1. Looking the Other Way: The Absence of Remittance Regulation

Past Time?

In December 2010, ACORN International released our report, Past Time for Remittance Reform

(www.remittancejustice.org), in the cities where we work around the globe. The report painstakingly

documented the real costs incurred by migrant workers and immigrant families in sending remittances from the

country where they are residing, receiving remittances by their family members in their home countries, and

paying the assorted fees that banks and money transfer organizations (MTOs) charge for currency exchange.

Remittances are the monies transferred usually from family members or migrant workers back to other

family members and home communities. Such money transfers are well known as critical components of the

GNP for many developing countries around the globe and total close to $400 Billion USD in latest estimates

costing more than $44 Billion USD in estimated charges.

Despite the claims of the G-8 supported by World Bank research that the average costs of sending is

now around 10%, ACORN International found the all-inclusive costs to be at or above 20% for each transaction

of $100 remitted. In our report though we joined the call for a 5% cap on costs for remittances since it would

move more than $20 billion USD in increased support from developed to developing countries and its citizens

were the costs cut in half.

Past Time for Remittance Reform was sent to the key MTOs (MoneyGram and Western Union) and the

top twenty banks in North America (including HSBC, Bank of America, Citi, Scotiabank, BMO, and others)

asking for both response and meetings with leaders of ACORN International to discuss ways of achieving cost

efficiency reforms and reductions. The response was underwhelming. We were very disappointed.

Of the banks that did respond, we received an answer from HSBC, Wells Fargo, Scotiabank, and BMO.

Unfortunately most of the responses were in the vein of the public complaint of the Canadian Bankers’

Association quibbling not about our data or conclusions but about our selection of $100 as the base amount for

the survey. Many of the institutions offered bulk discounts for transmitting higher sums and chafed at the $100

even though it is the usual remittance level sent regularly by both members of ACORN International affiliated

organizations and research published by the Inter-American Development Bank and the World Bank. Only

Wells Fargo offered claims that a special program for their account holders was much, much less expensive to

26 countries and in fact in many cases they waived the fees (see their letter at www.remittancejustice.org).

Mostly in responding to this critical issue for immigrants and migrant workers, there was deafening

silence. We asked ourselves, “Why?” Then we turned to look for the reasons that MTOs and banks could reply

and respond with such impunity. How could they be so arrogant about their predatory pricing of remittances?

How could their governmental regulators be allowing such practices?

Who’s on First? What’s on Second?

ACORN International researchers went back country-by-country to review who was in charge of

regulating the remittance practices for banks and MTOs. Our researchers looked in all of our countries in Latin

America (Honduras, Dominican Republic, Peru, Argentina, and Mexico) and we found nada, nothing at all. We

looked in Kenya and elsewhere in Africa. Nothing! We looked in India. The same! The answer had to be that

“sending” countries, like Canada and the United States, had a grip on something this important and involving

such large amounts of money. Wrong!

Oh, there were regulations in a number of countries, especially North America and India about transfers

that might not be fully documented and therefore arguably support potential terrorism. This is decidedly against

the law. Getting a better understanding of the hawala system of informal money transfers that we barely

touched on in Past Time, our researchers and organizers in India confirmed and clarified that such systems

2. might be popular and might involve significant sums, but were definitely illegal for all of these reasons since

they lacked any paper trail for the transactions.

All of this is not to say that the responsibility for regulating such enterprise is not clear. We found it

well documented that national banks in each country have the full responsibility for regulating the banks

domiciled in their countries on all matters of transactions within their businesses, including therefore

remittances. In fact the World Bank responded aggressively to one of our partners in January 2011 concerning

the ACORN International report because they did not want to be misunderstood as having usurped a G-8 goal or

the prerogatives and prerequisites of national banks in the various countries who were responsible for regulating

in this area.

Nonetheless, looking closely even at the Federal Reserve, as the United States banking regulator, and the

National Bank of Canada, as the principal Canadian banking overseer, we could find no specific regulation of

remittances and absolutely nothing that addressed the issues of cost in relation to remittances. The “who’s on

first, what’s on second” style of absent minded blindness in this area seemed global, not regional.

We did find that late in 2010 the Canadian province of Quebec legislated in this area and at least

specifically mentioned remittances in the statute therefore asserting jurisdiction in this area of MTO activity.

Though this provincial legislation was silent on the issues of cost in general or any fees in specific, at least it

seemed clear in Canada that the provinces had authority and regulatory responsibility in this area, or at least

thought that they did, and were unchallenged in their assertions at this time.

The same thing turned out to be the case in the United States where state banking commissions and other

bodies had jurisdiction over MTOs. ACORN International’s researcher painstakingly reviewed thirty-two (32)

different states and found a plethora of evidence that the states were very interested in fees, but this interest only

translated into a commitment to collect licensing fees to allow such MTOs to do business within the state. The

lack of transparency and difficulty of comparing every single state on the same terms leaves the possibility that

there may be a “Quebec” somewhere in the USA that has begun to assert regulatory authority over MTOs, but

ACORN International’s researcher has not been able to find it yet. From what ACORN International’s research

shows now, states have the authority, promulgate rules for licensing, collect the fees, but have not done

anything to legislate the behavior of MTOs in the area of costs and fees to immigrant consumers. As the

attached report from the research in the United States establishes, this is a cash cow for the state’s where MTOs

do business, but the states are taking no responsibility for the predatory leeching of immigrants within their

boundaries. Licenses run most normally in the range of $1000 up to $6000 per company with a number of

states bunched in at $4000 per company. The payments to the state for handling the remittances can be hefty.

New Jersey charges $25,000 for a “foreign money transmitter” and $100,000 for a “money transmitter.” Texas

requires $300,000 as minimum security for MTOs. Oregon sets $150,000 as the maximum. All of the states

require various significant levels of surety bonds to warrant the transfers and prevent fly-by-night operations to

some degree and provide a limited recourse to such takeoffs and landings. In short it is not that USA state level

legislators and banking commissioners and agencies have not taken MTOs seriously, because they clearly have.

Unfortunately to date states have seen their mission as enablers of such enterprises and felt no compunction, nor

exercised any responsibility, to assure that the immigrant consumer of such services was protected by either

transparency or regulations against predatory practices. For remittance users the United States and Canada are

remittance deserts!

Two and Two Equals?

Additional research has produced a clearer picture and a better understanding of the resistance of the

industry to reform.

Essentially, the World Bank is not exactly wrong when it impotently describes the process of driving

costs from its faulty 10% estimate currently to the G-8 proscriptive number of 5% by 2014 as being achieved by

3. “competition,” since both the responses received by ACORN International and the impunity expressed by

banking and money transfer organizations on these issues indicate that may be virtually no governmental

agency anywhere in the world taking as its core mission protecting immigrant consumers from predatory

practices and pricing. By default the only thing that would lower prices would be competition in the

marketplace in the absence of any regulation whatsoever. It is no wonder that the responses received by

ACORN International touted each institution’s competitive pricing, since without any incentive towards fair

pricing an informal cabal of self-interested institutional pricing has become the order of the day.

The institutional response to the call for reform boils down to either “Why bother, the money is good;

we’re all in it together,” or in the alternative, “Make me!” Without any real stick bandied about by any national

bank system or state or provincial level authorities in the cause of regulation, institutions facilitating remittances

can continue to engage in something that ranges between monopoly pricing within its own customer base or

where they enjoy exclusive agreements and simple predation of immigrant families and migrant workers trying

to send desperate dollars back home.

To achieve the G-8 5% goal by 2014 (Canada and the USA are both members of the G-8 along with

other highly industrialized and large powerhouse economies), ACORN International and its member

organizations and families are clear will take regulation both at the national level for banks in this area and at

the state and provincial level for money transfer organizations. Working with various legislators we are now

already at work in various countries trying to determine the best legislative response. ACORN Canada has

taken the lead in both Ottawa at the federal level and in Ontario and British Columbia at the provincial level to

work with various members of Parliament from all sides of the political aisles to draft legislation that would

finally protect immigrants and achieve just and fair pricing and fees for remittances. Their effort could shape

the debate around the world in coming months as they begin to take aggressive action in this area now.

Under any terms two plus two for remittances justice and the immigrant families who use the system

and depend on the system can no longer equal zero. Nor when applied to pricing and fees can it be allowed to

equal ten or higher. A proper balance of real costs and fair fees will have to restore a just math to these

enterprises making two plus two something closer to the neighborhood of four, rather than the distortion that

has come to dominate the remittance industry as billions are taken in predatory profits better spent developing

families and fueling community improvements in emerging countries.

ACORN International is united in demanding regulation of remittances at every level now.

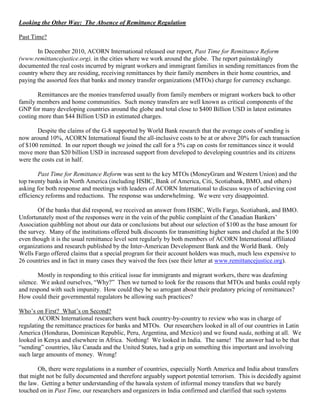

4. State Licensing Fees & Bond Requirements Reporting requirements Regulations of Fees

Maryland Initial License (application submitted in even numbered year) $4,000.00

Department of Financial Institutions Initial License (application submitted in odd numbered year): $2,000.00

http://www.dllr.state.md.us/finance Investigation Fee: $1000.00 States the number and aggregate dollar amount of payment instruments issued

License Renewal: $4,000.00 or sold and the aggregate number and dollar amount of money transmissions

Surety Bond Minimum $150,000 Maximum $1,000000 during the previous calendar year. None

New York

http://www.banking.state.ny.us

New Hampshire $500 for each principle owner $25 for each agent up to $4000 --each year None

http://www.nh.gov/banking

Colorado Surety Bond of at least $250,000 w/ max of $2,000,000 None

Colorado banking Board

http://www.dora.state.co.us/banking

The dollar volume of money transmitted for New Jersey clients only

New Jersey Base Assessment (Volume and Amount) and a complexity factor (up to $300) The dollar volume of payment instruments sold to New Jersey consumers None

New Jersey Department of Banking and Licensing fee S 700.00 The dollar volume of third party bills paid for New Jersey consumers

http://www.state.nj.us/dobi/banklicensing/mtfmtap $ 25,000 foreign money transmitter $100,000 money transmitter The dollar volume of store value cards

Surety Bond requirement & Financial Statements

Deleware

Deleware Office of State Bank Commissioner Can charge only 2% of the value of

www.banking.delaware.gov/ - Must report transactions of more than $10,000 check for payday lenders--not sure

if applies to mto but I think so

Texas The amount of the required security is the greater of $300,000 or an amount equal to None

Texas Department of Banking

http://www.banking.state.us

Georgia Money transmitters license $1000 None

Department of Banking and Finance Bond required -- amount ?

http://dbf.georgia.gov

California A licensee that engages in receiving money for transmission None

California Department of Financial Institutions shall maintain securities on deposit or a bond of a surety company in

http://www.dfi.ca.gov an amount greater than the average daily outstanding obligations for

money received for transmission in California, provided that such

amount shall not be less than two hundred fifty thousand dollars

($250,000) nor more than seven million dollars ($7,000,000).

License fee $5,000

Louisiana Application for License fee $350

Louisiana Office of Financial Institutions Annual report of all transactionsm, amounts with % in VA, US, and Foreign

Virginia a surety bond in the principal amount as determined by the Commission but not less None

Virginia Bureau of Financial Institutions

http://www.scc.virginia.gov/bfi/reg_inst/trans.aspx

Washington License fee $1000 main location $ 100 / additional Max $ 5,000 None

Washington Department of Financial Institutions Bond based on previous 12 month activity $10,000 to $ 550,000

http://www.dfi.wa.gov

Utah

Utah Department of Financial Institutions 42 annually licensed agencies -- can't find licensing requirements

www.dfi.utah.gov/ 1. A copy of the most recent audited consolidated annual financial statement,

2. The number of payment instruments sold in Minnesota, the dollar amount

Minnesota

Minnesota Department of Commerce Surety Bond - Each licensee must provide a surety bond, irrevocable letter of credit, 3. A list of permissible investments.

http://bit.ly/hkRc9T License fee -- $4000 Yearly renewal fee $ 2,500 4. A list of all locations in Minnesota at which licensed business is being

5. Any material changes to the original application that have not been

Filing bankruptcy or reorganization

Any revocation or suspension against the licensee by any state or

Any felony indictment or felony conviction of the licensee or any key

Any changes in control or controlling person

Notification of authorized delegate(s) contract termination

North Carolina

North Carolina Office of Commissioner of Banks Licensed industry - can't locate regulations--

http://www.nccob.gov/public/AboutUs/AboutMain.

Oregon

Oregon Department of Finance and Corporate License $1,000 Renewal $500

http://www.cbs.state.or.us/dfcs/ $25,000 security device, $5,000 per additional location; maximum of $150,000 None

Florida Listed as a Regulated industry - can's find regs

Connecticut $300,000 to $ 1,000,000 bond -- depending on level of activity

Connecticut Department of Banking $2,875 - Application filed between 10/1/2009 and 9/30/2010

http://www.ct.gov/dob/site/default.asp $1,875 - Application filed between 10/1/2010 and 9/30/2011

Pennsylvania License $ 1,000 Renewal $ 300 Bond Required $ 1,000,000 A Licensee shall, annually on or before January 31, file an annual report with the

Pennsylvania Department of Banking (1) financial statements, as of December 31 of the preceding year, signed under

http://bit.ly/eUwyUk (2) aggregate and other information on the amount of funds transmitted abroad

(3) any other information which the Commissioner may require from time to time

Massachusetts regulated but can't find license or bond amounts reports not required except as requested by Commissioner

Massachusetts Division of Banks

http://bit.ly/e5fhxk

Nebraska

Nebraska Department of Banking and Finance License $ 1,000

http://www.ndbf.ne.gov/soc/index.shtml Bond $100,000 min $250,000 max ($ 100 G base + $ 5000 for each agent in state) Quarterly Reports and Annual reports required containing: transaction date;

Vermont

Vermont Department of Banking Insurance Money Transmitter - $100,000.00, minimum amount (the bond amount increases by

http://www.bishca.state.vt.us/

Michigan

Michigan Office of Financial & Insurance Services Listed as regulated but can't find info

http://www.dleg.state.mi.us/fis/ind_srch/Consume

Ohio

Ohio Department of Commerce-Financial Can't find bond amounts

http://www.com.ohio.gov/fiin/Default.aspx License $ 6,000

Arkansas

Arkansas State Bank Department Can't find anything

http://www.state.ar.us/bank/

New Mexico

New Mexico Regulationa nd Licensing Have info on payday lending - nothing on mto's

http://www.rld.state.nm.us/

Wisconsin

Wisconsin Department of Financial Institutions no info on website

http://www.wdfi.org/

South Dakota

South Dakota Division of Banking • $500 initial application fee. The fee is nonrefundable.

http://www.state.sd.us/drr2/reg/bank/BANK- • $1,000 license fee. This fee will be refunded if the application is denied.

Surety bond of $ 100,000

North Dakota Investigation fee $ 450 License Fee $ 400

North Dakota Department of Financial Institutions Bond $ 150,000 min to max of $ 550,000

http://www.nd.gov/dfi/regulate/index.html

Oklahoma

Oklahoma Department of Bankins Site not working

http://www.state.ok.us/~sbd/

Tennessee

Tennessee Department of Financial Institutions <4 locations $50.00 / location -- 5 or more locations $500 + $12 / location

http://www.tn.gov/tdfi/ Bond required -can't find required amount

Kentucky

Kentucky Department of Financial Institutions Application fee $ 500 License fee $500

http://www.kfi.ky.gov/ $ 500,000 to $ 5,000,000 required

Hawaii

Hawaii Department of Commerce and Consumer License $ 2000 + $300 per location Application fee -- same

http://hawaii.gov/dcca/dfi/hrs/chapter-489d- Bond $ 1,000 to $ 500,000 depending on net worth of company

Wyoming

Wyoming Department of App Fee $ 3000 Annual License Renewal $2000 - $7000 depending on # of

http://bit.ly/g4GPWL Bond $ 10,000 to $500,000 depending on net worth of company