mfg costs 49 68 50 50 95 118

Personnel 117 145 182 185 214 253

Other 75 95 136 133 122 151

EBITDA 110 223 260 275 321 404

% chg - 102.4 16.4 5.8 16.8 25.8

(% of Net Sales) 6.9 10.0 10.4 10.9 10.5 10.7

Depreciation& Amortisation 21 22 26 35 30 36

EBIT 89 201 234 240 290 368

% chg - 125.2 16.3 2.7 21.0 26.7

(% of Net Sales) 5.6 9.0 9.3 9.5 9.5 9.7

Interest & other Charges 10 8 14 8 2 1

Other Income 13 49 22 31 16 16

(% of PBT) 13.9 20.0 9.0 11.9 5.3 4.2

Recurring PBT 93 242 242 263 304 383

% chg - 161.5 (0.0) 8.6 15.9 25.8

Extraordinary Expense/(Inc.) 1 25 - - - -

PBT (reported) 92 217 242 263 304 383

Tax 21 68 58 65 83 104

(% of PBT) 23.3 31.3 23.9 24.8 27.2 27.2

PAT (reported) 70 149 184 198 222 279

Add: Share of earnings of

- - - - - -

associate

Less: Minority interest (MI) - - - - - -

Prior period items - - - - - -

PAT after MI (reported) 70 149 184 198 222 279

ADJ. PAT 70 149 184 198 222 279

% chg - 111.7 23.5 7.4 12.2 25.8

(% of Net Sales) 4.4 6.7 7.4 7.8 7.2 7.4

Basic EPS (Rs) 7.9 19.4 20.5 23.5 24.6 31.0

Fully Diluted EPS (Rs) 7.9 19.4 20.5 23.5 24.6 31.0

% chg - 144.6 5.7 15.0 4.8 25.8

July 30, 2010 8

9. Blue Star | 1QFY2011 Result Update

Balance Sheet

Y/E March (Rs cr) FY07 FY08 FY09 FY10 FY11E FY12E

SOURCES OF FUNDS

Equity Share Capital 18 18 18 18 18 18

Preference Capital - - - - - -

Reserves& Surplus 195 246 349 474 597 749

Shareholders Funds 213 264 367 492 615 767

Minority Interest

Total Loans 89 37 24 9 9 9

Deferred Tax Liability (Net) 7 4 1 (1) - -

Total Liabilities 309 304 391 499 623 776

APPLICATION OF FUNDS

Gross Block 231 273 333 351 381 444

Less: Acc. Depreciation 117 135 145 180 210 246

Net Block 114 138 188 171 170 199

Capital Work-in-Progress 2 18 25 28 27 27

Goodwill - - - - - -

Investments 5 5 4 4 4 4

Current Assets 733 1,034 1,149 1,393 1,629 1,973

Cash 5 3 6 13 28 27

Loans & Advances 169 257 293 132 337 378

Inventories 209 290 207 258 322 406

Debtors 351 484 643 628 942 1,162

Other - - - 361 - -

Current liabilities 548 892 975 1,097 1,207 1,427

Net Current Assets 184 142 174 296 422 546

Mis. Exp. not written off 2 1 1 - - -

Total Assets 309 304 391 499 623 776

July 30, 2010 9

10. Blue Star | 1QFY2011 Result Update

Cash Flow Statement

Y/E March (Rs cr) FY07 FY08 FY09 FY10 FY11E FY12E

Profit before tax 93 223 254 362 353 410

Depreciation 21 22 26 35 30 36

(Inc.)/ Dec. in Working Capital 37 129 6 (274) 93 (84)

Less: Other income 13 49 22 31 16 16

Direct taxes paid 21 68 58 65 83 104

Cash Flow from Operations 117 258 206 26 378 241

(Inc.)/ Dec. in Fixed Assets (24) (21) (165) (128) (157) (191)

(Inc.)/ Dec. in Investments (0) 1 0 0 - -

(Inc.)/ Dec. in loans and advances (78) (88) (35) 160 (204) (41)

Other income 13 49 22 31 16 16

Cash Flow from Investing (90) (60) (178) 64 (345) (216)

Issue of Equity - - - - - -

Inc./(Dec.) in loans 13 (53) (13) (15) - -

Dividend Paid (Incl. Tax) 31 74 74 84 105 126

Others (8.9) (73.5) 61.5 17.0 87.83 100.14

Cash Flow from Financing (27) (200) (25) (82) (17) (26)

Inc./(Dec.) in Cash - (2) 3 8 15 (1)

Opening Cash balances 5 5 3 6 13 28

Closing Cash balances 5 3 6 13 28 27

July 30, 2010 10

12. Blue Star | 1QFY2011 Result Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Blue Star

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

July 30, 2010 12